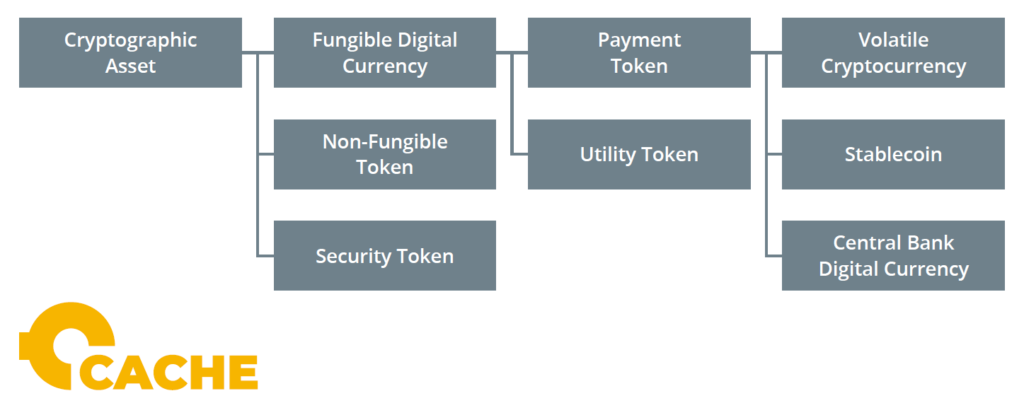

What are digital assets? Digital assets, or cryptographic assets, are tradable and digital representations of value that rely on decentralized consensus mechanisms for settlement.

According to the Basel Committee on Banking Supervision, the three distinguishing factors of cryptocurrencies are their digital nature; their use of cryptographic primitives, such as hash functions to verify the integrity of the data and symmetric encryption to create public and private keys; and decentralized record keeping and decision making.

Although there are over 7,000 cryptocurrencies listed on Coinmarketcap.com, not all of them serve the same purpose. Some are volatile digital currencies, such as Bitcoin, others are stablecoins that are pegged to the dollar, such as Tether. Generally, crypto assets fall into three categories including fungible digital currency, non-fungible tokens, and security tokens. Cryptocurrencies, stablecoins, and Central Bank Digital Currencies (CBDCs) are all forms of digital currency. Digital currency can also include online bank deposits issued to customers by banks, such as UBS or Deutsche Bank. The possession of digital currency often creates a legal claim against the electronic money issuer. However, this is not often the case with cryptocurrencies. In addition to fungible digital currency, non-fungible tokens can be used to represent unique assets, such as the Mona Lisa painting. Finally, security tokens often represent investment contracts, and they are regulated by securities laws.

Source: Cointelegraph Research

In addition to stablecoins pegged to fiat currencies, another class of tokens is gaining traction, whereby each token represents a commodity. For example, CACHE is a provider of regulated, transparent and redeemable tokens backed by gold stored in accredited vaults around the world. CACHE uses GramChain, a revolutionary new Proof of Reserve system, that enables the public to view photographs and see real-time status updates for each bar in each vault. CACHE provides fast, flexible redemption at scale with the option to sell the underlying gold for fiat currency. Based in Singapore, CACHE’s partners include vaults and gold dealers such as Brink’s, Dillon Gage, Loomis, Silver Bullion, and The Safe House as well as custody provider Onchain Custodian and digital asset exchange Bithumb Global.

The CACHE team draws on decades of experience in the precious metals and vaulting industry as well as legal, compliance, blockchain and cryptocurrency expertise. Each CACHE Gold token is backed by one gram of pure, investment-grade physical gold. CACHE Gold tokens can be redeemed for physical gold at any time. In amounts as small as 100 grams, redeemed gold can be sold for US dollars, shipped to the token holder’s address or collected in person at select vaults. Token holders have full control over their assets. No centralized third party can freeze or confiscate tokens. CACHE Gold tokens are deployed on the Ethereum public blockchain using the ERC-20 token standard. Bithumb Global and Bittrex Global both enable CACHE Gold token trading.

As these examples show, so-called “digital assets” are a very complex type of investment which, contrary to widespread public perception, cannot easily be reduced to a common denominator. The same also is true for the investors, because they are having different approaches and expectations of this new market. These aspects were also covered in our report, and next week we will make the findings available to our readers here on this blog.

Throughout Europe digital assets enjoy a great popularity among investors. Due to the significant price changes of individual assets in recent years, however, the timing of investments is an important factor in assessing the success of the individual investors. This article therefore aims at finding out when the investors we surveyed first started to invest in digital assets and which ones they primarily focused on.

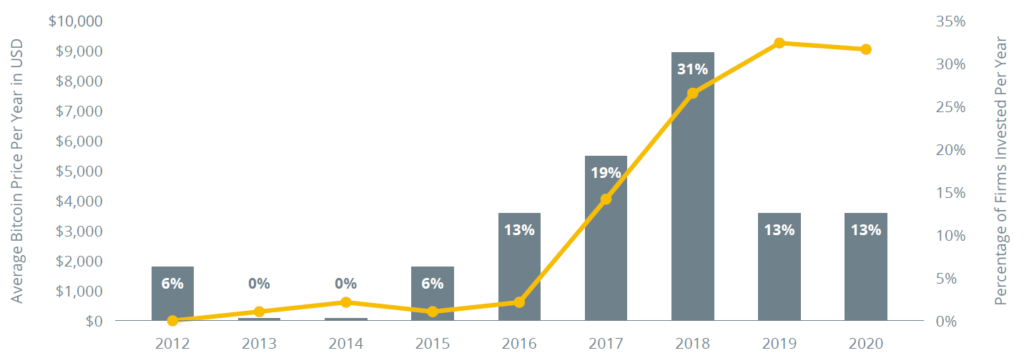

The majority of investors gained exposure to digital assets for the first time during the past two years. Nearly 31% of those surveyed invested in crypto assets in 2018 — after Bitcoin’s all-time high in mid-December 2017, when the price was almost $20,000 per coin and Bitcoin had a $334 billion market capitalization.

Question: What was the first year your company invested in digital assets?

Source: Cointelegraph Research, Bitcoin average yearly price data from Coinmarketcap.com

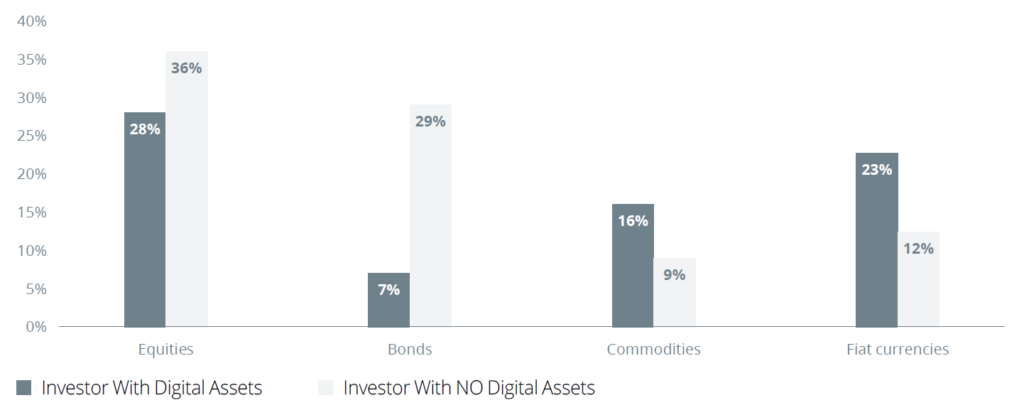

An important observation is that institutional investors that have invested in digital assets have distinctly different portfolios compared to ones that have no exposure to this asset class. Digital asset investors have significantly fewer bonds, more commodities, and more cash reserves than investors with no exposure to digital assets. This is in line with the ethos of the industry — lower trust in government bonds, higher trust in sound money, and growing cash reserves in expectation of a recession.

Average Asset Allocation of Institutional Investors

Source: Cointelegraph Research

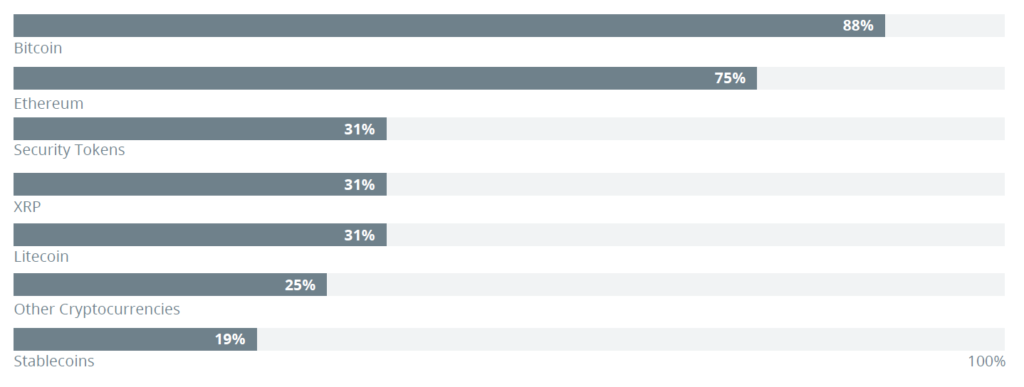

Cryptocurrencies are more interesting than Stablecoins and Security Tokens

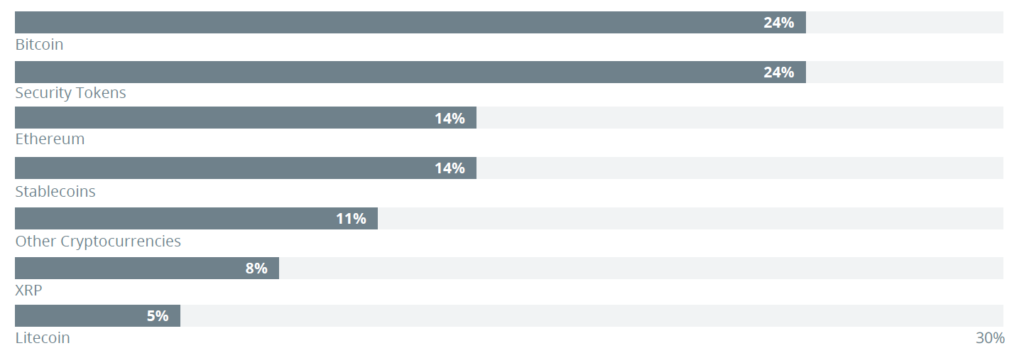

Bitcoin and Ethereum are still the most dominant cryptocurrencies. Around 88% and 75% of respondents exposed to cryptocurrencies have invested in these cryptocurrencies, respectively. Respondents have a clear preference for Bitcoin and Ethereum, as only 31% have invested in Litecoin and XRP. A quarter of the respondents answered that they had invested in “other cryptocurrencies”. Tezos, EOS, Stellar, Binance Coin, Cardano, Bitcoin Cash, and Bitcoin Satoshi’s Vision were among some of the other cryptocurrencies mentioned.

Question: Which types of digital assets has your company invested in?

Source: Cointelegraph Research

Stablecoins have become the most highly traded digital asset when measured by daily exchange-traded volume. On-chain trading activity grew over 800% between April 2019 to April 2020. However, only 19% of respondents own stablecoins, indicating that institutional investors may not be the dominant force responsible for stablecoin daily trading volumes. Notably, 31% of investors that have exposure to digital assets answered that they have invested in security tokens. This indicates that security tokens are on the radar of professional and qualified investors. Although venture capital was not a multiple choice option, two banks that manage over €350 billion in total mentioned that although the financial institution they work for has not invested directly in digital assets, they have invested in the equity of blockchain-related startups.

The European Union rolled out negative interest rates in 2014, and Switzerland has had them since January 2015. As Fidelity’s report on institutional demand from earlier this year pointed out, a common objection against investing in gold and Bitcoin is that they don’t produce an annual yield. However, in the current environment, these assets can help investors protect their wealth from inflation and negative interest rates.

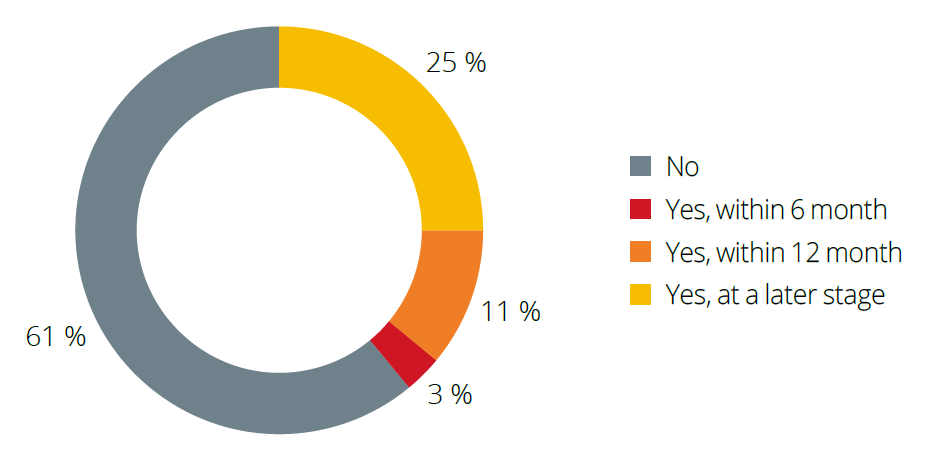

Future Demand

Among the 64% of investors who currently do not have cryptocurrencies in their investment portfolios, 39% plan to add them to their portfolio eventually. A quarter of the professional investors plan to buy cryptocurrencies at a later stage, and 14% of them plan to do so in the next 12 months.

Question: Is your company planning to invest in the future?

Source: Cointelegraph Research

Regarding the future demand for cryptocurrencies among professional investors, Bitcoin and security tokens are the assets in which investors are most interested. Surprisingly, there is more interest in security tokens and stablecoins amongst institutional investors than in cryptocurrencies such as Ethereum and XRP. This may be explained by the regulated nature of security tokens, as investors’ assets are often ring-fenced on the balance sheet of the issuer and rights in case of insolvency are explicitly mentioned in the prospectus. Furthermore, disputes can be settled by courts and contract law that the digital asset space is still building precedent for.

Question: Which digital assets would your company be interested in investing into in the future?

Source: Cointelegraph Research

After we have now dealt with these specific figures, we want to take a step back in the coming week, because some people will certainly ask themselves the question what exactly is meant by digital assets. The page Coinmarketcap.com lists more than 7000 different “cryptocurrencies”, however the differences between the entries could not be more substantial, which is the reason why we need a clarification.

Throughout Europe, investors have already invested millions of Euros and Swiss Francs into digital assets. Without a doubt, this is of significant importance for the economy in general and the crypto sector in particular, since these investors also play a major role in price movements. However, there are still only a small number of reports that systematically assess the demand for cryptocurrencies.

The first study was not focused on the German-speaking countries, and the second has not been published yet. Between November 2019 and early March 2020, Greenwich Associates under the auspices of Fidelity Digital Assets, Fidelity Center for Applied Technology, and Fidelity Consulting interviewed almost 800 investors across the U.S. and Europe.

Across the U.S. and Europe, 36% of the survey’s 774 respondents said they own cryptocurrencies or derivatives. The results show that over a third of institutional investors own digital assets. According to the survey, European investors generally have a more progressive view of digital assets, made evident when comparing the responses across all categories. Interestingly, this study found the same result: 36% of the survey’s 55 asset allocators said they have exposure to cryptocurrencies in the portfolio already.

The one survey that has targeted institutional demand for cryptocurrencies in the DACH region is BaFin’s survey of crypto asset derivatives. The German financial market regulator conducted a survey in late 2019; however, they have not published the results yet. In the survey’s preliminary research report, BaFin reported that there has been enormous growth of certificates that hold digital assets and contract for difference trading. Over 1,000 different certificates are on the market that have exposure to digital assets, and contracts for difference trading volume grew from €10 billion a month in August of 2018 to over €15 billion a month by January of 2019.

This study marks the first comprehensive survey of institutional investors on the topic of digital assets ever conducted across the German-speaking regions. The analysis contains key highlights of the survey’s results in addition to commentary from Crypto Research Report and Cointelegraph Research. Our experience combined with the proprietary dataset drives the unique perspective on the industry’s trends presented in this report.

Methodology

This survey had 55 responses from professional investors across the German-speaking countries including 44 online interviews and 11 case studies via telephone. Respondents included traditional banks, asset managers, and pension funds. This report focuses on buy-side, not sell-side asset allocators. Therefore, we did not send this survey to crypto funds that are invested 100% in digital assets. The goal of this report is to gauge the demand for digital assets from traditional financial intermediaries.

The survey was delivered via email to all registered professional investors with BaFin (Germany), FMA (Austria), FINMA (Switzerland), and the FMA (Liechtenstein) between the months of June to September of 2020. With the help of local banking associations, the survey was also sent out to the members of the BVI Deutscher Fondsverband and BAI in Germany, the Austrian Bankenverband, the Liechtensteinischer Anlagefondsverband, and members of SFAMA in Switzerland.

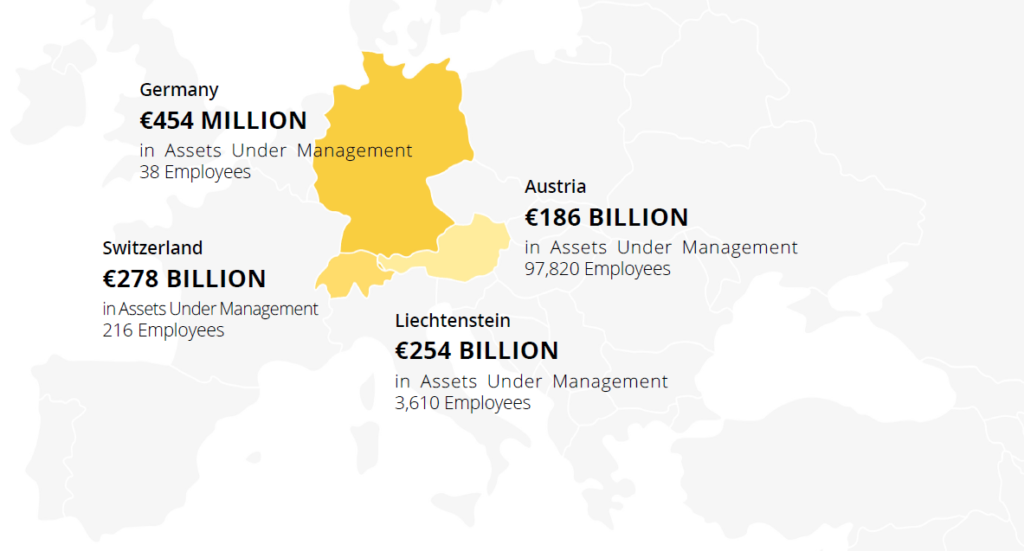

The majority of the respondents came from Switzerland (16) followed by Austria (10), Germany (7), and Liechtenstein (6). When sorting the survey results by country, the respondents from Switzerland managed the most assets with €278 billion. Austria’s respondents worked in firms with the highest headcount. The majority (83%) of the respondents worked in firms with less than 50 employees. Only three women that were in charge of asset allocation decisions at their company responded to the survey compared to 39 men. The median age of the respondent was 47.5 years old.

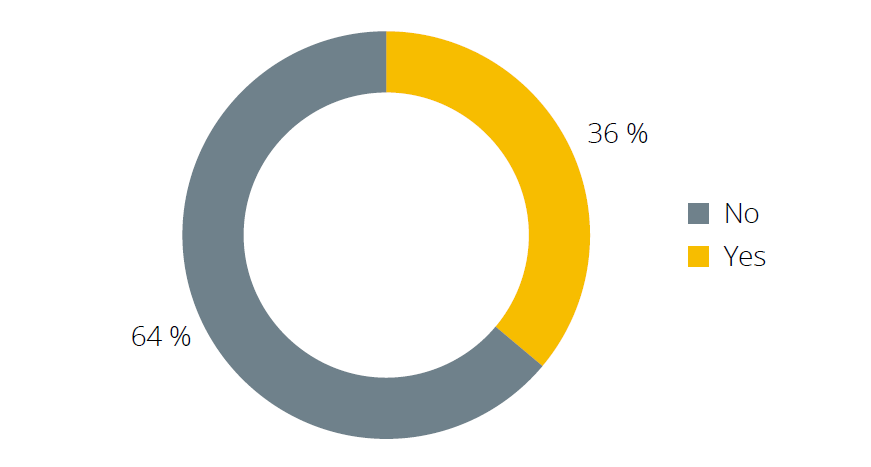

Current Exposure

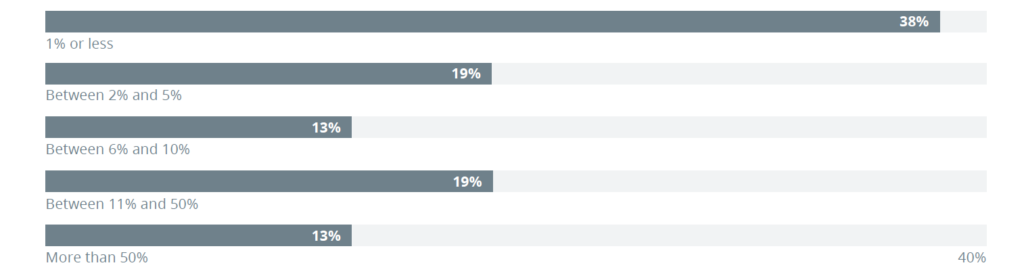

Over a third of the surveyed asset managers have invested in digital assets, while about 64% of respondents have not invested yet. Among the institutional investors who have had exposure to digital assets, approximately 69% of respondents have 10% or less of their assets under management in crypto assets. Notably, over a third of those surveyed have only 1% or less of their assets under management in crypto assets.

Question: Has your company invested in crypto assets in the past?

Source: Cointelegraph Research

This survey was conducted during the 2020 shutdown of the economy due to the government’s response to the Corona virus. During mid-March, many investors de-risked their portfolios and went into cash. From peak (February 19, 2020) to trough (March 17, 2020) Bitcoin lost 50% of its value, and briefly trading in the high 4000s. Since then, the price has recovered 115% to above $10,000. Bitcoin has performed better than equities, fixed income, real estate, and gold year to date (as of October 8, 2020). If governments continue to stimulate the economy with newly created money, then this trajectory is expected to continue. If the fiat faucet is ever turned off, there will likely be an ensuing correction in all asset classes.

Question: What percentage of your company’s assets under management are invested in crypto assets?

It is important to note that these figures apply to digital assets in general, but that there is a variety of these assets that are viewed by investors from different angles. Therefore, we will take a look next week at exactly how the interest is composed and what the conditions are for investors to make their purchases.

New survey on professional investors in Europe finds that 36% have already bought crypto. The percentage of big investors that plan to buy crypto in the future is even higher.

To gain a deeper understanding of how professional investors feel about digital assets, the Crypto Research Report and Cointelegraph Consulting has co-published a 70+ page research report written by eight authors and supported by SIX Digital Exchange, BlockFi, Bitmain, Blocksize Capital, and Nexo. TheDiscovering Institutional Demand for Digital Assets report highlights which coins wealthy investors already own and which ones they plan to buy in the coming months. The report also covers the most popular regulated funds and structured products that are designed for investors from the traditional finance realm.

The total assets under management managed by the 55 asset allocators that participated in the survey was over €719 billion, which almost double the entire market capitalization of the digital asset market. Out of those professional investors, 36% already had blockchain-inspired assets in their portfolio either through direct investment in cryptocurrencies, stablecoins, and security tokens or via funds, structured products, or futures. Out of the remaining 64% that have not yet invested, 39.29% plan to invest. This results in 61.15% of professional investors in the survey either already owning digital assets or planning to buy in the future.

The majority of investors with exposure to cryptographic assets were primarily interested in Bitcoin and Ethereum. Around 88% and 75% of respondents exposed to cryptocurrencies have invested in these cryptocurrencies, respectively. However, institutional investors appear to be increasingly interested in security tokens. Out of the 39.29% of investors that plan to invest in the future, security tokens were more popular than Ethereum and other alternative coins.

Some investors hold cryptographic assets for speculation rather than for use as a medium of exchange. They hope to “front-run” Wall Street by buying in before bigger pockets enter the market. Putting the fear of missing out aside, there are genuine reasons to be excited about institutional investors joining the space. Institutional investors hold the majority of the world’s wealth. The sheer size of the wealth managed by professional investors like pension funds, university endowments, and insurance companies is enough to have a dramatic impact on the entire digital asset industry if they enter the market. For years, there have been rumors that institutional investors were starting to buy cryptocurrencies, and now, the most recent academic survey provides evidence that this rumour is true.

The survey was conducted during June through September 2020 by Professor Dr. Philipp Sandner from the Frankfurt School of Finance & Management’s Blockchain Center, Professor Dr. Alfred Taudes from the Vienna University of Economics and Business’ Austrian Blockchain Center, and Cointelegraph’s Director of Research, Demelza Hays. The report is co-published by Cointelegraph Consulting and Crypto Research Report.

Our team of academics and seasoned blockchain technologists can cover a diverse range of topics including tokenomics, macroeconomics, legal, tax, central bank digital currencies, decentralized finance, supply chain logistics, and venture capital. To work with the Crypto Research Report and Cointelegraph Research team on creating a one-of-a-kind report, contact us at info@cryptoresearch.report.

In the book, The Liechtenstein Tax Law, Matthias Langer hits the nail on the head in respect to taxation of blockchain and FinTech companies in Liechtenstein. Alongside the tax law basics of Liechtenstein, Matthias Langer hits the nerve of the time by addressing the regulations for the taxation of blockchain and FinTech companies, and thus creates tax law clarity.

Published in 2019, the book opens up with the history of the Principality of Liechtenstein before moving on to the main topics of company, foundation, and trust law. The existing legal forms are presented concisely, followed by an overview of the type and scope of Liechtenstein’s audit, review and disclosure requirements, as well as the existing accounting regulations.

Matthias Langer has worked as a tax consultant in Liechtenstein for eleven years and now has his own law firm in Triesen. In the book, he delves into topics such as property and acquisition tax, gifts and inheritances, and income tax. The taxation of investment funds and foundations, as well as international tax law pertaining to offsetting and relocation find their way into the reading. Since Liechtenstein is also one of the pioneers in the blockchain and fintech, their handling of taxation is of great international interest. After a brief explanation of the basic terms and the balance sheet approach to cryptocurrencies, the peculiarities of the acquisition, income and value-added tax are discussed. In addition to differentiating different types of coins, the reader learns the tax significance of the transfer, trading, and storage of coins and tokens.

The book is easy to read due to the structure and short and accurate explanations that are illustrated with examples. In addition, the book enables quick reference and comprehension without the reader having to have in-depth tax knowledge. Although the book is primarily aimed at prospective entrepreneurs in Liechtenstein, it alsocontains information that is interesting for those who want to learn more about life in Liechtenstein and the country itself.

In summary, the book deals with all essential aspects of tax law in Liechtenstein. The treatment of tax law specifics of blockchain and fintech companies deserves special mention. The reader leaves the book with a deeper level of understanding of how crypto funds work and the taxation of cryptocurrencies. The book is only available in German at this time and can be bought on the publisher website, Springer Verlag.

Relai, a Dollar Cost Averaging bitcoin investing phone app made in Switzerland, announced a successful closing of its 200K CHF seed round at a valuation of 1M CHF – showing that venture capitalists are still investing in blockchain-inspired startups even during Covid-19. Among the investors is the controversial Bitcoin maximalist Giacomo Zucco, who served for the last years as board member of the Bitcoin Association Switzerland.

Relai allows its users to buy & sell Bitcoin directly via bank payment, without any account creation or KYC/AML verification, while still being fully regulatory compliant. The service is offered through a free, simple & user-friendly Smartphone App and available to all European countries. After only two months of being live, Relai’s volumes and revenues in August have more than doubled compared to July. The Relai App has been downloaded almost 2,000 times in more than 20 countries and processed well over 300’000 CHF/EUR in Bitcoin investments. More than 30 Bitcoins have already been sold, mostly to newcomers.

“Relai aims to finally boost Bitcoin mass adoption by making investing in Bitcoin as easy as finding a match on Tinder. While our great first numbers are a positive surprise, it doesn’t surprise me at all that people hate KYC and dealing with complicated user interfaces of Bitcoin & Crypto Investing Apps. If given the alternative, most newcomers will choose a service that is easy and KYC-less, for both convenience and privacy reasons.”

Julian Liniger, CEO of Relai

The most liked and most used feature of the Relai App is it’s DCA (Dollar Cost Average) function. Users can set up a weekly recurring buy order and watch their sats dropping in automatically.

“Bitcoin is currently affected by false dichotomies. You have economics-oriented experts advising newcomers to save and “stack sats” as opposed to focus on trading or spending, while infosec-aware experts advise them to avoid dangerous traps like KYC surveillance. You have terrible shitcoin-casinos wrapped in great mobile UX, versus Bitcoin best-practices limited to command-line. I like Relai since it tries to break these dichotomies with a minimalistic, intuitive, privacy-oriented, saving-oriented, Bitcoin-only design.”

What makes good money and how has the digital age changed the meaning of this term? This article takes a look at the key characteristics of a sound currency and then apply these to the MimbleWimble Coin. We will also speak with the developers of this project and demonstrate how a MWC transaction is executed.

A good money in the digital age must be: (1) recognizable, (2) scarce, (3) censorship resistant, (4) durable & indestructible, (5) extensible, (6) salable, (7) portable, (8) fungible, (9) private, and (10) divisible. However, most cryptocurrencies don’t meet these criteria. In 2019, one of the most talked about coins was “Grin.” However, investors quickly realized that Grin’s high inflation rate and lack of a hard cap on supply was worse than the inflation in the US dollar. This made people wonder why they should buy Grin with US dollars if Grin is a worse store of value. The Grin emission rate is 1 Grin per second indefinitely. There will be 31,536,000 Grin created per year. Currently, there are approximately 43 million Grin. This results in a very low stock-to-flow ratio in the early years. During 2020, the stock-to-flow ratio of Grin is approximately 1.19x or approximately 43,000,000 Grin divided by the new production of 31,536,000. This acts as a transfer of wealth from holders to miners.

As Saifedean Ammous explains, a low stock-to-flow ratio results in a transfer of value from holders of the asset to producers, while a high stock-to-flow ratio results in lower costs, measured in the asset itself, for holders. Before Grin launched, a MWC developer suggested there be an supply cap and emission rate change but was swiftly rejected by the Grin community which acted as a green light and was part of the inspiration for forking from Grin. After all, financial innovation is about trying many different approaches when bringing monetary products to market for consumers to enjoy. Every four years is a Bitcoin halving, and after the May 2020 halving the Bitcoin stock-to-flow ratio will be approximately 55. This will make it comparable to gold. MWC addressed the hard cap problem and low stock-to-flow ratio problem by placing a hard cap of 20,000,000 on the coin and then having a much slower emission rate Like Bitcoin, MWC uses a pure proof-of-work algorithm and has the highest stock-to-flow ratio of any base-layer MimbleWimble coin. By October 2020, MWC will have a stock-to-flow ratio almost equal to Bitcoin’s. And by February 2021, it will have a significantly higher stock-to-flow ratio.

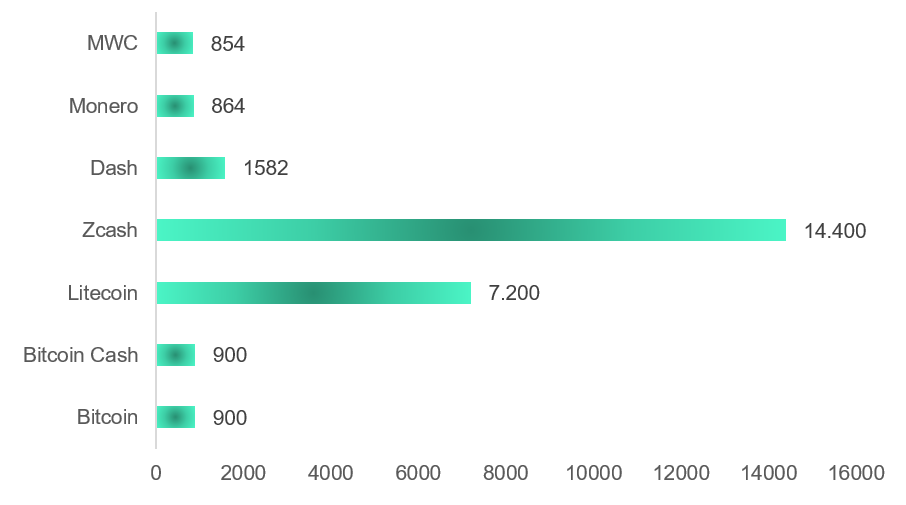

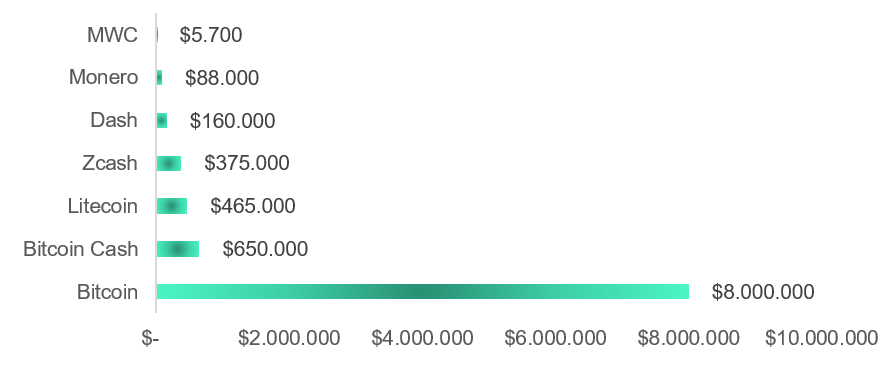

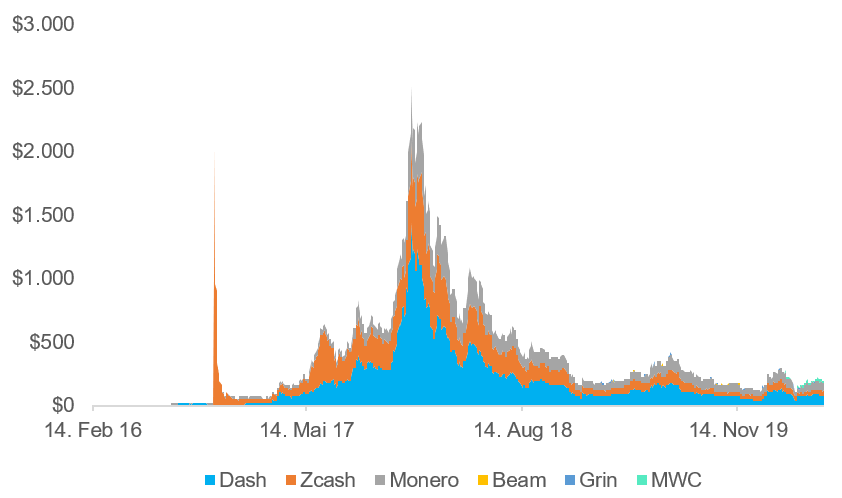

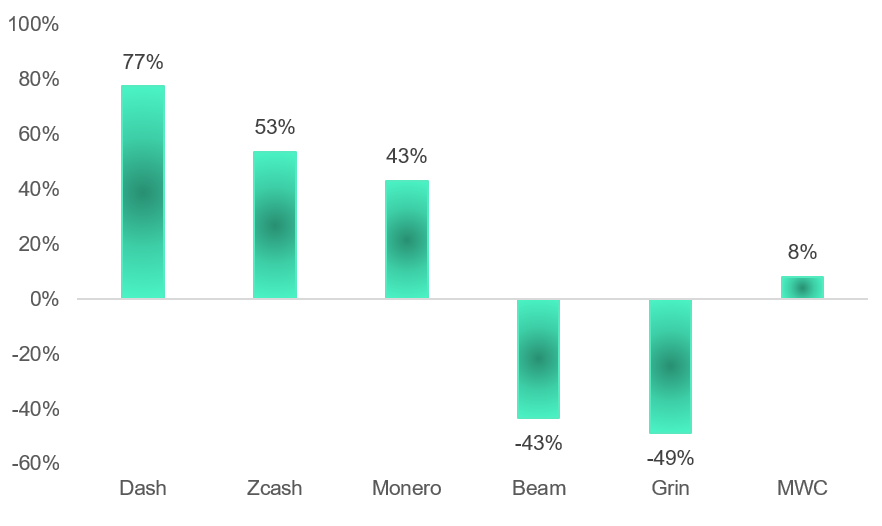

When looking at the number of coins created per day, MWC, Monero, Bitcoin, and Bitcoin Cash are the lowest. In terms of the US dollar value of the number of coins created per day, MWC is still the lowest, followed by Monero and Dash. Finally, the US dollar value of new coins created per year in relation to their US dollar market capitalization is also the lowest for MWC with 1.2 % followed by Bitcoin with 1.7 %, Monero with 2.8 %, Litecoin with 6.1 %, Dash with 8.4 %, and Zcash with an astonishing 35.1 %(!).

However, MWC has received some pushback from the cryptocurrency community because of how the initial stock was created. According to the whitepaper and protocol, half of the total supply of MWC were to be mined with proof of work mining, and the other half were created in the genesis block. From this initial stock of 10,000,000 MWC that was worthless when created, 2,000,000 MWC were immediately distributed to the developer team, 2,000,000 MWC were allocated to the HODL Program, and 6,000,000 MWC were airdropped to any Bitcoin holders who successfully registered over a three month period and claimed their MWC allocation during December 2019. Over 5.4 million MWC were successfully airdropped for free to Bitcoin holders and at the time had a total value less than $2 million. MWC primarily uses the C31 proof-of-work algorithm and MWC’s new monthly emission from a pure proof of work algorithm is about $500k.

How To Do A MWC Transaction

MWC was created to meet the demand for transferring money online with full privacy because Bitcoin transactions aren’t that private or fungible.2 MWC payments are slightly different to Bitcoin transactions, the least of which being that there are only outputs and no addresses. After all, everything is CoinJoined with Confidential Transactions and then the signatures are aggregated in the blocks.

To get started, you have to download a MimbleWimbleCoin wallet. To provide some context, the other privacy coin, Grin, relies mainly on command line interface tools, but they can be difficult for non-technical people to use. This is why MWC has created a very easy-to-use wallet that can be downloaded here: https://www.mwc.mw/downloads

After you have successfully setup your wallet, there are two main ways to send and receive transactions called the MWCMQS method and the File method. In general, this involves six steps:

The sender creates the transaction using output(s)

The receiver signs the transaction

The receiver returns the transaction to the sender

The sender signs the transaction

The sender broadcasts the transaction to the network

The miners confirm the transaction in a block and add it to the blockchain

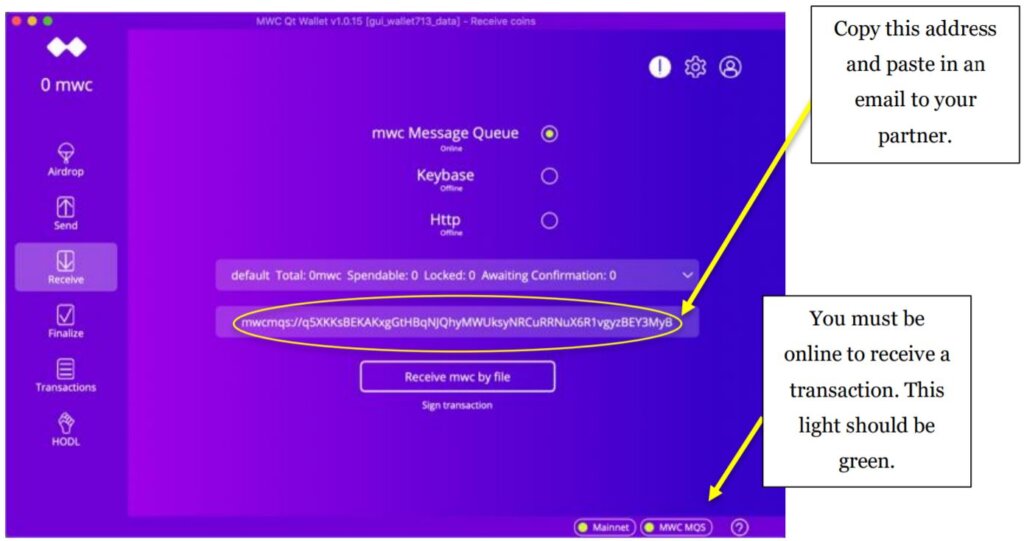

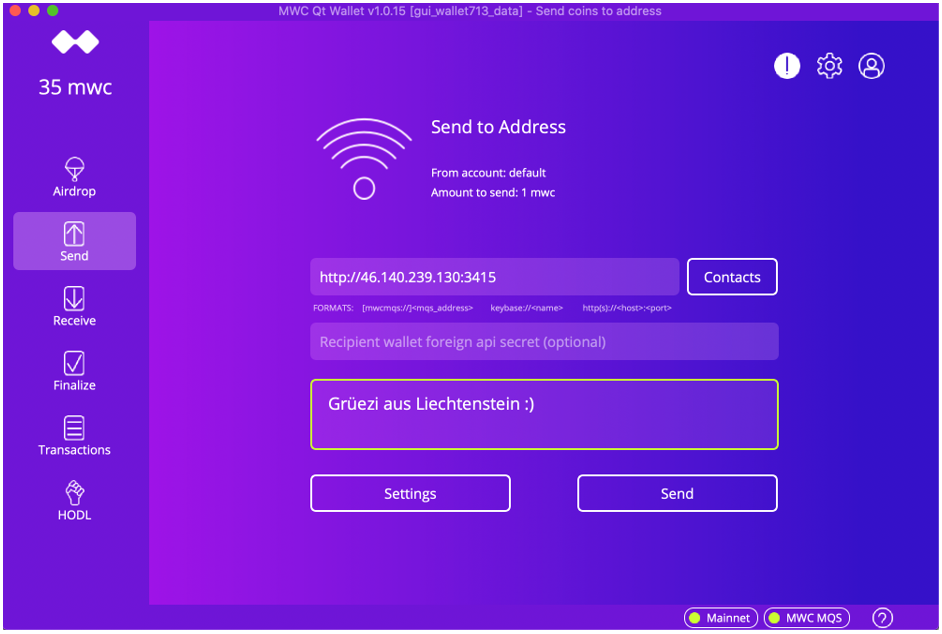

The MWCMQS Method

Sending and receiving via the MWCMQS method will be most similar to a Bitcoin transaction. However, both the sender and receiver must be able to interact. This means the receiver must be online and listening with the address the sender is attempting to send to. This means you cannot just provide an address and turn off your laptop and go to bed like you can with BTC, LTC, etc.

To get started, open up the wallet and click “Receive” in the left-hand menu. Copy the mwcmqs:// address and send it to your partner. Sending via email or a messaging application is fine. In order for your partner to send you a transaction, your wallet will need to be online and listening (in the lower right the MWCMQS will need to be green) for that specific address.

Once your sender copies in the address that you send them, they can paste in the address on the wallet by clicking on the “Send” option in the left-hand menu. They can also send a message along with the transaction.

The File Method

Although the MWCMQS method is the easiest method for people that used to send Bitcoin transactions, the most private way to send MWC transactions is with the File method.

Sending and receiving by File requires five steps.

The sender creates the transaction and generates a .tx file

The sender provides the .tx file to the receiver

The receiver signs the transaction and generates a .tx.response file

The receiver provides the .tx.response file to the sender

The sender signs the transaction and broadcasts it to the network by finalizing the transaction

To get started, a sender will attach the mwc-payment.tx file to an email and then email this file to the receiver. This covers the first two steps. The receiver must then download the file from the email and then go into their MWC wallet and insert the file. Depending on your operating system, a little box may pop up when you click “Receive mwc by file.” This box will ask you for permission to access files in your Downloads folder. Once you click “OK” you will need to find the specific .tx file that the sender sent you.

Then the receiver needs to email back a new mwc-payment.tx.response file, which will constitute the next two steps. Then, the final step will be finalizing the transaction on the sender’s side. The sender and receiver can check the transaction on the block explorer: https://explorer.mwc.mw/. By clicking in the upper right corner on the Gear, MWC users can see their transactions on the blockchain by double-clicking on the output. What is cool is that only you and the person you transacted know how many MWCs are associated with that particular output.

Fireside with the MWC Team

Are you inspired by Austrian economics? If so, please who is your favorite Austrian economist? What is your favorite book on Austrian economics? And, last but not least, what is your favorite quote?

Yes, we like the Austrian school of economics because of its objectivity. It is about understanding how things are in contrast to how we many want them to be. Mises, Rothbard, Gordon, Block and others have produced some excellent work. Human Action is a foundational text in the area. We are monetary sovereignty maximalists and are big fans of any means that help accomplish that purpose or aim whether that comes in the form of gold, silver, Bitcoin, Dogecoin, MWC or whatever. As Mises explained, “It is impossible to grasp the meaning of the idea of sound money if one does not realize that it was devised as an instrument for the protection of civil liberties against despotic inroads on the part of governments. Ideologically it belongs in the same class with political constitutions and bills of rights. The demand for constitutional guarantees and for bills of rights was a reaction against arbitrary rule and the nonobservance of old customs by kings. The postulate of sound money was first brought up as a response to the princely practice of debasing the coinage. It was later carefully elaborated and perfected in the age which—through the experience of the American continental currency, the paper money of the French Revolution and the British restriction period—had learned what a government can do to a nation’s currency system… Thus, the sound-money principle has two aspects. It is affirmative in approving the market’s choice of a commonly used medium of exchange. It is negative in obstructing the government’s propensity to meddle with the currency system.”

You mention that the MWC team are invested in Bitcoin. Are you invested in any other privacy-related coins?

We do not know. The MWC Team is composed of a significant number of people who are united by the purpose or aim of monetary sovereignty. And part of that means that what each of us does with our own money is our own business and not the business of others.

What do you say to the argument, “Only criminals use privacy coins?”

Without the ability to keep secrets, individuals lose the capacity to distinguish themselves from others, to maintain independent lives, to be complete and autonomous persons. This does not mean that a person actually has to keep secrets to be autonomous, just that she must possess the ability to do so. The ability to keep secrets implies the ability to disclose secrets selectively, and so the capacity for selective disclosure at one’s own discretion is important to individual autonomy as well.

Secrecy is a form of power. The ability to protect a secret, to preserve one’s privacy, is a form of power. The ability to penetrate secrets, to learn them, to use them, is also a form of power. Secrecy empowers, secrecy protects, secrecy hurts. The ability to learn a person’s secrets without his or her knowledge — to pierce a person’s privacy in secret — is a greater power still.

We want to help humanity exercise their unalienable right to secrecy, or in other words, to have you and your property left alone. This is even more important now that we have tools like Bitcoin and MWC which are based on public-private key encryption.

Who is the target demographic for privacy coins? What do you think is the average demographic of a privacy coin user? I mean, do you think that privacy coins are primarily used in developed countries or in developing countries? Do you think they are used by relatively rich people or relatively poor people?

We are not really sure since we have not done much market analysis besides personal introspection. For the most part, we have been significant Bitcoin holders for many years but are cognizant of its characteristics and how it does not necessarily perform very well all of the jobs we may want it to. We saw the opportunity to build a product we wanted to use ourselves, extremely scarce ghost money, and the other monetary entrepreneurs in the marketplace were currently neglecting that market demand or choosing design characteristics we did not find compelling in a product. So we built the type of monetary product we wanted to use ourselves.

What are the main points on the roadmap for MWC during the next 12 months?

Fully distributing the initial stock via the unclaimed airdrop fund and HODL program, additional exchange integrations, greater market liquidity, additional Grin rebases, release a mobile wallet, atomic swaps, a decentralized exchange, multisig, Lightning Network and other features.

Conclusion

The MWC network was launched in November 2019 and has functioned flawlessly with 100 % uptime. The MWC team considers the protocol ossified and currently sees no need for a future hard or soft fork unless a defensive action were required to protect the network. We feel the MimbleWimble sector may be neglected, to contain significant disruptive technological innovation potential, and there may be significant information asymmetry in the market. This type of technology is especially important in the age of surveillance.

Privacy is an important right that we must protect at all times. But not only authoritarian states can attack our privacy, other malicious actors can also use the knowledge about our financial situation against us. For this reason, Privacy Coins and other privacy options might play an essential role in the future of digital money.

One of the main reasons for Bitcoin’s success and popularity, is its trustless design. Instead of trusting humans with clearance and settlement of financial transactions, Bitcoiners opt to trust software protocols. What was particularly revolutionary about Bitcoin was how the network used proof-of-work to stop double-spending attacks and how anyone around the world could validate new transactions and store a copy of the database’s history. Imagine if Credit Suisse or Bank of America not only allowed anyone to see their entire database of transactions, but also allowed anyone to vote on the validity of new transactions.

However, over time becoming a validating node on the Bitcoin network became increasingly expensive and exclusive because of the size of the Bitcoin blockchain. Without heavy investments in computing power, relaying new transactions and storing a copy of the database is impossible. A newcomer to the Bitcoin blockchain needs to spend approximately one week downloading the 277-gigabyte database of existing transactions in order to participate in the validation of new transactions. However, the “blockchain” associated with Bitcoin is only one type of distributed ledger database architecture. There are also other kinds of distributed ledger databases, such as IOTA’s directed acyclic graphs that we explored in the June 2018 edition of the Crypto Research Report. This article discusses a different type of distributed ledger architecture called MimbleWimble that has specific advantages and disadvantages compared to Bitcoin’s blockchain.

What Are Privacy Coins?

In a recent report by the European Union Blockchain Observatory and Forum called, Legal and Regulatory Framework of Blockchains and Smart Contracts, the authors explicitly state that regulators should use blockchain explorers to track transactions and to find out personal information about the senders and receivers of Bitcoin transactions.

While not always identifiable at the moment of the transaction, given enough time and effort, many parties to a transaction can be unmasked. Therefore, at this point there is no question of total impunity for blockchain actors.

Thirdly, however, it cannot be denied that some privacy-focused blockchains, for example Monero or ZCash, can provide bad actors with effective tools for true anonymity. It is important to note that in practice anonymous transactions are currently not widely used: Bitcoin and Ethereum, the most popular platforms, do not support anonymity.

Governments also try to discourage the use of anonymization techniques in blockchain networks by, for example, imposing AML rules, thereby policing the gateway between the worlds of cryptocurrencies and fiat money (see also next section). That said, while anonymisation does not pose a significant enforcement risk on public permissionless blockchains at the moment, should the use of anonymous blockchains spread significantly, it could become a problem.

It seems that providing states with identification tools (potentially under the control of courts or through the private sector on a payment basis) should be a minimum condition necessary for a state’s ability to enforce the responsibility and thus to ensure the impact of the law on human behaviour in the blockchain space.

Many market participants consider fungibility a characteristic of good money. Bitcoin lacks fungibility, which means bitcoins can be traced to their initial transaction when they were mined. Privacy coins are coins that attempt to improve upon Bitcoin’s privacy by hiding the amounts that are traded and the wallet addresses involved in the transaction. Privacy coins use technologies such as coin mixing and confidential transactions. The largest privacy coins include Dash, Monero, Zcash, Grin, Beam, and MimbleWimbleCoin. In 2014, Dash was launched, and it was the first privacy coin on the market. Dash gives each user the option to make each transaction private or not. Dash’s technology uses coin mixing to obscure information about the sending and receiving addresses, and only 2 % of Dash transactions use Dash’s privacy option. The rest of Dash’s transactions are just as traceable as Bitcoin transactions. A few months after Dash came out, a new privacy coin called Monero was released to the market. Unlike Dash, every Monero transaction is private. Blockchain explorers don’t see the amounts being sent in Monero transactions. Monero introduced ring confidential signatures, which provide very strong privacy for Monero users. A few years later, Zcash came out in 2016, and then more recently, in 2018, the MimbleWimble base layer coins Beam and then Grin came out.

However, the developers of privacy coins face design choices that each have unique tradeoffs. For example, Monero is more private than Dash because the transaction amount is hidden, but Monero is less scalable because it takes more resources to run a full node, which makes it less censorship-resistant. Another tradeoff is between being able to prove a coin is scarce and having privacy features. Blockchains that obscure the amounts being transacted have difficulty determining the total amount of coins in circulation. In a recent interview on the Academic Blockchain Podcast with the Chief Technology Officer of Ledger, Demelza Hays discussed Zcash’s “inflation bug.” Zcash’s inflation bug makes it impossible for anyone to actually calculate the total amount of coins in existence. This means that there could be an infinite amount of coins in existence, which goes against one of the pillars of a good money in the digital age, namely, scarcity. However, the MimbleWimble protocol uses mathematical proofs involving excess values of intermediate transactions to prove that all debits and credits in the ledger sum to zero.

But what is MimbleWimble? In 2016, an anonymous person released the MimbleWimble protocol to increase Bitcoin’s scalability and privacy. MimbleWimble is a way to sign and validate transactions without needing to validate each historical transaction and to include the inputs of a transaction into a new transaction’s hash. This drastically reduces the size of the blockchain. Proponents originally proposed MimbleWimble as a sidechain or soft fork to Bitcoin; however, the current implementations of the MimbleWimble protocol are by new cryptocurrencies that created new blockchains including Grin, Beam, and MWC, that elegantly apply MimbleWimble in the base layer.

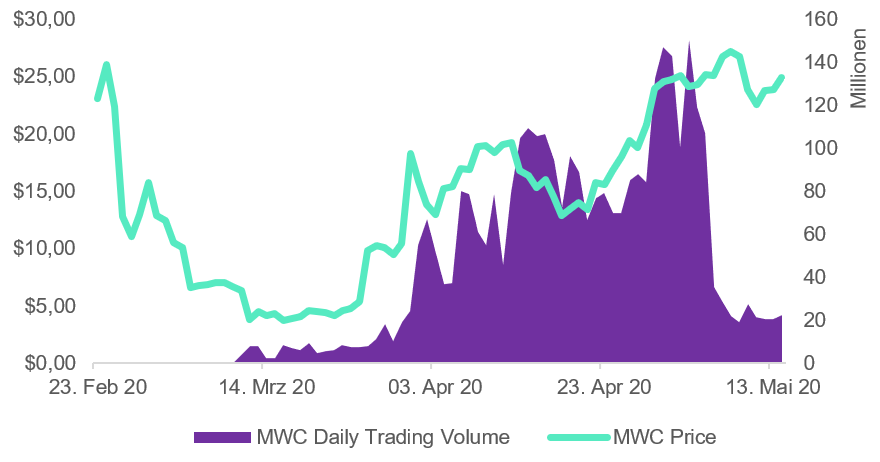

During 2019 and into 2020, much of the MimbleWimble hype had died down along with the market caps of Grin, currently about $19 million, and Beam, currently about $16 million. MimbleWimbleCoin (MWC) forked from Grin in November 2019 and hit a low of $0.25 per coin with less than a $2 million market cap in early December. However, since December, the market cap of MWC has grown 6,100 %. The MWC market cap is currently around $125 million and has been consolidating over $100 million for most of the past two months. By market cap, MWC is currently the 3rd largest privacy coin behind Monero and Zcash and the 13th largest proof-of-work coin behind Bitcoin Gold and Decred. MWC is currently traded on Hotbit, Bitforex, Whitebit, Trade Ogre, and Toktok.

The two ideas that form the basis for MimbleWimble stem from the Blockstream co-founder Gregory Maxwell’s work on “Confidential Transactions” and “CoinJoin.” Confidential transactions use encryption so the public blockchain doesn’t show the amount of coins being sent or received in a transaction. For example, in Bitcoin, anyone can see the amount of Bitcoin that is sent in each transaction. However, in MWC, the public cannot see how much is being sent even though verification can be done of adherence of the transaction to the consensus rules to, for example, prevent double-spending and enforcing the total number of coins. The second innovation that the MimbleWimble protocol uses is CoinJoin. This means that multiple transactions in the network are merged into one transaction so that blockchain forensics cannot discern the real sender and real receiver of a specific transaction.

Figure 3: The Newest Privacy Coin on the Market: MimbleWimbleCoin

However, there are disadvantages of the MimbleWimble protocol as well. For example, the MimbleWimble protocol doesn’t allow extensive scripting. Fortunately, there has been significant research done since then, and with MimbleWimble these types of scripts and applications are possible: Multi-signature transactions, time locks, atomic swaps, and hashed time-locked contracts which are the building block of payment channels and Lightning Network. Another large disadvantage of coins that use the MimbleWimble protocol including Grin, Beam, and MWC is that currently these blockchains aren’t widely used. Until more people use these coins and more people send transactions, the benefit of privacy from their use may be limited.

In the coming week we will take a closer look at MimbleWimble and also talk to the developers behind MWC. In doing so, we will also look in detail at how a MimbleWimble transaction actually works and what benefits it brings.

Tether has traditionally been seen as an on-ramp for investors looking to acquire larger quantities of Bitcoin, but the continued increase in the market capitalization of Tether is not necessarily the result of an increase in that demand. Instead, a different phenomenon seems to be emerging: There is a demand for tether as a value in and of itself. This is due to the fact that the Stablecoin is widely used as a settlement vehicle for arbitrageurs between crypto trading exchanges.

Over the past few years, the trading exchanges for cryptoassets have become more professional, which has also made the arbitrage business more professional. Arbitrage is being conducted with ever-larger sums of money – a stable settlement currency such as the USDT seems predestined for this. Tether is also used for arbitrage purposes by individual traders. If the Bitcoin price falls, these players switch their funds into the stablecoin in order to minimize losses and buy back in at a lower price.

Having a stable currency that is denominated in dollars lets you handle your books with more ease. So, as a matter of fact, there has been a tetherification of the crypto exchange industry. With exchanges, Bitcoin has been supplanted by Tether as the base currency. Several exchanges like Binance, OKEx, or Huobi have even launched Tether-denominated futures products.

Over the last couple of months, Tether supply on exchanges has been growing significantly. It’s not only exchanges that make use of Tether’s stable characteristics, USDT is also used for arbitrage purposes by individual traders. If the Bitcoin price falls, these players switch their funds into the stablecoin Tether in order to minimize losses and buy back in at a lower price.

Figure 21: During the Last Two Years, Tether Supply on Exchanges has Grown from the Millions into the Billions.

But not only arbitrage trading between crypto exchanges but also the moving of funds between individual countries is facilitated by a stablecoin like Tether. It is well known that one of the first major uses for Bitcoin was to circumvent capital controls. The first major price increase at the end of 2013 is said to be mainly due to Chinese people moving their savings out of the country.

However, the volatility of Bitcoin has always been a thorn in the side of capital refugees. And indeed, little seems to be gained by taking your capital out of the country only to see it be eaten away by Bitcoin’s volatility during the trade.

With the launch of Tether, new opportunities for capital flight have suddenly opened up. It is therefore understandable that USDT has been discovered as a killer application. Tether is used as a cross-border crypto dollar, especially by Chinese traders and business people exporting to Russia.

Everyone Wants US Dollars

There is a reason why Chinese businessmen hold a dollar-denominated stablecoin. The US dollar is currently the global reserve, reserve and trading currency. All major commodities are settled in US dollar, which is why it now accounts for 4.7 times global imports and 3.1 times global exports. For non-US companies it therefore often makes more sense to invoice in US dollars.

But it’s not only invoices that are issued and settled in US dollars. Companies around the world have nearly 60 trillion US dollar-denominated debts. This creates an ongoing demand for US dollars to service the debts of emerging and developing countries, which will not leave their currencies unaffected. The latter currencies are likely to depreciate against the dollar, which is bound to result in increased capital controls.

The most recent example is Lebanon. Local banks there are currently in the middle of a fight against capital flight, which is why restrictions on foreign currency withdrawals, especially for US dollars, have been tightened. Tighter controls on capital movements are likely to increase not only in underdeveloped countries, but the eurozone could also become more restrictive in this regard in the foreseeable future.

In contrast to the Japanese yen and the Swiss franc, which as currencies still enjoy the character of a safe haven, demand for the euro correlates mainly with the demand for exports from the eurozone. The sooner the euro liquidity created by the European Central Bank’s ultra-expensive monetary policy exceeds international demand for the euro relative to the dollar, the faster the former will lose value. Tighter capital controls to support the euro would primarily affect European banks. They still carry large US dollar positions on their balance sheets. Without having sufficient US dollar deposits, they need to have open channels to access US dollars at all times. Tighter capital movement controls would certainly be an obstacle in that regard.

The use of crypto dollars, especially Tether, might serve as a helping and welcoming solution. Not only can potential capital controls be more easily be circumvented, but transactions using crypto dollars are generally easier to initiate and process than those using the traditional financial infrastructure.

The demand for Tether which is not an equal demand for Bitcoin should, therefore, already satisfy several real needs today. Apart from the use cases described above, particularly the increasing demand for dollars in a world of increasing capital controls will accelerate a sort of “hyper crypto dollarization.” Ironically, what we have been witnessing is the dollarization of public blockchains, which is bound to grow in next couple of years.

Since the beginning of the year, the market capitalization of the Stablecoin Tether (USDT) has risen significantly. This once again raises various questions that have caused some controversy around Tether in the past. What is the extent to which Tether is backed by real US dollars? Is there a correlation between the market capitalization of Tether and the price of Bitcoin? For what purpose is Tether mainly used?

In September 2018, US Tether (USDT) reached a temporary high in market capitalization of just over $ 2.8 billion. By mid-November, market capitalization then dropped to below $2 billion. This correction was followed by a fall in the price of Bitcoin to almost $ 3,000 per Bitcoin shortly before the end of the year.

Today, the price of Bitcoin is once again higher, and the market capitalization of Tether has also risen continuously since then to over $8 billion. Not only has the outstanding amount of Tether hardly ever fallen, not even temporarily, but the issuance rate of new Tether has also shown sudden, erratic increases since the beginning of this year; a total of three in number, each greater than the previous one.

As one of the big black boxes of the crypto world, many secrets and speculations surround Tether, further fueled by these abrupt growth spurts in market capitalization. Aside from the rumors and speculation, USDT is still regarded as a so-called on-ramp for investors to easily and quickly invest in Bitcoin.

It’s a fact that Tether has been used as a gateway into the Bitcoin world. However, if Tether was an on- and off-ramp, then the market capitalization of Tether would in theory have to fall every now and then, because USDT would have to be burnt at intervals by the Tether Treasury when holders cash back out into fiat or go into Bitcoin. Since, the market capitalization of Tether has risen steadily over the past 18 months without significantly falling even once, this suggests that Tether is essentially not acting as both on-and off-ramps.

Figure 19: Negative Correlation Between Change in Tether Supply and Bitcoin Price

The argument against this is that the demand for Bitcoin is very volatile. During the last two years, there have been repeated periods when Bitcoin’s price fell, while Tether’s market cap remained the same or even went up. If USDT were used primarily as an on- and off-ramp, its positive correlation with Bitcoin would have to be much stronger. This isn’t the case, especially since there are even indications that the correlation is negative. This leads to the conclusion that something else more serious is afoot.

Alternative Explanation Sought

For example, some market observers suspect that USDT is being created without collateralization. So, Tether would be created specifically by Tether Limited and its parent company BitFinex and held in fractional reserves in order to drive up the Bitcoin price, so the argument goes.

This way the critics argue that BitFinex is trying to generate excitement among retail investors, which would then turn into a hysteria of FOMO leading up to a new Bitcoin bull run. This is how some analysts explain the fact that on May 14, a few days after the Bitcoin-halving, the Tether market capitalization suddenly rose from just over $6 billion to almost $9 billion.

What sounds like a conspiracy theory to some, others consider to be a fact: After all, the two companies BitFinex and Tether Limited would have strong incentives to run such games. As the New York Secretary of Justice pointed out, only about 70 % of outstanding Tether is secured by cash and cash equivalents. This hole when it comes to collateralization, according to the skeptics of Tether, could of course be filled up step by step if Bitcoin stabilizes at a higher level supported by private investors. The collateralization that BitFinex partly holds in Bitcoin as well would then have more value that could be sold for dollars and improve the reserve ratio.

Tether as a Savior

Another hypothesis to explain the abrupt rise in Tether market capitalization on May 14 is that BitFinex is going out of their way to secure the survival of certain miners with USDT loans. Bitcoin miners today operate highly specialized ASIC processors, of which two different ones are currently in use: the Antminer S9 and the Antminer S17.

The major difference between these two mining hardware devices is mainly their different efficiency. Although the S17 has about 50 % higher power consumption than the S9, a miner using the former achieves a 300 % higher hash rate. As a result of this higher efficiency, Antminer S17 accounts for a much higher share of Bitcoin mining, at just over 61 %. The use of the S9 type is just over 38 %.

And it is precisely these miners, so the argument goes, that are dependent on support, as they have become unprofitable after the halving. However, in order to not have to empty out their Bitcoin treasuries and generate downward pressure on the Bitcoin price, these miners could be buying time with USDT loans – time to renew their hardware equipment that had become unprofitable.

Speculations and theories of this kind always sound tempting. It is also difficult to refute them completely. But it is just as difficult to provide definitive evidence. In the end, it is argument against argument.

What stands against the BitFinex miner thesis is the fact that miners today are farsighted, long-term invested players. As rational players in a very competitive, highly innovative and little-regulated field, it can be assumed that precisely those miners with older Antminer S9 have taken precautions. They could have moved to a location with much lower electricity costs so that their Antminer S9s are still profitable even after the block reward was halved.

Again, there is friction and uncertainty in the real world. Not knowing the unpredictable could have caused miners to miscalculate long-term contracts with electricity providers, which is why they cannot easily relocate mining farms overnight. It is and remains a fact: We can only speculate about what is really the case.

Many years ago, observers in the crypto scene voiced their suspicion that the Stablecoin Tether (USDT) was not 100% covered by actual US dollars. While concrete information confirming these suspicions has repeatedly been the subject of discussion in the crypto media in the past, it is not certain to what extent this information can be transferred to the current situation. Due to the strong increase in Tether since the beginning of the year, it should be avoided to postulate a 1:1 correlation to older news.