For several years legacy financial

companies have started to integrate blockchain technology in their existing

business model. While digital-native and decentral-native start-ups have been

able to directly build on public blockchains like Cosmos, Tezos or Ethereum,

legacy finance firms with their complex IT infrastructure started to test

private blockchains in order to become familiar with the technology, remain regulatory

compliant and experiment in a controlled and surveyed environment with their

clients. R3 Corda for example has become the primary permissioned blockchain

platform for the legacy financial service industry.

While many companies believe that this

is the ultimate goal, several banks, like Goldman Sachs for example, have

already left the Corda platform. They belonged to the early joiners, but

already left in 2016. However, just last week, Goldman Sachs and Citi announced

to conduct the first blockchain equity swap on an Ethereum inspired platform. To conduct

this swap, they are collaborating with a new market player called Axoni.

Developments in the Permissioned Blockchain

Space

Axoni gave an interesting talk in Prague at DevCon 4 in 2018.

They introduced AxLang as a new programming language for secure and reliable

Ethereum smart contracts. The

speech can still be viewed on Medium. Similar to Hyperledger or Corda,

their approach is to use a permissioned distributed ledger platform based on

open source software in order to help legacy firms use blockchain technology to

operate more efficiently with their customers. Axoni specifically focuses on

derivative markets.

The big advantage is that their infrastructure is built on Ethereum,

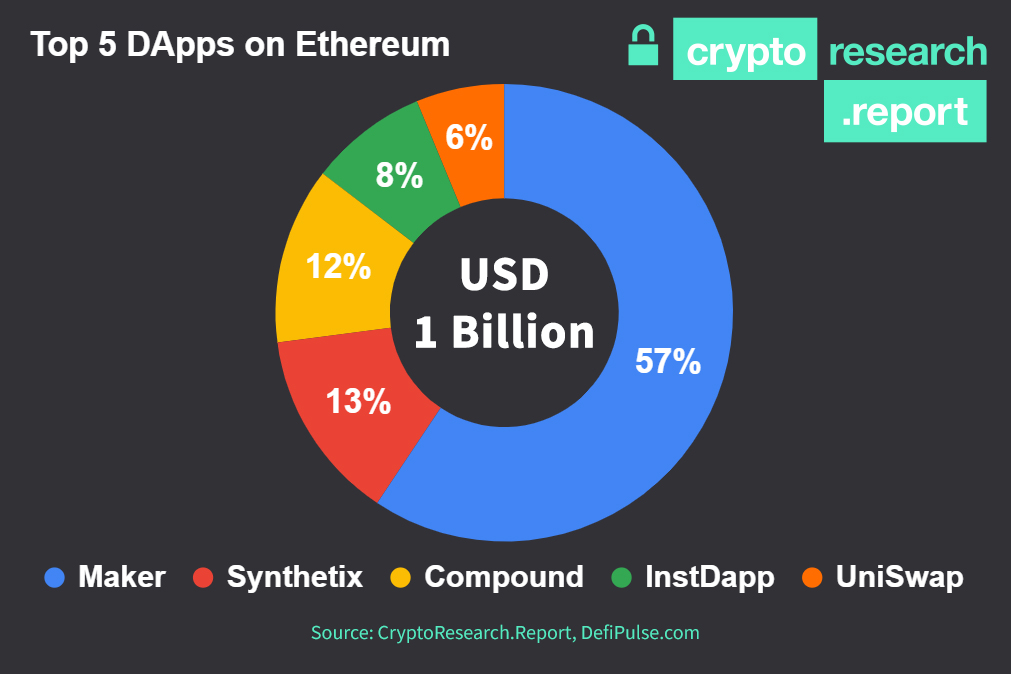

which is still the largest used blockchain for DeFi applications. According to

Defi Pulse, the total value locked in Defi surpassed USD 1 billion on February

9, 2020.

Figure 1: Top 5 DApps on Ethereum

Apart from the Lightning Network, which builds on Bitcoin, all DeFi applications

are based on the Ethereum blockchain. This finding is confirmed by State of the

Crypto Report, which shows the

strong developments and progress around Ethereum and Bitcoin.

Previous market players have struggled to implement Ethereum based

permissioned applications. Bank Vontobel, previously a Premium Partner of

the Crypto Research Report, for example wanted to launch a certificate on

ethereum as well, but there was one main problem. The legal situation and

the lack of a payment token recognized between banks has prevented them from

conducting the complete process exclusively on the blockchain.

Hence the news around the US investment banks Goldman Sachs and Citi

using the Ethereum blockchain is even more positive. Especially with regards to

the status of US crypto regulation, where the SEC is extremely reluctant and

causes many roadblocks.

While there are just a few crypto

advocates in the US, like the so called “crypto mom” Hester Peirce, the EU is

overall much more crypto friendly, especially in Germany. Since the Money

Laundering Act came into force on January 1, 2020, in which BaFin financial

institutions were allowed to conduct crypto asset transactions, more than 40

institutes have shown interest in crypto custody business.

Solaris Bank for example has taken a similar approach

to Fidelity with cryptocurrency custody. The young German bank Solaris AG

founded the subsidiary Solaris Digital Assets GmbH in December 2019 as digital asset

custody service provider. They consider themselves as tech company with a

banking license. Alexis Hamel, Managing Director of Solaris Digital Assets

says:

“We commit ourselves to become the leading infrastructure provider for the European digital asset ecosystem. We trust that by lowering the hurdles for digital asset pioneers, we are contributing to the development of a functional and secure decentralized world, which will transform the way we exchange value around the globe.”

Alexis Hamel

Private blockchains can constitute the perfect testing environment for legacy firms in order to learn about the technology and make their clients familiar with it. However, in order to unlock the full potential of DLT solutions, the ultimate goal should be the use of public blockchains and full business integration of digital assets.

Are digital currencies the wave of the future? Sweden, Switzerland, and Brazil move towards digitalized financial systems, exploring new possibilities of adapting to the ongoing FinTech revolution. E-krona, Swiss franc stable coin, and Pix system are all national responses to the growing cryptocurrencies’ market.

The potential of digital currencies is undeniable: the number of Blockchain wallets has grown over 4 times in the span of the last 3 years, from 10,98 million in late 2016 to 44,69 million by the end of 2019.[1] Powered by people’s enthusiasm, the planet of digital currencies attracts the attention of national banks all around the world. This month, Swedish and Swiss national banks decided to step into the future with the plan to create their own digital currencies, while Brazil came up with its own payment network Pix to lower costs of the national financial system and smoothly transition into the world of Fintech. Governments can no longer ignore the technological revolution, so they join it instead.

Inspired

by Blockchain technology, Sweden has started working on its own version of

digital currency: e-krona. The pilot project is expected to run for a year and

finish by the end of 2021.The Riksbank’s goal is to discover how e-krona could

function in Swedes’ everyday life. Envisioned as a user-friendly, secure

alternative to cash, it is set to work with cards and smartwatches to guarantee

maximum comfort at minimum difficulty. The technical aspects of the project draw

from Distributed Ledger Technology (DLT), used also by Blockchain. The exact

process of creating e-krona is yet to be decided, and there is no fixed date

for its debut. The Riksbankwants to

understand the inner working of e-krona before issuing it, so the one-year

project is mainly the market research. In all certainty, there is a need for a

fintech solution in Sweden, where cash is slowly fading into obscurity,

replaced by smartphone applications.

Sweden is not the only country, which announced the creation of

its own digital financial system this week. Brazil, where 18% of surveyed

people have already had experience with cryptocurrencies[2], is an immense market for

fintech innovation. The central bank of Brazil decided, however, to take

matters into its own hands and test a brand-new payment network – Pix. To offer

the optimal coverage and easily blend into the Brazilian financial landscape,

the system will be used by all major financial institutions, including the

country’s biggest banks, effectively becoming integrated into 90% of all active

bnks accounts in the country.

Pix is set to operate through an application, which allows for

instant money transfer and QR code scanning. The tests have just officially

begun, but in nine months’ time – November 2020 – Pix may be open to the public

for the first time if things go right. The officials’ plans are definitely

ambitious: the mass adoption of the system is scheduled for 2021. In fact, the

president of the Brazil’s central bank, Campos Neto, acknowledged the need for

the new payment methods in the digital age, saying that “the world demands a payment

instrument that is cheap, fast, transparent and secure” and he called Pix one

of the most important projects of the year, stating that it would be the Brazilian

answer to bitcoin and cryptocurrencies. Designed to enable a wide range of

transactions, including paying government fees, and mandatory for the country’s

major financial players, Pix might be Brazil’s digital future in the making.

In

the midst of the fintech revolution, Switzerland doesn’t remain a passive

bystander. Swiss Central Bank announced plans for its pure digital currency to

dive into the digital future on its own terms. While the project’s exact

details and likely launch is unclear, Swiss transition into to the digitalised

banking continues in 2020, with the launch of Swiss Digital Exchange (SDX)

planned for the end of the year.

As the increasing number of

governments acknowledge the need for new banking systems, the future of digital

currencies looks bright. With Brazil’s ambitious plans to accelerate its own

fintech transformation, Sweden’s hopes to offer its citizens the institutional

replacement of obsolete cash, and Switzerland’s slow but inevitable financial

adaptation, the world is ready to move into the post-cash era and redefine the

way we view money.

The price of Bitcoin, by far the biggest player among all cryptocurrencies, fell more than 10% within the last few days. Other major cryptocurrencies, such as Ethereum, Litecoin and Bitcoin cash, have also decreased in value, but Bitcoin’s decline generates the most headlines, as earlier this year, it noted the record $10,000 per bitcoin and was showing no signs of slowing down. In the course of the last few days, Bitcoin lost $30 billion in value, going down 0,22% within the last 24 hours. Created by unknown individual(s), Bitcoin was designed to enable fast, cheap transactions without using traditional banking, and when its price went up at the beginning of the year, many started to regard it as a ‘safe-haven asset’ and the answer for the global trade crisis connected to coronavirus. China’s participation in the cryptocurrencies’ market is enormous, so given the latest course of events regarding the virus, the cryptocurrencies’ decline seems natural for some, while other industry experts, such as Vitalik Buterin call it “rationalised bullshit”.

Despite Bitcoin’s drop in value, many remain positive about its future, as it is driven by demand, rather than GDP. The entire business model of Bitcoin is based on scarcity, much like the former monetary programs, which only allowed printing the amount of money corresponding to the actual amount of gold. To ensure such scarcity, Bitcoin invented the process of halving, or simply reducing the total supply over time to boost the value of the cryptocurrency. Typically, Halving takes place every four years and the next one is set to take place in May 2020. Experts predicted that the price of Bitcoin would increase several times and reach up to $70,000 per bitcoin. Whether it is wishful thinking or an accurate prediction, only time will tell.

Nevertheless, it is without a doubt that Bitcoin continues to develop and improve its services, particularly in terms of privacy and scalability. In the first half of 2020, we can expect the launch of a consumer application for Bitcoin and cryptocurrency purchases. The app will be supported by Starbucks, Microsoft, and Boston Consulting Group. Despite a sudden decline in value, Bitcoin’s market capitalization equivalent is substantial. According to Statista’s database [1], between the first and last quarter of 2019, it increased by over 57%, from 72,37 billion dollars in the 1st quarter to 169,44 billion dollars in the 4th quarter. Square, one of the companies, which included Bitcoin in their payment methods, observed a 60% rise in the number of active users in the last quarter of 2019. The company’s revenue increased by 41% within a year, reaching over $1,3 billion dollars. Why is their success attributed to the Bitcoin adaptation? Half of $361 millions produced by Square’s Cash app were generated by Bitcoin transactions – in just 3 months. Numbers seem to be in favour of cryptocurrencies, even when investors are not. During the meeting with crypto representatives, the famous investor Warren Buffet was reported to have donated all cryptocurrencies he was given to the charity, stating that “I don’t own any cryptocurrency. I never will.” Regardless of the current crypto landscape, Bitcoin’s kingdom is yet to fall, but will it quickly recover? Remains to be seen.

Change is the only constant in the world of cryptocurrencies. Although Bitcoin lost $30 billion in value within just a few days, it continues to attract customers across numerous applications, having generated half of Cash app’s revenue in just 3 months. Powered by demand, it may rise again, once scarcity’s in play.

Several blockchain-based companies are publicly listed on stock exchanges throughout the world. Some of them are trading at an unwarranted price given their revenues and earnings potential. Some have even already gone bust like Riot Blockchain Inc. (RIOT) that dropped 97% from an all time high of $46 in 2017 down to the current price of $1.33, or they have switched business models like Fortress Blockchain Corp. now called Fortress Technologies Inc. (FORT) after quarters of consecutive million dollar losses.

This article is a sneak peek of the Crypto Research Newsletter published every week to our subscribers. We do not often publish these posts publicly, so if you would like to receive professional financial analysis of crypto assets weekly subscribe here: https://cryptoresearchnewsletter.substack.com/

In this week’s edition of the Crypto Research Newsletter, we discuss how to value publicly listed blockchain stocks, and how some investors with deep pockets are turning overvaluation into an opportunity.

There are several ways to value a publicly listed stock. This week, we wanted to evaluate if Michael Novogratz’s Galaxy Digital Holdings Ltd. traded on the Toronto Stock Exchange with ticker GLXY was a good buy or not. Galaxy Digital does venture capital, they sell investment products, they do lending, and they do market making, amongst other activities.

The market capitalization of Galaxy Digital is $88.56 million Canadian Dollars (CAD). The stock price is $1.32 CAD. Is this a good buy at $1.32 or not? There are many ways to answer this question, but a simple way is just to compare Galaxy Digital’s price to comparable firms.

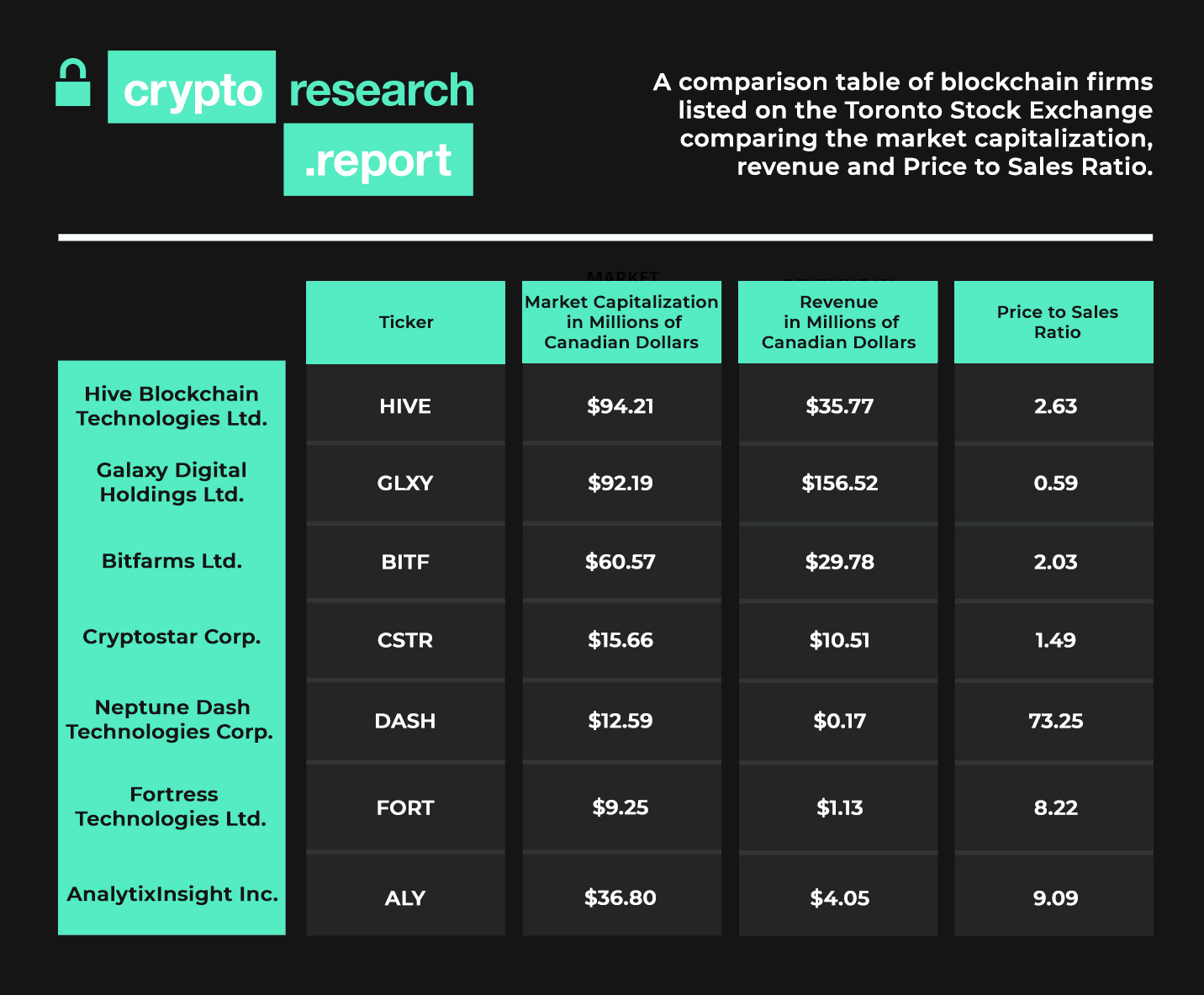

Comparable blockchain firms that are listed on the Toronto Stock Exchange include Hive Blockchain Technologies Ltd., Bitfarms Ltd., Cryptostar Corp., Neptune Dash Technologies Corp., Fortress Technologies Ltd., and AnalytixInsight Inc. The market capitalization, revenue and Price to Sales Ratio (P/S) are listed in the table below.

Table 1: Price to Sales Ratio of Publicly Listed Blockchain Companies

Just a quick glance at the table shows that Galaxy Digital is relatively low priced compared to other blockchain firms. Galaxy Digital’s Revenue in 2019 was $156 million, higher than the company’s $92 million CAD market capitalization. This gives Galaxy Digital a P/S Ratio of 0.59 compared to the group average of 13.9. Galaxy Digital’s stock has increased 26% since the beginning of this year from $1.05 to $1.33. However, the company is still not turning a profit after costs.

A quick glance at Table 1 also shows a humungous outlier. Namely, Neptune Dash Technologies Corporation. Neptune Dash is a company that hosts masternodes on the Dash network. They currently have 16 masternodes, or approximately 16,100 Dash worth around $1.7 million USD and they have invested in Cosmos (ATOM). Even though everyone says that Tesla is overpriced, Tesla (TSLA) is still only trading at a P/S Ratio of 6.5x their annual revenues. Apple (AAPL) trades at 5.5x their annual revenue.

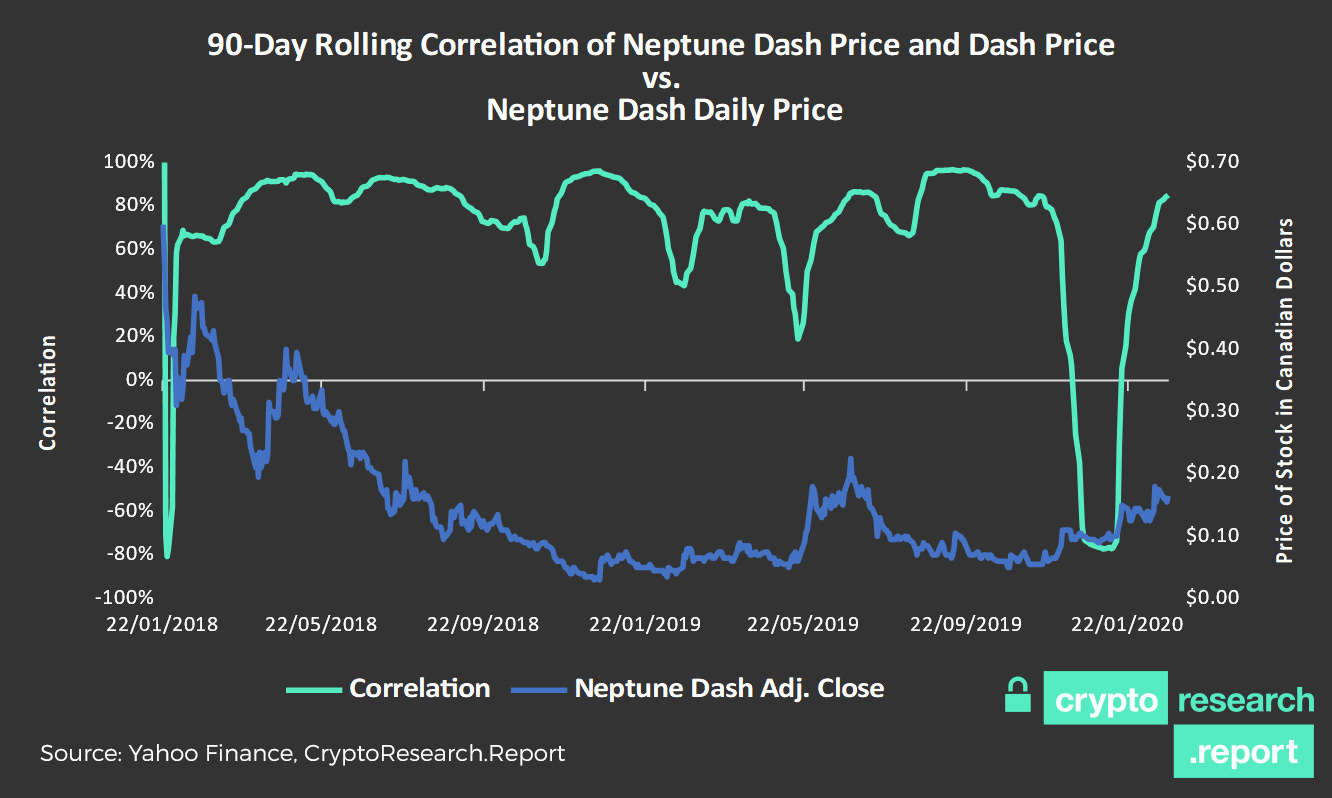

Figure 1: Neptune Dash Stock and Dash are Highly Correlated

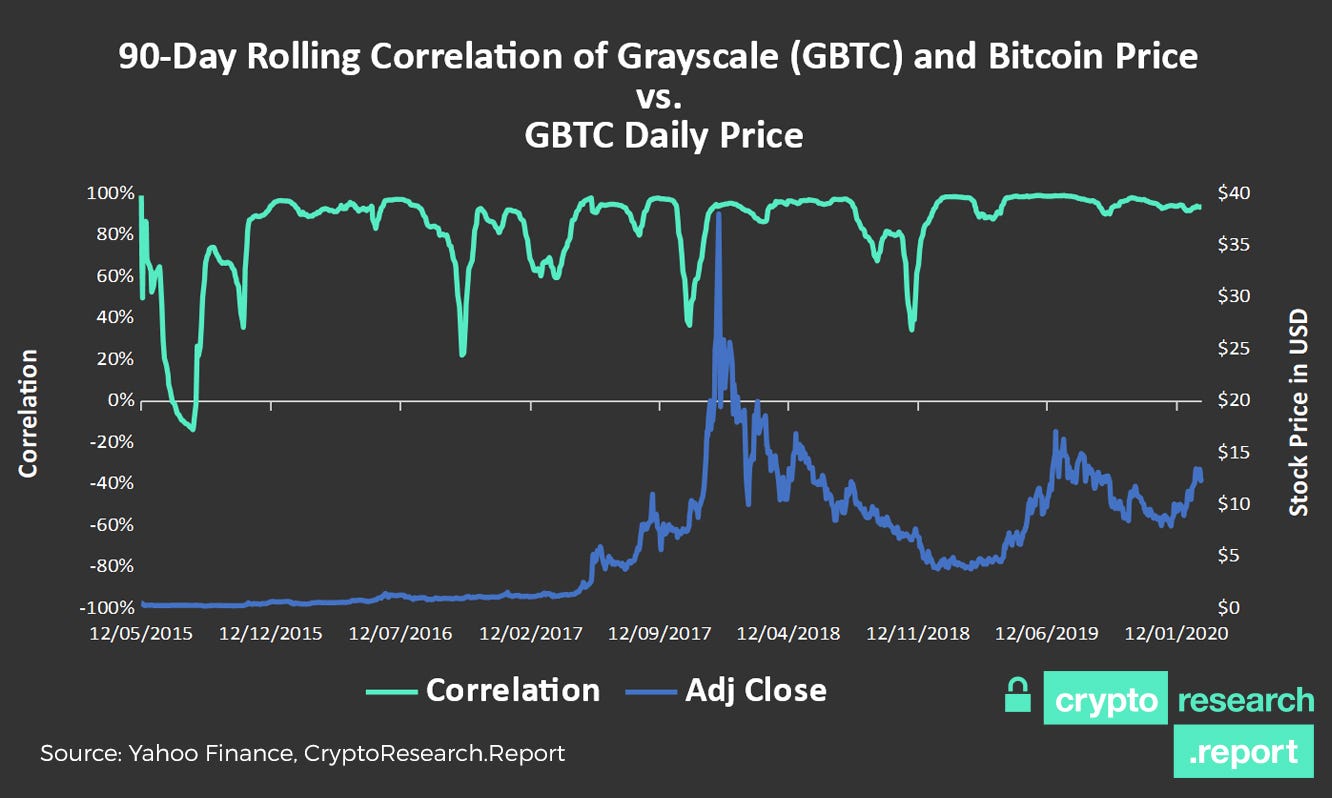

Figure 2: Grayscale GBTC Stock and Bitcoin Are Even More Correlated!

So how can a 73x P/S Ratio be warranted? One interpretation is that 73x could be a very early stage startup multiple meaning that investors expect for Neptune Dash to earn a lot more in the future than they are currently earning.

Another interpretation is that institutional investors cannot easily hold privacy coins directly in their portfolio, and are therefore, willing to pay more for a publicly listed stock that gives them access to privacy coins. There is some evidence of this with stocks like Grayscale’s GBTC Bitcoin tracker that has more often than not traded at a 20%-30% premium over the spot price of Bitcoin during the past few years.

Grayscale has 303,363,800 outstanding each worth $11.72 USD, and each share is backed by 0.00096645 Bitcoin, worth approximately $9.33 USD. This means that GBTC shares are trading at approximately 25.6% premium over the spot price of Bitcoin. An obvious trading strategy would be shorting GBTC and holding Bitcoin long, but this has not worked well in the past for traders, because GBTC’s premium has persisted month after month. Grayscale has approximately 293,185 Bitcoin under management and charges a 2% annual fee on a passive investment strategy, which at first glance, seems high, but is actually quite reasonable given the fact that cryptocurrency custody is not that straightforward.

When comparing the Neptune Dash stock price to the Dash price, an average 90-day rolling correlation of 70% is found over the past two years since Neptune Dash was listed on the Toronto Stock Exchange. The only time that these two assets had a negative correlation was during December 2019 and early January 2020, when the price of Dash was going down and the price of Neptune Dash stock was going up. This can most likely be explained by the fact that the drop in Dash’s price triggered a massive selloff of Dash masternodes, which meant that the existing masternodes earned more. Since Neptune Dash runs masternodes, this means that their earnings went up on each node.

In contrast, the GBTC average 90-day rolling correlation with Bitcoin is much higher, at 83% over the past five years and 92% over the same time span that the Neptune Dash and Dash correlation was calculated over.

One final note on this peer group of blockchain firms: there is an unfortunate back story to Fortress Technologies Ltd. The company was listed on the stock market in 2018, and is currently trading at $0.12 CAD. This is the epitome of a crypto penny stock. The company has basically no information on their website and the last post that Fortress Technologies Ltd. made on their Twitter account was in 2018 shortly after being publicly listed. We were surprised to find that Roy Sebag and Josh Crumb from Goldmoney are part of the Fortress team. Apparently, their attempts at Bitcoin mining did not pan out as expected, as they officially removed “blockchain” from their name in April of 2019 after consecutive quarters of layoffs and losses.

In conclusion, Grayscale and Neptune Dash seem grossly overvalued when comparing their share price, number of shares outstanding, and earnings. This is most likely a symptom of all stock prices being grossly overvalued because the Fed’s faucet of money is flooding the market and investors are betting on scarce crypto assets as being a hedge against fiat inflation. This will not last forever, but as Keynes said, “markets can remain irrational a lot longer than you and I can remain solvent.”

This Week’s Top Cryptocurrency News

Wyoming’s Blockchain lady, Caitlin Long, is starting the first Bitcoin Bank called Avanti. We are personally excited at the CryptoResearch.Report, because Caitlin is one of the few people in the Blockchain space that combines competency, hard-work, and honesty – all qualities needed for a company to have long-term success in the crypto world! Read more.

Tomorrow, Wednesday the 26th of February, the U.S. Securities Exchange Commission will decide if the Wilshire Phoenix exchange traded fund (ETF) on Bitcoin will be approved or not. If approved, the ETF will have fees of 68 basis points (0.68%) per annum and a maximum share price of $2,500 USD. Read more.

No Central Bank Digital Currencies (CBDCs) have been officially launched so far, but Sweden will probably win the race with their e-krona. Read more.

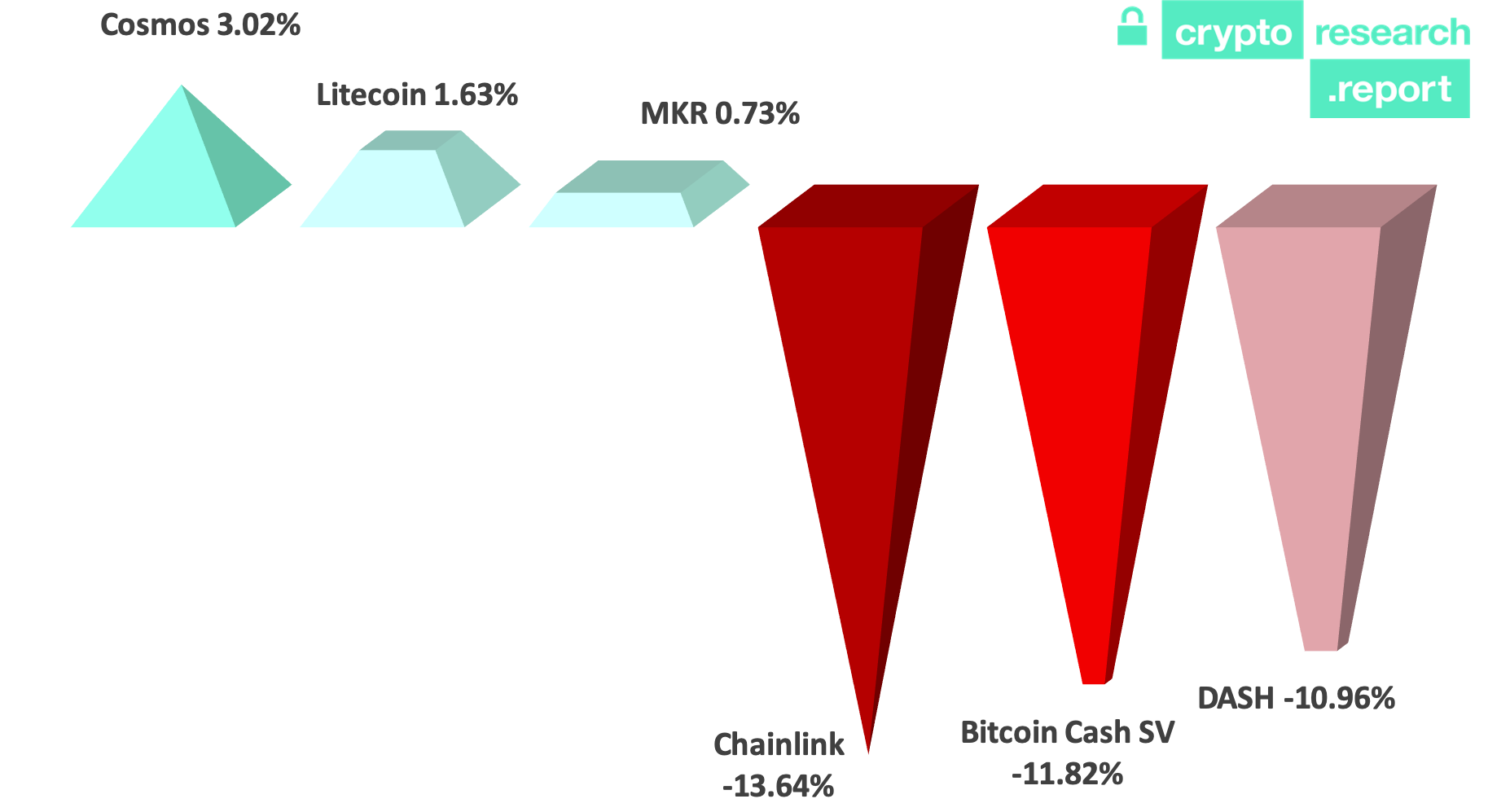

Winners and Losers

Everything that goes up must come down, and this week was not very kind to Chainlink or the crypto asset market in general. Chainlink is down – 13.64% this week, but is still up 116% year to date with a current price of $3.91 compared to $1.81 on January 1, 2020.

The past week’s largest cryptocurrency winners from the top 50 market capitalization are Cosmos (3.02%), Litecoin (1.63%), and MKR (0.73%).

The biggest losers were Chainlink (-13.64%), Bitcoin Cash SV (-11.82%) and Dash (-10.96%).

Figure 3: Largest 7-Day Returns for Top 50 Market Capitalization Coins

Bitcoin has had a second week of losses, and is down 1.21%. Due to the wide diversification of the assets held in the Crypto Research Portfolio, the weekly return for the portfolio was positive. This is mainly do to our gold coin Pax Gold shooting up 8.2% in value after the stock market sell-off. As of February 25th, 2020, the portfolio’s value increased by 205 basis points or 2.05% in the last six days since the last edition of the newsletter was published on February 19th, 2020. Gold is an interesting asset given the economic uncertainty surrounding the Corona Virus.

Leading digital money platform Uphold today introduces zero-commission trading on cryptocurrencies in a milestone for the industry designed to open up affordable access to one of the world’s most important new asset classes for millions of retail investors.

“In practical terms, there’s now no easier or more cost-effective way for retail investors to trade cryptocurrencies and other assets”

Initially available only on iOS and Android mobile apps, the move represents a seismic shift in a sector that until now has largely resisted the commission-free model revolutionizing stock and ETF trading. Before today’s announcement, cryptocurrencies were one of the more expensive asset classes for retail investors to trade, with fees north of 200bps on some mainstream platforms.

‘Our goal is to create the easiest and most cost-effective place for retail investors to buy and sell cryptocurrencies and other assets,’ explained J.P. Thieriot, C.E.O. of Uphold. ‘And unlike our competitors, we’re staying true to the fundamental premise of cryptocurrencies: financial self-sovereignty.’

‘At Uphold, you can move your crypto into private wallets at will; send funds to virtually anyone, anywhere, instantly and free of charge; as well as use your holdings as a medium of exchange for payments. None of which you can do at Robinhood or Revolut.’

As an established platform listing 50+ currencies and providing account funding via seven cryptocurrency networks, debit/credit cards and bank connections in more than 40 countries – with the UK, Canada, Poland, Romania, Croatia, and Hungary added earlier this month – Uphold is the first major U.S. cryptocurrency venue to offer commission-free trading.

Simultaneously, Uphold is launching the world’s easiest trading interface, consisting of just two fields: ‘From’ and ‘To’. The ‘Anything to Anything’ screen means that a novice user can fund their account, send money to other people, or trade from any asset into any other asset directly, in two taps – on one screen.

The new interface surfaces Uphold’s unique advantage over its rivals: customers can trade directly between any supported asset, free from the limitations of Currency Pairs that still constrain choice and create unnecessary cost and complexity at many trading venues.

Whereas on most exchanges a conversion such as Mexican Pesos to XRP would require two trades and incur two sets of fees – Mexican Pesos to USD and USD to XRP – on Uphold, the process is one seamless, commission-free transaction.

“In practical terms, there’s now no easier or more cost-effective way for retail investors to trade cryptocurrencies and other assets,” said Thieriot. “No other platform gives customers such choice, freedom, and value for money.”

Uphold is also adding new funding and withdrawal options to the platform, which is now attracting up to 7,000 new accounts every day. For the first time, customers can fund their accounts with zero fees via credit* (and debit) cards – a new standard for the industry. Instant withdrawal to debit cards will be available in the coming weeks.

“The convenience of being able to withdraw your funds immediately to a bank-issued debit card is going to be a huge attraction for customers,” said Thieriot. “And in many parts of the world, it will be a first for a cryptocurrency platform.

“These are the biggest changes we’ve made since we started in 2014. Together, they make Uphold the easiest and most cost-effective place for retail investors to buy and sell cryptocurrencies, and break down the barriers that prevent people from investing and enjoying world-class financial choice.”

The web version of New Uphold is expected to launch later this month. iOS and Android Mobile Apps available to download now.

* For deposits into cryptocurrencies.

About Uphold

Uphold is a leading digital money platform with more than 1.7 million customers globally and almost $6 billion in transactions to date. It serves both retail investors and businesses. Leveraging blockchain technology, Uphold provides its customers with easy access to cryptocurrencies, national currencies, precious metals, yield/credit products, and soon crypto-backed debit cards. Customers can trade with zero commissions. Or send funds to virtually anyone, worldwide, free of charge, including payments to businesses and employees. Uphold is unique in translating all supported asset classes into a common digital language, which means that any asset can be exchanged directly into any other asset, creating an easy and intuitive trading experience. This Anything to Anything architecture cuts out unnecessary fees and complexity compared with other platforms relying on currency pairs, which would require an intermediate trade to exchange Mexican Pesos into XRP, for example. Businesses use Uphold to pay people around the world, or to accept customer payments in cryptocurrencies and convert them automatically into national currencies. Accounts can be funded via seven cryptocurrency networks, bank connections in around 40 countries, as well as debit and credit cards. The platform offers 27 national currencies, 30 digital currencies, and four precious metals. Uphold is available through web, iOS and Android applications.

Alternative Airlines, a UK-based global flight search and booking platform, in October last year partnered with Utrust, a payment method offering cryptocurrency payments of your choice. With this partnership, Alternative Airlines customers can pay for flights to destinations around the globe using a range of cryptocurrencies including Bitcoin (BTC), Ethereum (ETH), DASH, DigiByte (DGB).

Alternative Airlines currently works with over 600 global airlines to provide customers with a greater choice of flights and payment methods. Partnering with Utrust means customers can pay for competitively priced flights rates through all the major airlines, including American Airlines, Delta Air Lines, United Airlines, British Airways, Virgin Atlantic, and China Southern Airlines. Specializing in off-the-beaten-track destinations, Alternative Airlines also works with national and regional carriers such as Air Chathams in New Zealand.

With the help of Utrust, Alternative Airlines’ customers can use an extremely safe way to pay. Utrust is providing customers with the increased security and convenience of cryptocurrency payments by offering buyer protection on all purchases and crypto-to-cash settlements.

Sam Argyle, Managing Director of Alternative Airlines, said, “At Alternative Airlines, we are committed to offering a seamless transaction process, while allowing our customers to choose how they want to pay. Alternativeairlines.com is a single platform for travellers to easily search and book flights on over 600 airlines. We believe crypto to be the money of tomorrow, playing an important role in the future of commerce. Therefore, we are incredibly excited, as our partnership with Utrust is the next major step in continuing to tailor the online booking experience to the customer, who now have the opportunity to pay with cryptocurrency on all of the airlines that we ticket.”

Alternative Airlines, an IATA-accredited agency, was featured in the 2019 Sunday Times Fast Track Tech 100, which highlights the top 100 fastest growing technology companies and awarded Best Selling Travel Agent in 2017. Customers can also choose from over 25 international payment methods — including all major debit cards and payment plans from all the best-known global providers — as well as over 160 localized currencies.

Alternative Airlines is a flight-search and booking website that offers a fast, easy and convenient way to book flights to remote destinations, as well as well-known locations. Alternative Airlines specializes in providing travellers with a wider choice of flights by working with more than 650 airlines including the smaller, regional ones across the world, especially in Latin America, the Caribbean, Africa and South-East Asia. Alternative Airlines’ global audience can enjoy over 25 international payment methods across 160 currencies.

About Utrust

Utrust is the leading cryptocurrency payment solution designed to modernize the finance and payments industry and solve the problems of traditional payment methods by offering instant transactions, buyer protection, and immediate crypto-to-cash settlements for the merchant. The Swiss-based startup was granted SRO approval to operate as a ‘financial intermediary’ under VQF, the self-regulatory organization approved by Switzerland’s independent financial-markets regulator, FINMA. The Utrust platform went live in 2019 when football club S.L. Benfica came on board as the first merchant and the first major European football club to accept cryptocurrency. Utrust has since added Phone House Portugal to its growing list of merchants.

Facebook’s Libra coin is meeting strong resistance from governments and central banks. But there is also a lot happening in the “traditional” crypto sector. Several players are laying foundations for a regulated market that could attract institutional investors. And Bitcoin reacted to the recent rounds of easing by central banks.

The year 2019 is slowly coming to an end. What was the best place for an investor’s money this year? Prices for Bitcoin have more than doubled since January – even though they have recently fallen sharply again. From April 1 to June 24, they rose by 250 percent – from just under $4,000 to just under $14,000. At the time this report was prepared, Bitcoin was priced at around $9,000.[1]

Figure 1:Almost 1 Million Active BTC Addresses Per Day

Source: Coinmetrics.io, Incrementum AG

“Facebook’s digital currency, Libra, is a mixed blessing for Bitcoin and other digital currencies.” Forbes

Forbes

Whichever way you look at it, Bitcoin beats the second-best asset of the year, namely US technology stocks, by far. This year, they have risen by about 30 percent. Even gold, which is experiencing a quite respectable year, is just up 17 percent. The broad S&P 500 index gained 21 percent. All this fades in comparison to Bitcoin’s growth by more than 140 percent – from $3,300 in January to about $8,200 per coin in October.

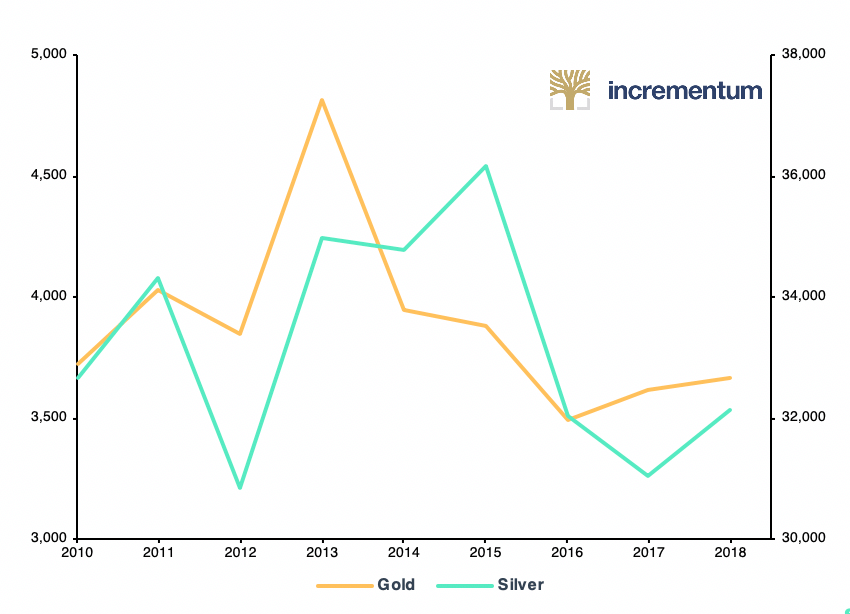

Figure 2: Non-Monetary Demand For Gold and Silver Declining (in Tonnes, 2010 – 2019)

Source: The Silver Institute, Refinitiv GFMS, Metals Focus, World Gold Council, Incrementum AG

Still the crypto space has been rather quiet lately. The rise in prices alone was not enough to satisfy the mainstream media hunger for new stories. In addition, Altcoins look rather bad at the moment. Take Ethereum, for instance. The second most important cryptocurrency rose by “only” 80 percent between January (around $100) and October (around $180). The focus of politicians and the media has for some months now not been Bitcoin or Ethereum but the Libra project initiated by Facebook.[2]

One almost has the impression that Libra has displaced Bitcoin from the podium of the most important crypto projects. Especially in the mainstream media, where many journalists have specialized in crypto. And they don’t seem to get enough of the drama around Libra. But: Libra does not yet exist. Worse still, the alliance around the project is already beginning to crumble. [3]

According to Szabo, Bitcoin is more secure that Ethereum.

The currency coins that Nick Szabo is interested in are Mimblewimble-based coins and some of the of the privacy coins including Monero, ZCash, and Dash.

Demelza Hays. Do you think Bitcoin is Turing-complete? What can Ethereum do that Bitcoin can’t? Nick Szabo: No, the Bitcoin main chain is not Turing complete. It does have a Turing-complete sidechain called RSK. Ethereum’s programming language can do open-ended loops for example (up to gas limits) and Bitcoin main chain (layer 1) can’t. Programming Ethereum or RSK gives you the full expressive power of programming whereas programming on the Bitcoin main chain does not. This makes Bitcoin safer and is more appropriate where the main functionalities are store of value and medium of wealth transfer but makes Ethereum and RSK better for smart contracts.

Nick Szabo speaking with Richard Olsen at Money Museum in Zurich, 2016. Source: Google Images.

Demelza Hays: Do you think Bitcoin is digital cash or digital gold? In ten years from now do you think that we will be paying for our coffees with Bitcoin or some derivative of Bitcoin? I think Bitcoin and gold are too inelastic to be used as a unit of account. As the coinbase reward tapers, do you think the Bitcoin main chain will have many transactions with a small fee or do you think there will be few transactions with large fees?

In my opinion, setting an artificial data size limit for each block is similar to the government setting a price ceiling or floor on a good or service. I would allow the block size to be determined each block by the miners. This would be more similar to the free market. If the miners make the size too small in an attempt to earn more from fees, then users will switch to other blockchains that are a substitute service. If the miners make the size too large and certain miners gain an advantage because they can propagate blocks faster then users will switch to a substitute service.

Nick Szabo: Layer 1 is digital gold and Layer 2 is digital cash (among other things it can be — RSK is an example of Layer 2 for smart contracts).

Demelza Hays: Over the past decade, the correlation between Bitcoin and gold has been between positive 0.2 and negative 0.2 and has a slightly positive uptrend at the moment. Since some of gold’s demand comes from non-monetary purposes such as jewelry and industry, we argue that gold will always be less volatile than Bitcoin in terms of purchasing power of real goods and services over time. We have an investment strategy which intends to arbitrage between Bitcoin and gold. As Bitcoin becomes relatively expensive to gold, we sell Bitcoin and buy gold, and vice versa. Do you think the correlation in returns between gold and Bitcoin will go up in the future?

Nick Szabo: Very probably yes.

Demelza Hays: Are there any blockchain projects that piqued your interest recently?

Nick Szabo: The various Mimblewimble-based coins, some of the other privacycoins (Monero, ZCash, Dash), RSK (an Ethereum-like sidechain for Bitcoin).

Demelza Hays: Where do you see the US in ten years from now? Do you see Libra and Bitcoin competing or do you see a David Crowley-style Gray State? Nick Szabo: I suspect Libra will get buried under a political blizzard and doesn’t stand much of a chance. It would compete far more with payment systems like PayPal, and is more akin to things like Tether, than it would compete with or is akin to Bitcoin.

“With a commitment in a structured product,

specifically a tracker certificate, one does not invest directly in the

cryptocurrency but follows the price movements like a shadow. Investment risk

depends on price losses and creditworthiness of the issuer (default risk).

However, the investor must remain vigilant. Just because he has purchased a tracker

certificate from a bank, it doesn’t mean that it’s iron-clad. Should the price

of his cryptocurrency crash or even disappear from the market, there is, of

course, a total default risk here as well.”

Jürgen Kob and Paweł

Sobotkowski

We want to sincerely thank Lucas Ereth and GenTwo Digital for contributing this chapter. Lucas is a managing member of GenTwo Digital (https://www.g2d.io). Our readers can sign up for a free newsletter at https://www.g2d.io/blog. Please note, that GenTwo is a premium partner of the Crypto Research Report.

Lucas Ereth

This chapter features a sneak peek into

the life of the Managing Partner of GENTWO Digital and Forbes DACH 30 Under 30,

Lucas A. Ereth.

What does your business do?

To put it simply, we’re securitization experts working to bridge

the gap between traditional finance and the emerging crypto market. While our

parent company GENTWO creates securities for all asset classes, GENTWO Digital

specializes in the securitization of digital assets. In other words, we convert

digital assets, like cryptocurrencies, into structured products. These products

are then outfitted with an International Securities Identification Number (or

ISIN, for short) ‒ the de facto standard for securities trading internationally ‒ which ensures that the product is “infrastructure

compatible” with every bank and large scale/institutional investor.

In doing so, we turn a digital asset into something that is

bankable and manageable within traditional investment portfolios inside the

global banking system. Why would we do that? Well, large private and

institutional investors were having quite a bit of trouble accessing the market

for digital assets due to different aspects of the traditional functional

framework. So, we set out to provide a service that would make crypto assets

accessible for qualified investors from around the world via GENTWO and GENTWO

Digital.

How are tokens different from

structured products?

Structured products are flexible investment instruments that offer

an attractive alternative to direct financial investments (such as stocks,

bonds, currencies, etc.). Thanks to their flexibility, structured products

allow for the creation of investment solutions that are suitable for different

risk profiles and market expectations, even in demanding market environments.

New, next-generation structured products can now be utilized to give access to

a myriad of digital assets.

Tokens, on the other hand, are digital assets themselves, and are

not necessarily considered financial instruments. Both structured products and

tokens can be used for similar purposes, but the two are not the same thing.

Tokens also live on the blockchain, while structured products are financial

products that live in the banking system, and asset managers, banks, and

professional investors use them in their daily lives to get access to assets

and markets.

What are advantages of securitization vs.

tokenization?

I think that within today’s investment

landscape, one could make use of both, as they are each tailored to different

purposes and clientele.

A token offering, for instance, is limited to investors that can

handle the complexity of crypto wallets. At this stage, most crypto wallets are

best suited for retail investors that usually invest in small ticket sizes.

With the help of securitization services (this is where we come into the

picture), you can now take a crypto portfolio or a portion of any token and

convert it into a traditional financial structured product. This “real”

security is now suddenly made available to banks, family offices, pension

funds, high-net-worth individuals etc. So, big investors who generally do not

make use of digital wallets are, thus, granted the opportunity to actively

participate within the crypto market.

What makes securitization attractive to

traditional market participants?

Institutional investors can invest in new assets with their proven

and compatible form of investment. Structured products are investment

instruments that are very familiar to traditional market participants. So,

institutional investors can finance a crypto venture, and serve as a strong,

key member of the project supporters’ community, all while using the same daily

financial instruments that they are already used to. This is a wonderful

example of how structured products and tokens complement each other. At GENTWO,

we firmly believe that this setup will not only grant access to but actively

attract investors of the highest caliber. We’re essentially allowing the

investor to choose which format he or she prefers: a fully digital asset that

lives on the blockchain and in a digital wallet or a traditional investment

certificate (structured product) that lives in your bank account and represents

a digital asset. Securities are issued through a tailor-made and segregated

issuance vehicle that is unique and stays off of a client’s balance sheet. With

this design, the so-called issuer risk is (by default) eliminated.

As someone who works with many

structured products on a daily basis, what would you personally invest in?

I personally currently hold 27

different coins and tokens in my crypto portfolio. If I were to create my own

structured product, I would most probably turn my portfolio into a so-called

Actively Managed Certificate (a structured product with an actively managed

strategy behind it) and make it available for qualified investors. This is

actually one of our most common use cases at GENTWO Digital – traditional or

crypto asset managers who utilize us to turn their strategy into an investable

asset. Our platform provides the tools to facilitate the process from start to

finish, from converting the AMC into a Swiss-compliant security to getting a

Swiss ISIN. All within 5 to 15 business days.

Just to be clear, this is my personal view; cryptocurrencies are

highly volatile, and it’s important to remember that while there are attractive

return opportunities, you have to be willing to expose yourself to high risk

and the chance of losing your principal if you choose to embrace crypto

investments.

What is the biggest opportunity for

entrepreneurs who want to make a successful business in the crypto space?

Today’s digital world is quite

literally at our fingertips. I would encourage entrepreneurs to try to look

into the future and play around with connecting the dots between what is

present and what is possible. Making use of and/or sometimes just breaking up

and reshuffling certain dots can make all the difference.

I also think that making crypto-based

services or applications so accessible that an individual user does not even

realize that he or she is interacting with a blockchain-powered product or

service still remains the biggest challenge for mass adoption, and therein lies

the biggest potential for entrepreneurs within the crypto space.

What should entrepreneurs be aware of?

As always, everything starts with a

good business case, a business plan, and a good execution strategy ‒ I’d say that applies regardless of

whether or not you throw blockchain into the mix. Once you’ve laid that

foundation, you now need to evaluate how to use and leverage blockchain

technology for your specific case. Also, and I can’t stress this enough, ask

yourself if it even makes sense, because in most cases blockchain alone

probably won’t be the sole, magic ingredient that will ensure your business’

success.

What is the biggest threat to the crypto space?

I would say a lack of

understanding and public disinterest. If people fail to recognize or

acknowledge the benefits, value and possibilities of cryptocurrencies, Bitcoin

and the like will eventually die out as the hype and fanfare of even the

starkest supporters begins to wane.

Where do you expect the sector to be at the end of 2020?

It looks as though 2020 is set to be

the year where blockchain technology may (for the first time) reach billions of

people at once, as big tech firms like Facebook become active participants

within the space. I think this will mark the real start of the Internet 2.0,

with the potential to usher in an era of trust and digitized value.

Decentralized services will definitely help shape the future development of

this planet.

“The only reason that cryptocurrencies exist is because of regulations that stop us from using gold as money.”

Peter Schiff

Key Takeaways

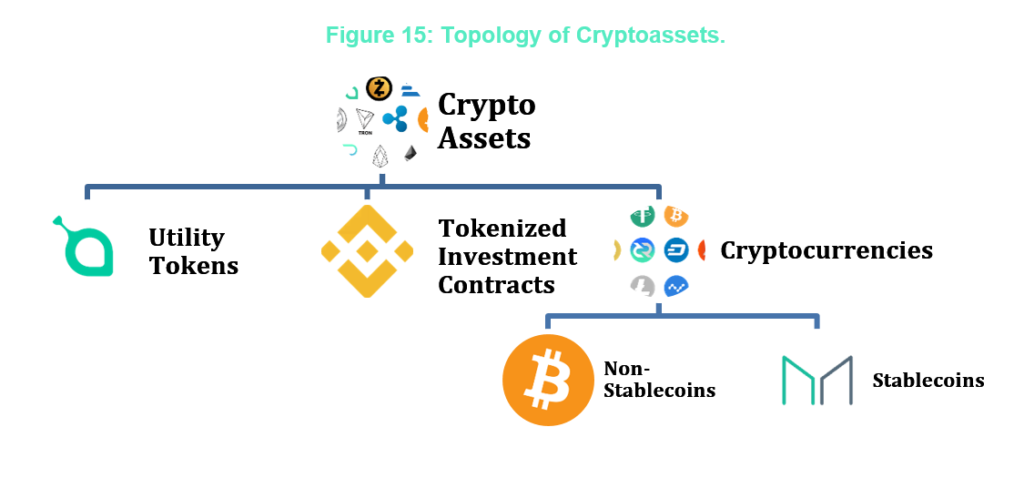

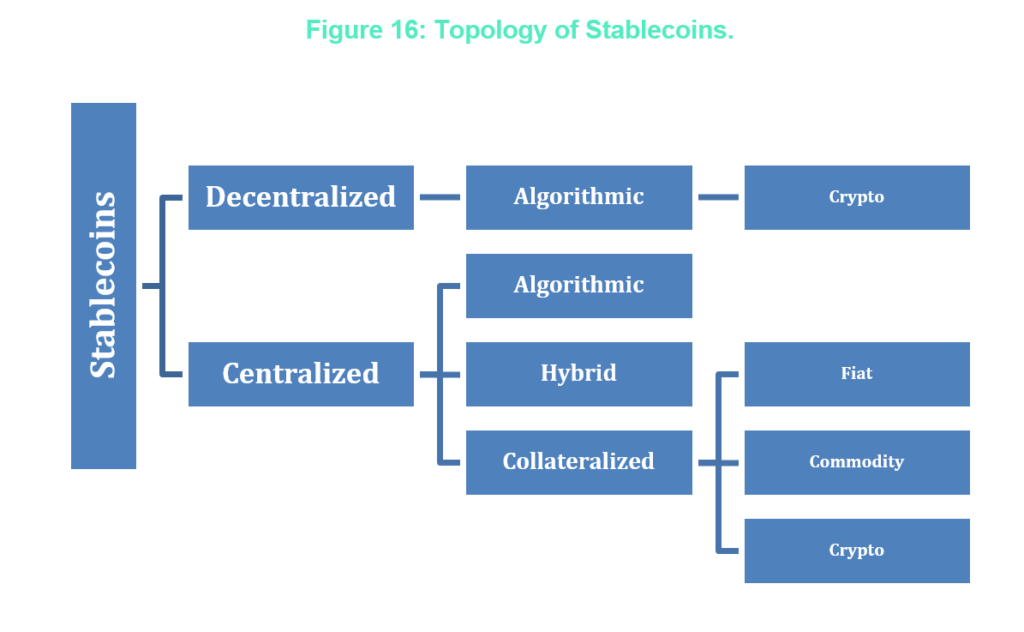

Similar to gold-ETFs, all of the gold-backed cryptocurrencies on the market are centralized. This means they have counterparty risk. Unlike storing your own physical gold, gold-backed cryptocurrencies require you to trust a company for storage.

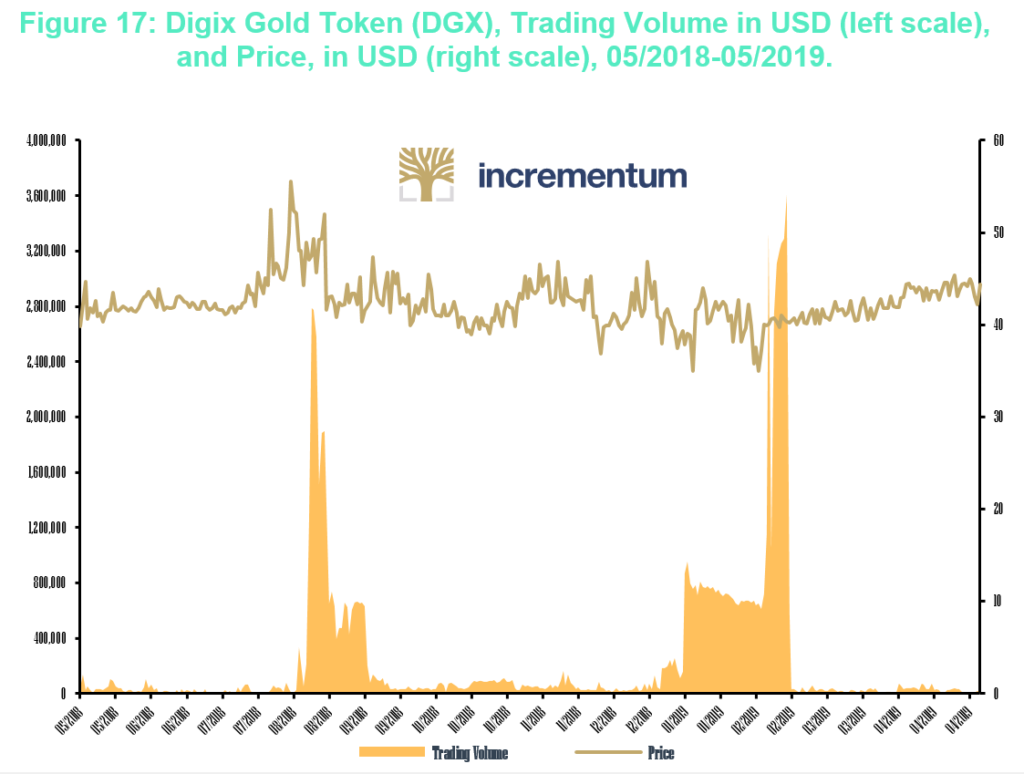

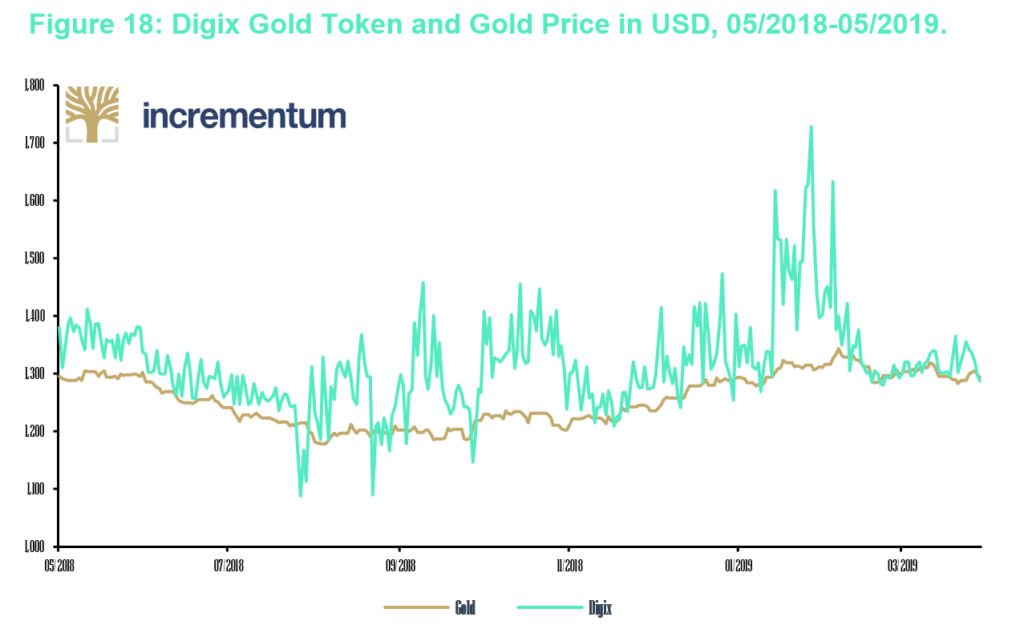

There are three main types of centralized, collateralized stablecoins: fiat, commodity, and crypto. Gold-backed cryptocurrencies are considered to be centralized and “off-chain-backed coins.” The most famous gold-backed cryptocurrency is the Digix Gold Token (DGX). DGX has a market capitalization of approximately USD 4mn and a daily trading volume of approximately USD 240,000 over the past year. Even though Digix is backed by gold, it often trades at a discount to gold, and Digix’s return is extremely volatile compared to gold’s return.

Gold-backed cryptocurrencies have higher costs and risks than ETFs and managed gold funds. Investors can suffer loss of value due to faulty private key storage, double-spends from weak blockchain security, regulatory uncertainty, lack of liquidity, and non-transparent accounting of gold vaults.

The first version of this article originally was published in the sister report of this publication, the In Gold We Trust report 2019. Interested readers can download the publication here: https://ingoldwetrust.report/

Last

year in the sister report of the Crypto Research Report called In

Gold we Trust, we featured an article exploring the intersection between gold

and Bitcoin.[1]

The article focused on how gold impacts Bitcoin’s application as a global store

of value. Now an even newer competitor

to gold is emerging: stablecoins. Stablecoins promise to improve on gold by

being digital and to improve on Bitcoin by being stable. But can the companies

behind these stablecoins deliver or are they just modern alchemists? This

chapter gives a rundown of the stablecoin market with a focus on gold-backed

stablecoins, which are in many ways similar to gold ETFs. Bottom line: All of the gold-backed stablecoins on the market are

centralized, which means they have counterparty risk. Unlike storing your own

physical gold, trusting a company to store your gold is required.

Gold has fascinated mankind for thousands of years. So far, more than 190,000 tons of the precious metal have been mined.[2] How much is still underground remains unknown. One thing is clear, however: The extractable quantity is finite and subject to diminishing returns. Similarly, the number of bitcoins that can be mined is limited: The mysterious inventor of Bitcoin has set the maximum amount to 21 million coins.[3]Unlike fiat money, gold and Bitcoin cannot be created by central banks at will in response to demand shocks. While the average annual growth rate of the gold supply is around 1.7 % with a rather small standard deviation,[4] Bitcoin’s inflation rate is currently 3.69 % and on a downward trajectory.[5] As mentioned in last year’s In Gold We Trust report, the supply of newly mined bitcoins follows a preprogrammed, transparent, and predictable schedule, which remains unaffected by fluctuations in demand.[6]Their inelastic supply makes the prices of gold and Bitcoin dependent on their demand.

Overall,

the supply trajectories of Bitcoin and gold show that Bitcoin is expected to

have a lower inflation rate by 2021. Every

210,000 blocks, the reward the miners receive per block is halved. This

roughly corresponds to a four-year “half-life.” Observers pay very close

attention to the schedule, because the so-called “halving” is regarded as an

important indicator of price movement. There is only little experience so far,

since there have been only two such “halvings.” But they show that the price

has always risen in the months before the actual event. Specifically, the

Bitcoin price found its bottom in the first bear market that came 378 days

before the first halving and again in the second bear market, 539 days before

the second halving.[7]

This equals an average of 458 days, and we are currently approximately

350 days from the next halving, which will probably take place towards the end

of May 2020. If the pattern observed so

far is confirmed, the bottom should have occurred somewhere between December

2018 and May 2019.

Source: bitcoinblockhalf.com, World Gold Council, Incrementum AG.

When we compare the supply of gold to the supply of Bitcoin, we notice

that both are being mined, albeit in their own particular ways. Gold can be

found in soil, rivers, and rocks all over the world, regardless of borders.

Similarly, independently of their location, Bitcoin miners receive a reward for

providing the network with computing power to verify and settle transactions. The main difference when it comes to mining

is that mining is what secures the Bitcoin network and the price of Bitcoin on

the market. In contrast, gold mining does not secure the price of gold.Therefore, we would like to make the subtle

distinction that Bitcoin is not a bearer instrument in the same sense that gold

is. Paying with gold requires absolutely no dependence on a network for

settlement. However, Bitcoin transactions can take hours to settle; and

trusting the software, hardware, and internet that support Bitcoin is a type of

counterparty risk even though the “party” is not human.

To make Bitcoin and gold even more scarce, a certain amount of Bitcoin

and gold becomes unusable every year. Previously, gold was used in quantities

that made smelting and recovery cost-effective and common. For example, the

gold in your mother’s necklace may well have in it metal mined by the Romans,

then used by the Tudors, etc. Now we see gold used in tiny amounts in high-tech

goods, amounts that may not be cost-effective to salvage for a long time. The British Geological Survey estimates

that around 12% of current world gold production is being lost for this reason.[8]This means gold is being consumed in

an absolute sense for the first time in history. Again, this is similar to

Bitcoin’s annual loss of coins that are unspendable due to lost private keys

and fat-finger mistakes while typing cumbersome recipient addresses. Two

different cryptocurrency researchers, Chainanalysis and Unchained Capital, have created an upper bound of 3.8 million

for the total number of Bitcoins lost.[9]

Overall, the supply trajectories of Bitcoin and gold show that Bitcoin is

expected to have a lower inflation rate by 2021.[10]

Since many young investors consider Bitcoin to be

digital gold with a payment option, some may suspect that the demand for gold

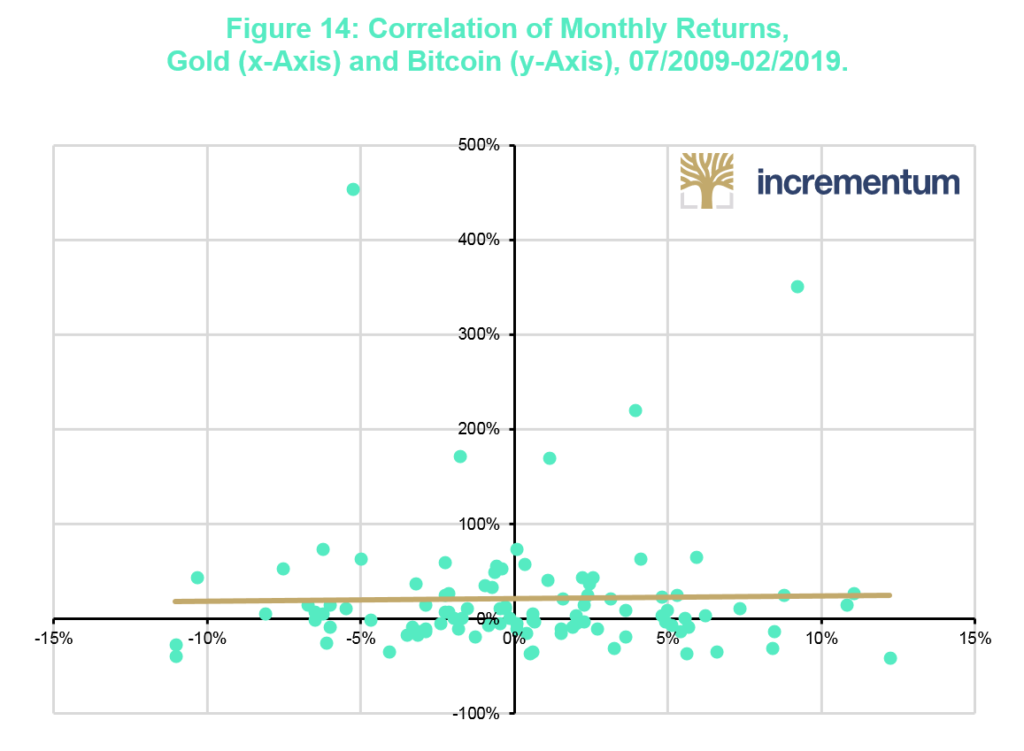

is adversely affected by the success of cryptocurrencies. As of yet, the correlation between gold and Bitcoin returns is still

low and slightly positive, indicating that the demand for gold is not adversely

affected by cryptocurrencies.

Source: Coinmarketcap, Gold.org, Incrementum AG.

This

secure demand strength of gold is due to the unique advantages it has over

Bitcoin. First, gold is far less volatile than cryptocurrencies and will

remain so for the time being. In 2017, Bitcoin was about 15 times more volatile

than gold. In addition, gold is much more liquid. On average, USD 2.5bn in

Bitcoin is traded daily.[11]

This amounts to just 1% of the total gold market: The daily trading volume of

gold is around USD 250bn. Furthermore, gold trades in regulated and

well-established venues and has long been accepted by institutional investors

as an investment alternative. This is not the case for cryptocurrencies.[12]

The US dollar’s hegemony is under increasing

pressure from China and Russia, as US national debt reaches record highs. Instead of returning to a gold standard in

support of a fiat currency, the 21st century could witness the

emergence of a gold standard involving a cryptocurrency.

The notion of a monetary system based on a cryptocurrency may be

surprising, given the fact that cryptocurrencies are the most volatile asset

class. Many Bitcoin holders have experienced a ride from USD 1,000 right up to

USD 20,000, and then steadily back down, culminating in a long, choppy sideways

market followed by the recent rally to USD 8,000. Enter stablecoins. Stablecoins promise to offer all of Bitcoin’s

benefits while fixing the problem of volatility.

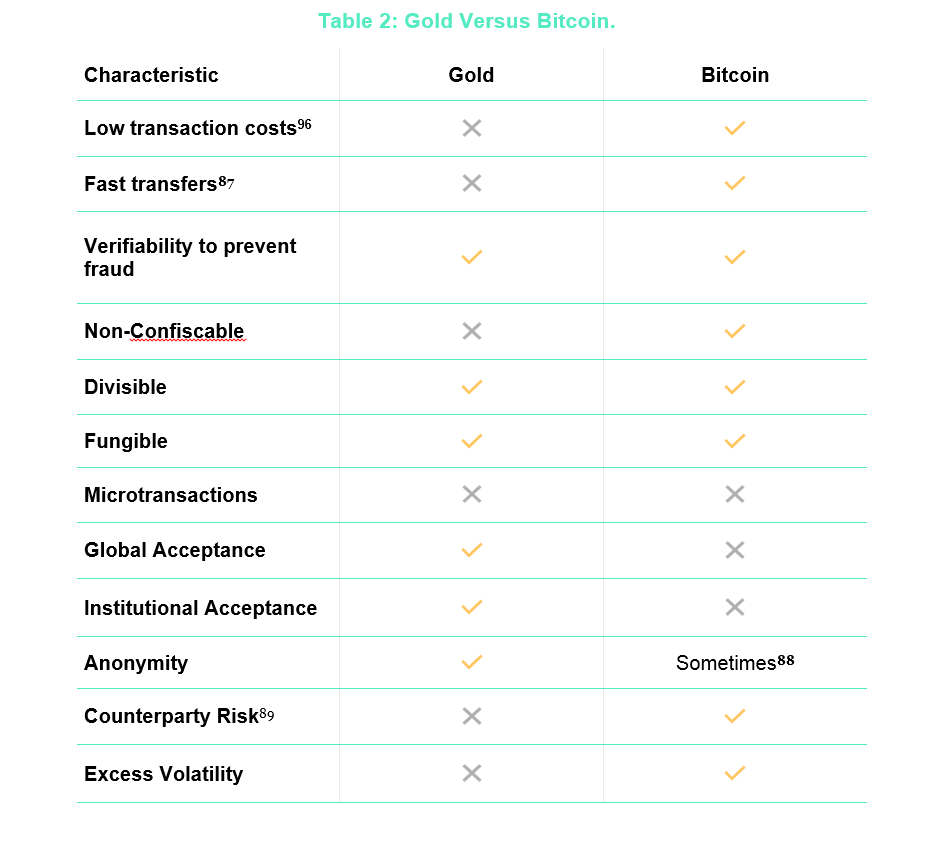

While the decentralized and independent nature of their supply makes

gold and Bitcoin good stores of value, there are major differences with respect

to other monetary features. Following Dobeck and Elliott[13]

and Berentsen and Schär[14],

the next table gives a quick overview.[15]

Source: Incrementum AG.

However, the promise is most likely to be optimistic, as promises often are in the cryptocurrency space. For several decades, countries around the world have tried to peg their exchange rates to other more stable currencies. Not a single fixed peg has lasted in the long run.

Take for example the European Exchange Rate Mechanism (ERM), which

attempted to keep the plethora of European currencies within a narrow band of

each other during the ‘80s and ‘90s. Since the UK could not keep their print

presses turned off, George Soros and other speculators were able to mount a

speculative attack and profit from breaking the peg. This is because whenever a currency holds fractional reserves,

arbitrage opportunities arise between it and other currencies. Therefore,

stablecoins that are not fully backed are trading off between stability in the

short run and blow-up risk in the long run, because keeping a fixed peg without

investing in the underlying asset makes the peg fragile to black swan events.

Source: Incrementum AG

However, Bitcoin is volatile, and many cryptocurrency users are now

demanding stability. To meet this

demand, the new stablecoins are combining the advantages of gold and Bitcoin.

Gold-backed stablecoins are similar to gold ETFs. For example, the most famous

gold ETF, SPDR Gold Shares (GLD), is a fund that buys physical gold and divides

the ownership of it into shares.

In theory, gold-backed cryptocurrencies are supposed to work the same

way. However, there are currently no

cryptocurrency exchanges that are licensed to trade tokenized ETFs. Even if

regulators eventually approve an application for such an exchange, they will

require KYC/AML on each transaction.[19]

This begs the question: How is a

centralized gold-backed stablecoin any better than a gold ETF?We have still not found a suitable answer

to this question. In fact, the solution seems inferior at first glance,

because investors still have to safely protect the private keys that control

the gold-backed stablecoins, and if the tokens are traded on a public

blockchain like Ethereum, then the coins will be subject to volatile and

increasing transaction fees when they send and receive the gold tokens. Then

there are all of the problems associated with public blockchains, such as

latency, lack of scalability, and security.

As shown on the next figure, there are three main types of

collateralized stablecoins: fiat, commodity, and crypto. Gold-backed cryptocurrencies are considered to be centralized “off-chain-backed

coins” because they generate value by a counterparty’s depositing gold, gold

certificates, or other gold-related securities into a vault. Similar to

fiat-collateralized coins like the infamous Tether, gold-backed

cryptocurrencies are supposed to be listed on cryptocurrency exchanges so that

gold positions can be opened and closed within seconds by retail and

professional investors alike.

Over 50 cryptocurrencies are

somehow backed to gold. The next section summarizes just a handful of the

gold-backed projects. The projects selected were drawn from responses to an official

@CryptoManagers tweet

on Twitter. We asked our followers what coins they wanted to learn more about.

We also selected a few coins from the German-speaking countries, including

Vaultoro, Novem, and AgAu. Finally, we have included an update on the

gold-backed tokens that we covered last year.[20]

Source: Incrementum AG.

*Please be advised that the table includes fees

such as transfer fees, custody fees, subscription fees, and redemption fees. We

included all information which was provided to us by the companies. However, a

substantial cost that investors will have to bear may be the spread between the

price of gold on the market and the price of gold that each company charges

investors. This markup on the price of

gold is often not stated clearly in the whitepaper. The table is not

complete because the information was unavailable. Readers are responsible for

their own due diligence on each firm, and this is not investment advice.

Digix

Gold Tokens (DGX)

There are two tokens

associated with this company: DGD and DGX. The DGD crowdsale in March 2016 was

the first crowdsale and major DAO hosted on the Ethereum network. A

decentralized autonomous organization (DAO) is a type of decentralized application

(dApp) that allows owners to make business decisions by voting electronically,

and execution of the business decisions is performed using smart contracts.[21]

The second is the DGX token, which equals one gram of standard gold.[22]

The company reportedly procures its gold from LBMA-approved refiners. The

tokens are issued by Pte. Ltd. in Singapore, and the gold is stored at The Safe

House in Singapore. As you can see in the next chart, the daily trading volume

is approximately USD 243,000 over the past year, and USD over the past month.

The next chart shows that the Digix Gold Token is not correlated with the price

of gold. The token is more volatile and often trades at a discount to gold.

AnthemGold

What makes

AnthemGold unique is that it is the first insured, fully gold-backed stablecoin

based in the US. The token is open to citizens of 174 countries, and the vault

where the gold is stored can be viewed on video, on the AnthemGold homepage.[23]

Currently, there are 20kg of gold there. The gold is insured through Lloyd’s;

there is zero FACTA reporting required for investors; and according to the

founder of AnthemGold, Anthem Blanchard, the gold has zero risk of bank deposit

freeze or closure. There is a 0.40 % storage cost per year, extracted from

metal (which is the same as the GLD gold ETF fee structure).[24]

AgAu

AgAu is a gold-backed token that is being developed by

Thierry Arys Ruiz and Nicolas Chikhani, the former CEO of Arab Bank in Geneva.

Their offices are located at the Zug-based blockchain incubator, Crypto Valley

Venture Capital (CV VC). Their coin will be audited by E&Y and built as an

ERC-1400 smart contract on the Ethereum blockchain. The gold is 1 kg LBMA bars

stored at Trisuna in Liechtenstein. AgAu will be engaging in a token generation

event (TGE) to raise the initial round of capital that will be used to buy the

gold required for backing the tokens. The storage fees are 0.2 % per annum, and

each transaction has a maximum total cost of 0.4 %.

HelloGold, a Malaysian-based company founded in 2015, offers a token

backed by 1 gram of 99.99 % investment-grade gold. The tokens can be converted

into physical PAMP Suisse gold, and the shipping is insured. The total GBT

supply is limited to 3,800,000 (representing 3.8 tons of gold). Users also have

the opportunity to convert their gold into a digital gold token (GBT) if they

have a “pro” account, which requires standard AML/KYC. This enables them to use

the stored gold as a value outside the HelloGold system.

In addition, people may use their gold as collateral for loans made available by Aeon Credit Services, giving them access to personal finance. Finally, HelloGold offers a Smartphone app with which users can trade their tokens and exchange them for their corresponding shares of investment-grade gold. When they redeem their GBTs for physical gold, they receive the corresponding amount in bullion, coins, or jewelry via recorded mail.

GBT accounts are charged an

annual fee of 2 %. Interestingly, the HelloGold blockchain operates on a

private network to reduce fees and transaction latency and avoid the risk of

independent developers adding their own contracts to the blockchain. This means

that HelloGold and its nodes control block times as well as the execution of

the gold transactions.

Due Diligence on Gold-Backed Stablecoins

Can the cryptocurrency be converted into physical gold on demand? How easy is the process?

Does the company disclose how it stores the gold?

Who is storing the gold that backs the cryptocurrency? Is that company trustworthy?

Is the gold insured?

Does the company have a well-known and reputable auditor? If the company is not audited, then it can easily issue more tokens than gold, thereby creating fractional reserves.

What happens if the company goes bankrupt? Is it a limited liability company that could leave investors empty-handed?

What blockchain are the gold tokens built on? Is that blockchain secure?

Do you know how to store the private key to the wallet that controls the gold tokens? What happens if you lose the key? What happens if the key is stolen?

Gold-backed cryptocurrencies are similar to ETFs, which may make them subject to securities laws in Europe and the US. Is the company selling the cryptocurrency regulated? Does it store the gold in a country that has approved their token?

Where can the gold-backed token be traded? Gold ETFs are traded on exchanges, but there are currently no cryptocurrency exchanges that are licensed to trade tokenized ETFs.

How much liquidity does the gold-backed cryptocurrency have? Can you really close a position in case of a liquidity trap? The largest gold-backed cryptocurrency, Digix Gold Token, has a small daily trading volume of USD 243,000 over the past year, and USD 27,000 over the past month.

What is the total expense ratio for the tokenized shares of the gold fund? The most famous gold ETF, SPDR Gold Shares, has a management expense ratio (total fund costs / total fund assets) of only 0.40 %.

What is the business model of the coin? How do the people who created the coin make money? If there is not a clear way that they are profiting, then be suspicious of indirect costs or high risk.

Conclusion

A gold-backed cryptocurrency promises to be digital gold: no

weight and stable. However, no one has figured out yet how to make a

decentralized gold-backed stablecoin. All gold-backed stablecoins are

centralized in the sense that you have to trust someone to store the gold for

you. Similar to an exchange-traded gold fund, gold-backed stablecoins have

counterparty risk. In the cryptocurrency world they say, “Not your keys, not your crypto.” Well, the parallel for gold would

be something like, “Not your vault, not

your gold.”

Backing a cryptocurrency in a way that an intermediary is required – a custodian or a bank for instance – actually conflicts with one of Bitcoin’s central tenets, namely, that users do not have to trust any intermediary. The security of Bitcoin and other cryptocurrencies is based on cryptographic technology. In contrast, the gold-token projects we have presented above are managed by real companies. They are responsible for the safekeeping of the gold. Therefore, the user has to trust that no state or private actor will be able to steal or confiscate the gold from the vaults.

Furthermore, the coins are often traded on a public blockchain structure such as Ethereum, which means the coins also suffer from all of Ethereum’s problems, such as scalability and security. Finally, there are over fifty gold-backed coins currently, and most likely, many of them will fail. It will take a few years for the market leaders to emerge, gain widespread exposure, and thus secure the standing of gold-backed tokens as a store of value. This year will be pivotal in identifying which projects are going to take the lead in this endeavor.

[3] In this context, we should note that the edge

length of the cube that could be cast from the total amount of gold already

mined is roughly 21 meters, which may have been Satoshi Nakamoto’s inspiration

for the arbitrary 21 million hard cap.

[12] This may change quickly, however, as more and

more countries open their financial markets to blockchain-related investment

vehicles. To give an example, the Liechtenstein Financial Market Authority

(FMA) has recently approved three alternative investment funds (AIFs) for

crypto-assets. See “Liechtenstein gives green light to crypto

funds“, Liechtenstein.li –

official website of Liechtenstein Marketing, March 6, 2018

[13] Dobeck, Mark F.; Elliott, Euel: Money.

Greenwood Press, 2008, pp. 2-3

[14] Berentsen,

Aleksander and Schär, Fabian: Bitcoin, Blockchain und Kryptoassets. 2017, pp. 16-17

[15] This table was inspired by a presentation

given by Frank Amato at the LBMA/LPPM Precious Metals Conference 2018 in

Boston, Massachusetts.

[17] Transfers within the Bitcoin network can be

tracked indirectly due to the transparent nature of account balances. Companies

such as Chainanalysis offer to analyze the entire Bitcoin blockchain in order

to forensically detect transfers between addresses and identify the owners of

the accounts. The US tax authorities are already using this service to track

cases of money laundering and tax evasion.

[18]

The counterparty of Bitcoin defined as functionality of the Network

[19] Know your customer (KYC) and anti-money

laundering (AML) are standard protocols that require a customer to verify their

identity in order to use specific services, such as bank accounts and

cryptocurrency exchanges.