Summer 2017 was the summer of Initial Coin Offerings. ICOs and token sales in the crypto sector have seen explosive growth. In 2017, more money has been raised in this market than through venture capital or angel investments. However, this new market is a minefield for investors. Although no ICO regulation exists at the moment, that could soon change. This chapter focuses on initial coin offerings, bubbles, scams, and – of course – regulation.

Who still remembers Pets.com? The rise and fall of this Internet company has become a symbol of the dotcom bubble at the end of the 1990s. The technological possibilities offered by the Internet fired up the imagination of investors quite a bit at the time. For a little while it was considered received wisdom on Wall Street that a good-sounding domain name was all it would take to guarantee success. Pets.com actually had more than just a domain name: it had a business concept, more than 300 employees – and an already existing network of storage facilities across the US. Amazon was an early investor in this provider of pet supplies. It seemed that nothing could go wrong. And yet, Pets.com eventually failed spectacularly.

The online store went public in 2000 – with great success. 82 million USD were raised on the first day. But a mere nine months after the initial public offering (IPO) it was all over: Pets.com was bankrupt. The famous domain name was later acquired by competitor Petsmart. Within just 268 days, the stock plunged from 11 USD dollars to 19 cents.

Pets.com with ticker IPET went from $11 to $0.19 per share within nine months. Source: CNN Money

Pets.com joined the game too late. Other web sites, such as social media forerunner TheGlobe.com, initially had outstanding success. The stock skyrocketed by 600% on its first day of trading. But reality would soon intrude: “The rules of the game changed as soon as we went public”, co-founder Stephan Paternot wrote in his book A Very Public Offering: A Rebel’s Story Of Business Excess, Success, And Reckoning, “It was not about developing our business model, but increasing shareholder value. We were doing well if our stock went up and badly if it went down.”

A mere 20 years later, history seems to be repeating. This time it is blockchain technology that stokes the imagination of investors. The ingredients are almost the same as back then: once again a new technology appears to offer seemingly revolutionary possibilities. Once again, no sphere of life seems likely to be untouched by it. And once again millions are rushing in as though nothing could possibly go wrong.

A New Market is Born

However, there are decisive differences as well. The blockchain sector based on the technology underpinning the cryptocurrency Bitcoin is to this day an almost hermetically sealed market. Companies don’t list on the stock exchange, they don’t conduct an IPO but an ICO – an “initial coin offering”. In contrast to the dotcom mania, an entirely new market has sprung up – which is to date de facto unregulated. Neither investment banks nor hedge funds are the driving forces of the mania but private investors who made a lot of money in recent years as the prices of Bitcoin and other cryptocurrencies massively increased.

Only recently, eight years after Bitcoin first surfaced, the interest of investment bankers and hedge fund managers has been piqued. Goldman Sachs analysts have been giving consideration to Bitcoin since July. Unconfirmed reports suggest that at least 70 different hedge funds are currently entering the market.

ICOs have grown explosively in number and success this year as well. Goldman Sachs states that more money was raised via these instruments since the summer months than internet start-ups received from venture capital firms and angel investors. The precise figures are open to debate though. Goldman Sachs estimates that around USD 300 million were raised in ICOs this July. The New York Times even reported a figure of USD 665 million, which various projects were supposedly able to raise in this month alone – referring to data collected by industry journal Tokendata.io.

These statistics are moreover distorted by the extreme price volatility in cryptocurrencies, as ICOs are not based on dollars but on Bitcoins or more recently increasingly ether as well, the currency of the Ethereum network. As a result of this, a company that made an ICO a year ago may possibly have more than a hundred million dollars in the form of ether coins at its disposal – provided it didn’t exchange the cryptocurrency for dollars right away. The only thing that can be stated with certainty is: this new form of initial funding for start-ups is currently undergoing a boom that surpasses anything we have seen in the blockchain sector up to this point.

What is an ICO Actually?

The term ICO is of course an allusion to the established term IPO. There are in fact a number of similarities between these fund-raising procedures. Both aim to collect money from investors who have become aware of a potential profit-making opportunity and are prepared to take risks. Two important differences were already mentioned: ICOs are mainly the domain of inexperienced retail investors. In addition to this, contrary to stock exchange listings, ICOs are neither precisely defined, nor are they regulated. Lastly, only very few ICOs actually involve the sale of stakes in a company in the form of shares, but rather so-called tokens, the exact purpose of which can vary widely. It therefore seems to make more sense to regard ICOs as a new form of crowd-funding rather than confusing them with traditional stock market listings.

Often the people offering ICOs specifically stress that the process should be defined as a “token sale”, a “donation”, or a “crowd sale”. This is designed to prevent future problems with regulators. A number of the latter, such as the SEC in the US, have already signaled that they plan to examine ICOs closely in the near future. Should the sale of ICOs be equated to the sale of securities, the same laws and tax rules that apply to the stock market could be applied to them as well. Currently no binding rules exist. Many ICOs already exclude U.S.-based investors though in order to forestall potential future legal problems.

“It can be compared to Kickstarter”, said Julian Hosp in a private interview we conducted during fall of 2017. Together with three partners, the Austria-born entrepreneur has founded the start-up company TenX in Singapore. TenX has developed a prepaid debit card which can be connected with a cryptocurrency wallet on a smart phone. “We want to make cryptocurrencies spendable”, Hosp explains. TenX raised the equivalent of USD 80 million within seven minutes in a token sale it conducted this summer. A special decentralized structure was developed in collaboration with a law firm so as to make the token sale immune to legal challenges.

With an all-time high market cap of almost $9 million, Putin coin’s sole purpose is to pay tribute to Putin and the people of Russia. Source: Twitter.com/putincoinput

The token itself, which trades under the symbol PAY, has no purpose beyond its “kickstarter” function. Soon it is supposed to be possible to use it for payments via the TenX app and debit card. With respect to his opinion on ICOs in general, Hosp isn’t exactly mincing words, neither in his YouTube videos, nor in interviews: “95 percent are scams and pure rip-offs. It probably won’t be long before many of these projects go under. How many of them have actually a useful sphere of application?”

Beware of Scams

Analysts at Smith and Crown are listing several dozen upcoming token sales and ICOs scheduled to take place in the coming months: the ideas range from blockchain-based adult entertainment to the storage of wills – also on the blockchain. According to Smith and Crown, the history of ICOs can be traced back to 2013. At the time token sales were mainly organized through the Bitcoin Talk forum. The first ever ICO is said to have been conducted for the purpose of funding Mastercoin, a mega-protocol that was supposed to create additional features for Bitcoin. The Mastercoin ICO raised 1,000 Bitcoin. The cryptocurrency project NXT also originated via an ICO conducted through the Bitcoin Talk forum. In 2013 and 2014 numerous further ICOs followed, some of which were the work of scammers.

Floyd Mayweather in July became one of the first high-profile celebrities to endorse an ICO. Source: Twitter.com/floydmayweather

That is the other side of the coin, so to speak. The growing success of ICOs and the ever-larger amounts of money involved in these offers continue to attract numerous criminals to this day. In summer of 2017, the Enigma project became victim of an attack by hackers. The hackers altered the web site of the project and entered a false wallet address to which users were supposed to send money to purchase Enigma tokens. The damage reportedly amounted to half a million dollars. How big the long-term damage to Enigma’s reputation will be remains to be seen. The hackers took advantage of the hype accompanying the project and the greed of potential investors.

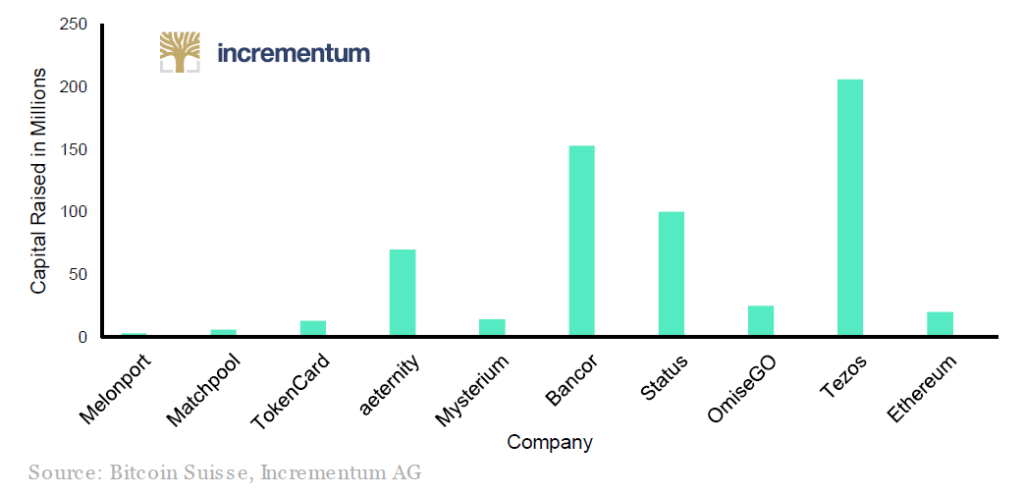

Similar events occurred also on occasion of the ICO of Israeli project Bancor, which raised more than 150 million USD in June 2017. In this case false wallet addresses were distributed via social media, causing quite a few gullible investors to send money to them that is now lost forever.

The Role of Ethereum

The reason why ICOs have gathered significant steam this year has a name: Ethereum. The number two cryptocurrency by market capitalization was itself created by a token sale. Bitcoin equivalent to “only” USD 18 million were raised at the time. Ethereum is more than a currency, it is a platform providing a blockchain other enterprises can use for their own purposes. Moreover, Ethereum offers a feature called “smart contract”, which inter alia makes it possible to automatically exchange ether tokens for other tokens. That is precisely what happens in a “standard” ICO. Users send their investment in form of ether coins to an ether wallet address and in return receive the tokens issued by the project they want to invest in. The ICO of Bancor took place on the Ethereum network and was so successful that the latter was overloaded for more than a day.

A typical blockchain product roadmap showing progression from idea to implementation. Source: OxFina.com

What purpose the different tokens distributed by their inventors serve varies widely. There are several attempts to create tokens that will make it possible to receive passive income – such as, for example, dividend payments. In view of the looming threat of market regulation, this trend was at the very least hampered of late. Other tokens, such as the one issued by EOS, which will leave its ICO up and running for an entire year, are merely placeholders for the “real” token that will be traded on the still-to-be-developed “real” EOS blockchain.

Similar to many ICOs, participants in the EOS ICO invest merely in an idea and a team, not a ready-made final product. Until the EOS blockchain is ready, the EOS token remains an ETH token, which trades on the ETH blockchain. The highly successful token of Thai company Omise is an analogous case. Omise distributed an Ethereum token by the name of OMG. The token has in the meantime become tradable as well. Omise ultimately wants to develop its own blockchain though and exchange the tokens at a later point in time.

Investors as a rule don’t necessarily have to purchase a new token during the ICO phase, as most of them quickly tend to become tradable at cryptocurrency exchanges. At this juncture one would do well to remember the remarks of the CEO of Globe.com. Similar to start-ups at the time of the dotcom bubble, the survival of new ICO-funded blockchain enterprises should actually not depend on the prices at which their tokens are trading. On the contrary: many have raised enough money to be able to pursue their work for years without funding pressures. Alas, then as now, investors definitely tend to judge a project’s success by watching prices. That leads to a situation in which communication and public relations appear almost as important as the actual technological progress that is achieved – particularly in cases in which several projects in a specific sector are working toward the same goal.

The First Large ICO Failed

Thus, several companies are currently working on building supercomputers based on blockchain technology, on the introduction of cryptocurrency debit cards, or the creation of blockchain-based cloud storage solutions. These are just three examples of spheres of application in which blockchain enterprises want to gain a foothold. A number of projects in the health care, travel and gambling sectors are underway as well. An additional complication is the question what role the token plays in a company’s business concept. It is, for instance, possible that a token has to remain relatively cheap in order to support a project’s functionality.

As of December 2017, Facebook’s market cap is twice the size of the entire cryptocurrency market. Source: howmuch.net

Ether itself of all things is subject to a recurring debate in this context: is ether actually a currency, or is it rather the fuel that is burned on behalf of other projects? Moreover, in the case of some projects it cannot be ruled out that their developers will flood the market with additional coins through a new ICO, which would inflate the total outstanding amount of the tokens concerned. In view of the sheer confusion and complexity of the several hundred ICOs in the pipeline for this year and next, interested investors will have no choice but to engage extremely thorough due diligence wherever possible – and to rather pass on investments if it isn’t possible.

Just how dangerous an ICO investment can be is illustrated by the history of DAO. It was the first large-scale ICO on the Ethereum network, which raised around USD 130 million in May of 2016 already. Alas, hackers exploited a security flaw and were able to steal tokens valued at USD 50 million.

Regulatory Authorities are Coming

The event had two important consequences: a so-called hard fork of the Ethereum network was implemented in order to restore the stolen coins. Ever since, both Ethereum and Ethereum Classic exist. The DAO disaster was also the reason for the US regulatory agency SEC to begin a review of the issue. The wheels of justice grind slowly. In the summer of 2017, the SEC issued a statement asserting that the stolen DAO coins should have been registered as securities with the agency.

The importance of this decision has to be equaled with that of the CFTC to classify Bitcoin as a commodity, similar to gold. SEC decision could have an enormous impact on the blockchain industry. Currently ICO issuers are still careful and will rather circumvent the US market in order to avoid becoming a target for regulators. On the other hand, if tokens are treated as securities, an important door will be opened as well.

The reason is that a sufficient degree of market regulation is a precondition for an asset to become accessible to institutional investors, banks, hedge funds and other large financial market participants. A blockchain asset regulated by the SEC could one day also become acceptable as collateral in the capital markets, which would give the importance of cryptocurrencies a massive shot in the arm.

The same applies to the giant Chinese market. The PBoC recently “prohibited” the ICO business as practiced in recent years, which was followed by a brief panic that led to a sharp sell-off in Bitcoin. But even in Beijing the next step is likely to consist of issuing regulations specific to ICOs, which should ultimately boost confidence in the sector and help it to attract more investment.

Conclusion: enormous potential remains

It is therefore probably too early to dismiss the ICO-mania of the past two years as a bubble. Over the medium term there is undoubtedly a danger that the crypto-sphere could be struck by a medium-strength or even very strong earthquake, which could lead to a noticeable shift in the valuation of Bitcoin and other alt-coins. But the potential for the market to become much bigger seems quite obvious as well. Thus, the total market capitalization of all blockchain assets stood at less than USD 260 billion at the end of November 2017.

Although the market capitalization of cryptocurrencies has grown nearly ten-fold since last year, the market remains very small compared to traditional financial assets. The market cap of Apple alone is almost five times larger than the entire sector. The combination of a maturing market, the slow emergence of more specific regulations and the rapidly growing interest on the part of investment banks and hedge funds leads us to conclude that the blockchain mania probably still has a lot of room to grow – perhaps it hasn’t even really started yet. Only once the authorities have indeed leveled the regulatory playing field between blockchain assets and other securities will it be possible to truly compare the market to traditional financial markets.

The same applies to comparisons with the dotcom bubble: between 1997 and 2000 a total of 522 dotcom companies were listed, raising more than USD 43 billion in the process. On the day the Nasdaq Composite peaked it had reached a total market capitalization of USD 6.6 trillion – level that was of course hopelessly exaggerated. However, one must not forget that despite duds like Pets.com and Globe.com, numerous companies involved in this bubble later more than fulfilled their promise – such as, for example, Amazon. Amazon disrupted the retail business by offering an online shopping platform with customer reviews, fast shipping, and free returns. Similarly, the blockchain technology may change the way we store value and pay for goods ands services.

Investors in the late 1990s were not wrong with their assessment of the future – they were merely too early. The required infrastructure didn’t exist yet. If one uses the Internet as a model for the prospects of the blockchain and believes that this technology will have a comparable revolutionary impact, investors can take steps to hedge themselves to some extent against the risks associated with a bubble: they only have to buy the Amazon equivalents of the sector and avoid falling for empty promises. That is of course easier said than done.

{kind=link}