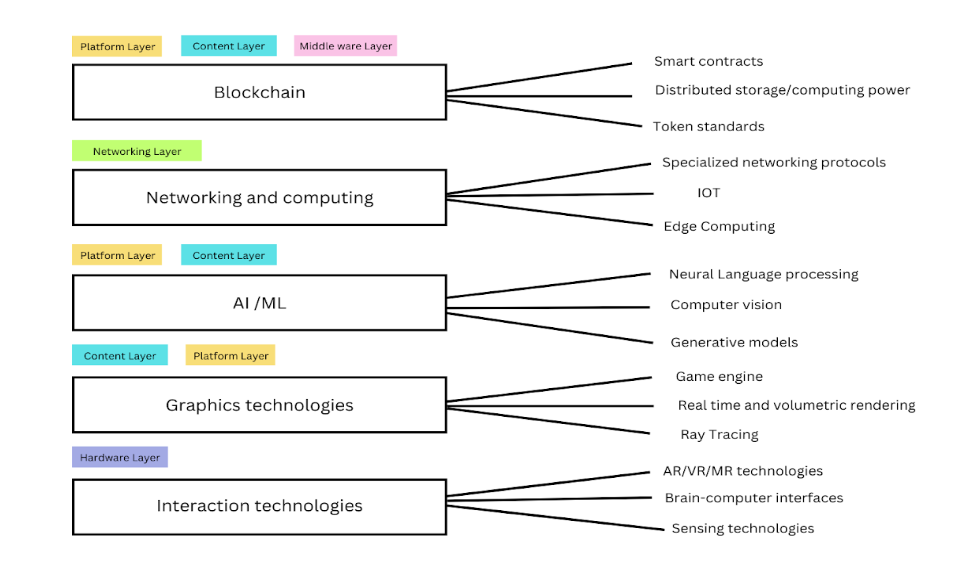

The metaverse technology, a blend of various hardware and software components, is a complex system enabling the creation, management, and experience of virtual spaces. It contains five key layers: platform, networking, middleware, content, and hardware.

The metaverse technology stack is an intricate system that encompasses a diverse array of hardware and software components. From virtual and augmented reality devices to cloud computing platforms, blockchain-based digital identities and AI-powered virtual environments, the metaverse stack is multifaceted and complex.

At a high level, the metaverse stack can be divided into several distinct layers:

Platform layer: At the platform layer, we have software that enables the creation, management and hosting of virtual environments and assets. These platforms could be centralized like Second Life or decentralized like The Sandbox.

Networking layer: This layer encompasses the infrastructure that facilitates communication and data transfer between devices and servers in the metaverse. This includes well-known protocols, such as TCP/IP and HTTP, and specialized protocols, such as WebRTC, for real-time communication.

Middleware layer: The middleware layer comprises software components that provide essential services, such as identity management, payments, APIs and social networking within the metaverse. Examples of metaverse middleware include identity systems like High Fidelity and wallets like MetaMask.

The content layer: This is where the magic happens. This layer consists of the virtual assets, environments and experiences that are created by users and developers within the metaverse. From virtual clothing and accessories to fully interactive games and simulations, the content layer is where users can truly unleash their creativity.

Hardware layer: This layer consists of physical devices that enable users to interact with the metaverse, including virtual reality headsets, augmented reality glasses and other sensory devices. These devices allow users to fully immerse themselves in the metaverse and experience its wonders firsthand. Devices like Oculus Rift and HTC Vive would fall under this category.

In essence, the metaverse technology stack is an intricate combination of layers that facilitate creation, interaction, and immersion in virtual environments. Each layer, from platform to hardware, plays an indispensable role in shaping the metaverse and the way we engage with it.

Sinum continues to impress us with its updates and by the end of the fourth quarter of 2023, they have already added 15 in-app widgets and are ready to show us two exciting new features – Whales Alert and Sinum Score.

Whales Alert

Active traders who follow the market closely will find this feature particularly useful. Sinum’s in-app Whale Alert Widget is linked to the official Whale Alert API, the leading blockchain transaction data provider, that offers current information on large transactions on the crypto market.

Sinum will notify you immediately via push notifications about the real-time information on these transactions. You also have the option to filter the alerts and create a filter that only notifies you about the tokens you’re interested in. All Whale Alerts are stored in the app as a feed, so it’s easy to view and analyse the Whale transaction history. As a Sinum app user, you can trust the Whale Alert to keep you informed about market changes.

As a result, you can better anticipate price changes and take timely action without the loss of crucial opportunities. And indeed, traders will find it useful. Imagine receiving the alert, rethinking your trading strategy and swapping tokens without wasting a minute. And all without leaving the app. It’s great to see how the Sinum widgets aren’t just a set of functions, but they’re linked to each other, providing a vast range of possibilities for using the app.

Sinum Score

This will surely prompt you to get the app. Sinum has introduced a new feature, Sinum Score, that allows users to earn points for using the app and on-chain activities. Opened a widget for the first time? Earn points. Swapped tokens in the in-app token exchange? Earn points for that too. With this new feature you’ll be rewarded for discovering all the obvious and the hidden features. This makes the app more like a game. Stay tuned for project announcements, as these points will be able to be exchanged for rewards in the future.

Sinum Score also includes a leaderboard that shows the top users of the app throughout the week and all time. Take part in activities and use different features of the app to earn points and take first place.

With Sinum Score, your user account goes from being a plain wallet address to something much more. It turns into your personal page with rankings, total points earned, achievements and the history of your on-chain activities. Update your profile and share your achievements with your friends, on social media and in the Web3 community. Use your profile as your personal calling card to show your experience and reliability in the blockchain space.

Outro

As you can see, Sinum is truly built as an ultimate web3 app that not only provides various interconnected widgets and features to help you in the crypto market but also makes your daily activities enjoyable and rewarding.

Sinum app is already available for download on GooglePlay and AppStore, so you can be one of the first to try out the new features.

Navigating the digital waters of the metaverse, investors are on the lookout for potential goldmines. Big players like Meta are already investing heavily, but finding a company solely focused on the metaverse is still elusive. This piece aims to guide you on spotting both publicly listed companies and greenhorns in this exciting new realm.

Publicly traded companies are usually maturer than their tokenized counterparts. As of now, we don’t know of any company that focuses exclusively on the metaverse.

Meta (formerly known as Facebook) is definitely pouring tons of money into the development of the technology and user experience around that subject but, so far, has seen little success, much to the chagrin of shareholders.

Please check out section 4.2 of this report for the top publicly listed companies in this space. This section will focus on finding the newcomers. DefiLlama(1) has a section that features recent raises and gives you some details about the companies.

You can use the search function of your web browser to find metaverse-related raises and follow companies to see when they’re doing an initial public offering (IPO).

A good old internet search for “new metaverse stocks” will also surface numerous websites that give you the low down on incumbents and newcomers alike.(2)

If you’re already an active investor, you’ll likely have a go-to list of stock-picking websites like the Motley Fool or Liberated Trader that you frequent. Searching for metaverse stocks there might surprise you.

Watching sites that cover new IPOs and researching companies is also a good way to get in as early as possible, but of course, this requires a certain amount of time dedicated to the process.(3)

You can also leave the research to dedicated professionals and buy one of the ETFs or other funds in our section 4.3 to get exposure to the metaverse with minimal upfront work.

Of course, Cointelegraph will report on metaverse IPOs on its news site — definitely worth watching.

Investing in the metaverse is no child’s play; it requires vigilance and knowledge. From using websites like DefiLlama to tracking IPOs, there are several ways to stay informed. Alternatively, ETFs and other funds offer a less labor-intensive option. With news sites like Cointelegraph, keeping up with metaverse IPOs becomes a breeze. As we plunge deeper into the metaverse, the key to success lies in staying ahead of the curve.

The metaverse, a burgeoning frontier of digital interaction, offers exciting opportunities through project tokens and stocks. This article guides you to resources like Cointelegraph, CoinGecko, and CoinMarketCap for the latest metaverse news and trends. DappRadar provides key metrics for DApps, while Twitter influencers offer additional insights. However, due to the risks associated with smaller projects, thorough research is paramount.

So, you want your slice of the metaverse? Eager to stake your claim in these new lands? We got you covered. This section will equip you with the tools you need to find out about new metaverse project tokens and stocks.

Let’s start with tokens. As we discussed earlier in this report, tokens are usually the hallmark of Web3 metaverse projects, such as Illuvium or Decentraland, whereas some Web2 projects come from publicly traded companies, like Meta.

First, Cointelegraph’s excellent coverage of current affairs lets you search for the term “metaverse” so you’re the first to know if a new project launches.Price aggregator CoinGecko has a distinct metaverse section that you can sort by performance to see trends.

Watch out, because there are some microcaps in there that are likely very risky to hold because liquidity will be very constrained. This is not financial advice, please do your own research.

CoinMarketCap(1) also has a metaverse section and has slightly higher market cap requirements. CMC charges coins for listings, which also means you might miss some grass-roots developments that do not want to pay to play.

Last but definitely not least is DappRadar(2), which focuses on important metrics for DApps, like unique active wallets (UAWs) and balance (TVL for games). DappRadar is a great place to check if projects are getting traction.

Following Twitter influencers isn’t a bad idea, either. Zeneca.eth(3) and his Zen Academy are a good place to start. Punk6529(4) and 1990s rapper MC Hammer have surprisingly deep NFT and metaverse know-how.

In conclusion, the metaverse presents a thrilling new chapter in digital interaction. With the right tools and resources, you can navigate this evolving space and potentially become a pioneer in this digital landscape.

The metaverse, a digital universe that mirrors our own, is attracting significant interest from investors. This article explores the two main types of funds investing in this emerging space: exchange-traded funds (ETFs) and venture capital (VC) funds. ETFs primarily invest in established, publicly-traded companies, while VC funds support businesses at various stages of development, often with a focus on early-stage financing. While VC funds are typically closed to the public, they can provide valuable networking opportunities and significantly increase a project’s chances of success.

Funds that invest into metaverses come in two major categories: exchange-traded funds (ETFs) and VC funds. ETFs deal with already public companies that have matured for longer, while VCs fund anything from angel rounds to later stage financing rounds. Most VC funds are not open to the public, though. Nevertheless, the involvement of a top-tier VC usually boosts a project’s popularity and chances of success. Good VCs also bring a considerable network to the table that portfolio companies can tap to get ahead.

We found the following ETFs investing decidedly into metaverse stocks:

Fidelity Metaverse ETF (FMET)

Roundhill Ball Metaverse ETF (METV)

Global X Metaverse ETF (VR)

Ishares Future Metaverse Tech And Communications ETF (IVRS)

Evolve Metaverse ETF (MESH)

Subversive Metaverse ETF (PUNK)

ProShares Metaverse ETF (VERS)

Horizons Global Metaverse Index ETF (MTAV)

Most of these ETFs contain Nvidia, Microsoft and Meta, but some have interesting additions, such as TMSC or Block Inc as well as Cloudflare. It would be easy to portray these efforts as bandwagonning, but they do offer decent exposure to a relevant portfolio in one easy swoop. What’s not to like?

Regarding VCs that invest into metaverse projects, we can finally bridge over to the Web3 and token world. Many VCs had invested into token based projects even before Facebook rebranded to Meta and a flurry of others followed shortly thereafter.

The top funds are:

a16z

Polychain Capital

Sequoia Capital

Archetype

Dragonfly Labs

And many exchange investment arms like Binance Labs, KuCoin capital and others.

These funds invest into token-based projects like The Sandbox but also into GameFi and other VR projects. The beauty of the VC model is that only one in a couple of checks has to make it big to validate a fund, which allows this kind of capital to finance multiple pathways to metaverse adoption at the same time.

Recently, investors have not looked upon Facebook’s rebranding as Meta with favor, but we the jury are still out if the claim staking by CEO Mark Zuckerberg was not a great move in the end.

In conclusion, the metaverse represents an exciting new frontier for investment, with both ETFs and VC funds playing crucial roles in its development. Despite some skepticism regarding Facebook’s recent rebranding to Meta, it’s clear that many investors see potential in the metaverse space. With diverse portfolios that include both established tech giants and innovative start-ups, these funds offer multiple pathways for metaverse adoption. The future of the metaverse is still being written, but one thing is certain: investors who understand this space will be well-positioned to benefit from its growth.

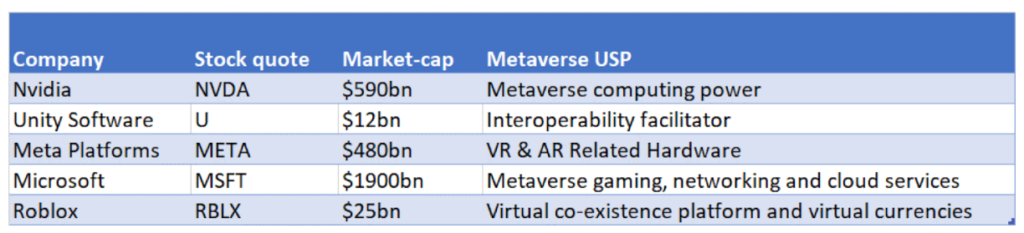

Metaverses are fluid entities, constantly reshaped and redefined by multiple players. The technologies propelling these virtual universes today might be starkly different from those in use a decade or so down the line. This article discusses five public companies – Nvidia, Unity Software, Meta Platforms, Microsoft, and Roblox – that are making significant strides in shaping the metaverse.

Passive observers of the metaverse may ostensibly be prone to perceiving this buzzword as a destination, or an end-game, with a “winner-takes-all” ethos serving as the overriding motivation of competing entities in this space. The reality, though, is that metaverses are still very fluid, with multiple entities altering and shaping their contours by the day. Besides, the optimal mix of underlying technologies that buttresses a paradigm of the metaverse in 2037 could be very different from what’s deemed as credible in 2023. Thus, in the context of what we’ve just laid out, we think the following publicly listed entities may be worth considering for the medium term.

Nvidia

Nvidia specializes in the design and development of high-performance 3D graphic processing units (GPUs) that will be instrumental in proving the necessary processing power to ensure seamless interactions with the virtual environments of the metaverse. Crucially, Nvidia’s Omniverse platform gives users a gateway to metaverse applications and is already being used by auto and defence stalwarts in areas such as virtual factory planning, simulation, etc.

Having great plans for the metaverse is one thing, but Nvidia also has the necessary financial chops to fund its transformative metaverse ambitions; for context, this is a business that has generated positive free cash flow (FCF) every year since 2010.

Unity Software

One of the biggest hindrances to further metaverse adoption lies in the interoperability deficit of this universe. Put another way, we have a lot of metaverse platforms that offer immersive experiences in isolation, but the interconnectedness of these experiences across platforms is still a challenge.

Unity Software could play a key role in bridging that deficit as it already provides a developer platform called UDP, which enables gaming developers to construct one version of a game that can then be distributed and managed across multiple platforms. Unity’s IP, which has a high flexibility quotient, isn’t limited to gaming alone and can be used in a range of industries encompassing the film industry, manufacturing, construction to name a few.

It’s also worth noting that Unity is one of the founding members in the establishment of the Metaverse Standards Forum and will likely play a key role in establishing consistent standards that could facilitate interoperability in the open metaverse.

Meta Platforms, Inc.

Meta Platforms is currently in the process of building VR- and AR-related hardware that could be integral to accessing and interacting with the metaverse. Separately, this hardware could also be used to conduct immersive work experiences or conduct court hearings virtually.

While a number of mega-caps are making a splash in the metaverse, it is arguable whether there are too many of them that share the heightened level of fidelity that Meta Platforms has to the metaverse. From rebranding itself to Meta in 2021, to burning over $10 billion a year ($13.7 billion in 2022) in Reality Labs (the metaverse division) alone, there is an inherent seriousness with which the company is tackling its ambitions in this space.

Microsoft

Microsoft will have its foot in the door across multiple facets of the metaverse. Key applications include gaming, networking and enhancing 3D virtual environments with low-latency cloud support.

Microsoft’s inherent financial muscle shouldn’t be played down and will enable the company to engage in big transformation projects in the metaverse, either organically or inorganically (something akin to Activision Blizzard). For some context, Microsoft’s cash on its balance sheet has consistently exceeded its level of debt, whilst its operating profits have comfortably covered its interest bill by 30x over the last decade.

Roblox

The metaverse needs non-physical, immersive platforms where humans can create, socialise, transact and engage in various virtual experiences at ease. This, in a nutshell, is what Roblox offers, and what’s key is that it has already amassed around 58.8 million daily active users on its platform.

This isn’t just a platform where one gets to engage in traditional gaming applications; rather, users also have the option of programming games, creating content and monetizing their efforts via a virtual currency called “Robux.”

In conclusion, the metaverse is not a distant reality but a rapidly evolving space. Companies like Nvidia, Unity Software, Meta Platforms, Microsoft, and Roblox are not only contributing to its development but also actively shaping its future. Each company brings unique capabilities, from high-performance GPUs and developer platforms to immersive hardware and engaging social platforms. With their financial strength, technological prowess, and forward-thinking strategies, these companies are poised to play pivotal roles in the evolution of the metaverse. As we move ahead, watching how these entities further their metaverse ambitions will provide a fascinating insight into the future of this exciting digital realm.

CAIZ is at the forefront, preparing to launch its innovative Remittances and International Payments service. This service is designed to meet the growing demands of users seeking efficient, affordable, and secure international transactions. Whether facilitating business payments or personal remittances, CAIZ’s new offering promises to set a new standard in the realm of international financial transfers.

Key Features and Unparalleled Benefits

Central to this service is a suite of features tailored to enhance user experience and trust. Transactions are not only swift, completing in seconds, but also cost-effective with fees ranging from 0.1 to 0.25% of the transaction volume. Users can send fiat currencies such as EUR and USD with ease. On the receiving end, individuals can opt to retrieve the original fiat or exchange it economically to their domestic currency. An added advantage is the option to retain funds within the CAIZ ecosystem in the form of a stablecoin, serving as a safeguard against inflation, or to utilize it in CAIZ Gold for future use.

Commitment to Compliance and User Trust

To ensure a smooth and compliant user journey, the service mandates a full account registration, including passing KYC procedures, as part of the onboarding into the CAIZ ecosystem. This rigorous process underscores CAIZ’s commitment to full verification, transparency, and adherence to both Islamic Financial law and local domestic laws. Users can rest assured knowing their funds remain untouched and readily available during transit, with no hidden tactics or covert methods employed.

The Road to Mainnet Launch

The excitement within the CAIZ community is building as this service is slated to be the inaugural product released once CAIZ’s blockchain/mainnet becomes operational. This milestone is not just a testament to CAIZ’s technological advancements but also its dedication to providing solutions that resonate with users’ needs and values.

Conclusion

With the impending launch of the Remittances & International Payments service, CAIZ is not just introducing a product but a vision for the future of international finance. This vision is rooted in understanding the intricate needs of users and bridging the gap between technology and trust. As CAIZ continues its journey, it remains steadfast in its mission to empower users with tools that are both cutting-edge and deeply aligned with their values. The horizon looks promising, and CAIZ invites its community to be part of this transformative endeavor.

About Caiz

CAIZ stands out as the leading Islamic-compatible Blockchain ecosystem rooted in the EU and is envisioned to be the bridge between the centralized and decentralized financial world.

In the rapidly evolving world of cryptocurrency, a new frontier has emerged that is piquing the interest of investors worldwide – metaverse tokens. These digital assets, which are associated with virtual worlds and online communities, have witnessed significant traction in recent years. As these metaverses continue to grow and integrate with various aspects of our daily lives, from gaming to social interactions to business, their associated tokens are becoming increasingly prominent in the crypto investment landscape. This rise in prominence has resulted in an expanded market with diverse options, offering ample opportunities for savvy investors.

This article delves extensively into this vibrant market, spotlighting the top 10 metaverse tokens as of Q1 2023. These include well-known names such as The Sandbox, Decentraland, Axie Infinity, Enjin Coin, Illuvium, Magic, Merit Circle, My Neighbor Alice, Mobox, and Vulcan Forged. But we’re not just listing these tokens based on their market capitalization. We’re also providing an in-depth analysis of their adoption rates and user metrics. By doing so, we aim to give you a comprehensive overview of their performance, potential, and the trends shaping their trajectory.

Let us dive straight in and unearth a few gems in the form of top metaverse tokens.

Using CoinGecko’s excellent tagging of tokens, we can identify the following top 10 tokens as of Q1 2023:

The Sandbox (SAND): market cap. $1,024 million

Decentraland (MANA): market cap. $961 million

Axien Infinity (AXS): market cap. $878 million

Enjin Coin (ENJ): market cap. $375 million

Illuvium (ILV): market cap. $253 million

Magic (MAGIC): market cap. $239 million

Merit Circle (MC): market cap. $105 million

My Neighbor Alice (ALICE): market cap. $103 million

Mobox (MBOX): market cap. $93 million

Vulcan Forged (PYR): market cap. $79 million

Now, let’s look at adoption and user metrics using DappRadar. We’ll use 30-day metrics across the board

Project Name

Unique Active Wallets

Transactions

Volume

Balance (TVL)

The Sandbox

6.93K

4.71K

5.21M

54.22M

Decentraland

3.52K

50.33K

12.93M

30.06M

Axie Infinity

80.12K

898.78M

88.75M

744.5M

Enjin

N/A

N/A

N/A

N/A

Illuvium

379

683

605.1K

2.64M

Magic

N/A

N/A

N/A

N/A

Merit Circle

4

7

N/A

N/A

My Neighbor Alice

55

97

N/A

15.09K

Mobox

28.21K

414.55K

5.82

38.42M

Vulcan Forged

N/A

N/A

N/A

N/A

Unfortunately, these metrics are hard to compare to DeFi. For example, Balance in Metaverses is similar to total value locked in decentralized applications (DApps). We left out projects that are not DApps, but instead tokens for whole ecosystems, where a major part of the transaction volume comes from swaps and trading on exchanges, instead of in-world activity. Token transaction volume cannot be compared to in game (or in metaverse) transactions. A few striking observations:

Activity on Illuvium is shockingly low, even though the market capitalization of the token is still above $154 million. This could be captive liquidity since Illuvium incentivizes users to lock up tokens for up to four years with massive rewards, or it could be that many holders still believe that the developers will unlock massive success with a token-powered game. Illuvium has recently launched Illuvium: Beyond.

Axie Infinity is still going strong and has a devoted client base.

Decentraland was one of the first distinct metaverse tokens and one of the poster children of the metaverse land gold rush. User activity there has since dropped and continues to shrink.

Enjin and Vulcan Forged are ecosystems of their own with multiple DApps.

My Neighbor Alice is a NFT sharing DeFi game.

How can you, discerning investor, decide whether to buy tokens, considering the above metrics do not apply, though?

Short Primer on Valuing Tokens

When looking at tokens, market capitalization is often seen as a good measure of value. We found, time and again, that market cap is sometimes achieved by mere speculation, without reflecting underlying or intrinsic value. While it is perfectly rational to use market ballistics for investing, we find that most holders overestimate their ability to time the market and get caught in a destructive spiral of FOMOing in much too late and then getting out when they can’t bear the pain anymore.

Experienced investors form opinions that lead to very concrete expressions in the market. Something like: I will buy token X at this price with this exposure and sell at this price with a stop loss at that price.

Most investors want to buy and hold tokens, so we want to give some additional tools that can be used to research possible investments. Please understand that this is in no way an invitation or enticement to actually buy tokens. This remains at the sole discretion and the singular responsibility of the reader.

Liquidity: Using CoinMarketCap, check how much trading volume a certain token has had on what exchanges. See a screenshot below for Illuvium, where you can see $22 million in centralized exchanges volume and $1.6 million in DEX volume. While these are large numbers, they’re paltry compared to major currencies. ETH has $12 billion worth of volume on CEXs and $60 million on DEXs. Stablecoins, meanwhile, have even more.

Liquidity becomes important when buying or selling tokens. Low liquidity means high slippage (or loss from friction) when buying or selling.

Distance from all-time high, all-time low: Where in the history of the token is the current price. If it is close to the all-time high, is there any news that supports this momentum?

News and products: Has a new game or product recently shipped or is expected to boost demand for the token? Has the founding team raised money from a top fund? Has a celebrity publicly endorsed one of the products or the token?

Tokenomics: How much dilution is going to happen going forward, and when is the next big unlock of tokens? This is especially important because a sudden influx of additional available tokens always leads to substantial sell pressure and lowering prices — at least in the short term.

The more research you can put into your purchase, the better. Try to come up with a credible thesis of why you would want to buy a token at a certain price and also define clear targets for selling or at least taking some profit.

In conclusion, investing in metaverse tokens requires a nuanced understanding of several factors, such as liquidity, distance from all-time high and low, news and products, and tokenomics. Market capitalization, while often considered a good measure of value, can sometimes be misleading due to speculative influences. Therefore, it’s crucial for potential investors to conduct thorough research and form concrete opinions before making any decisions. Remember, investing in tokens is not just about buying at a certain price, but also knowing when to sell. With the right tools and knowledge, you can navigate the dynamic landscape of metaverse tokens more effectively.

In this article, we navigate the speculative world of the metaverse, focusing on the tokens of leading platforms, Decentraland and The Sandbox. Our analysis explores land ownership, exchange volumes, net exchange activity, and virtual land speculation trends to understand the primary motives behind acquiring these tokens.

Speculation is an integral part of any new technology, and the metaverse is no exception. Due to the use of blockchain-based tokens, it is even more susceptible to speculation.

To analyze the level of speculation in the metaverse, we have analyzed the tokens of the top two decentralized metaverse platforms: Decentraland and The Sandbox.

Chart 1 shows the percentage of tokenholders who used their tokens to purchase land on these platforms. The ownership of land is low for both MANA and SAND tokenholders, but SAND tokenholders have a higher percentage of ownership than MANA tokenholders in all months. This low level of land ownership indicates that most users are not acquiring these tokens to buy land on their respective platforms.

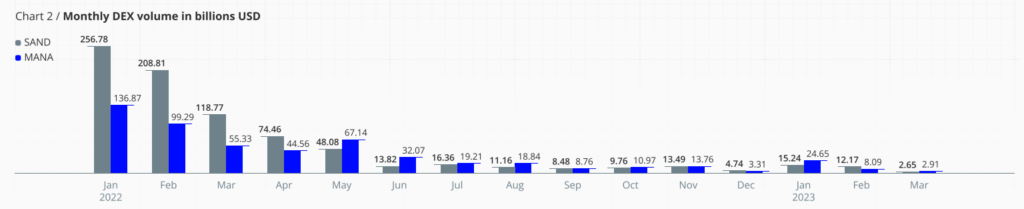

The decentralized exchange (DEX) volume for both tokens has been decreasing over the months and is minuscule compared to the centralized exchange (CEX) volume for the same.

Net exchange activity for both tokens is contrasting, as MANA largely has a net outflow of the token from major CEXs, while SAND has a net inflow. A higher net inflow to CEXs indicates that fewer tokens are being used within the metaverse.

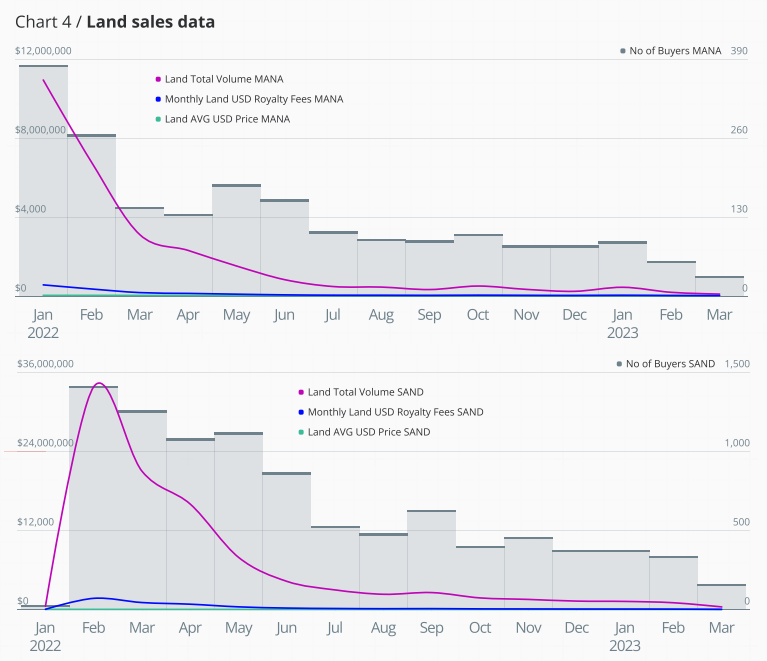

In chart 4, one can observe the speculation in the virtual land of both platforms. The current land sales volume is only a fraction of what it was at the start of 2022.

The average sales value of land has decreased by approximately 89% in Decentraland and 84% in The Sandbox. The number of buyers shows a similar trend.

From the charts, it’s clear that metaverse tokens are still not primarily being acquired to use within the platforms. For most users, these tokens are a means to ride the anticipated growth of the two metaverse platforms. Moreover, as the metaverse platforms become more immersive and adoption grows, speculation will decrease with time.

From our extensive examination, it’s evident that the primary motive behind acquiring metaverse tokens is not yet to utilize them within their respective platforms but rather to speculate on their anticipated growth. Low levels of land ownership, decreasing exchange volumes, contrasting net exchange activities, and diminishing land sales all point towards this conclusion. However, as the metaverse continues to evolve and becomes more immersive, we expect that the level of speculation will decrease over time, paving the way for genuine adoption and utilization of these tokens within the metaverse platforms.

In the fast-evolving world of cryptocurrency, token minting has traditionally been perceived as a complex and intimidating process, accessible only to tech-savvy individuals. However, with the advent of xLFi Minters by LFi, this notion is about to change.

LFi, a trailblazer in the blockchain and fintech arena, is all set to launch a groundbreaking addition to its ecosystem – the xLFi Minters. These innovative hardware devices are designed to make token minting accessible and user-friendly for all, regardless of their experience level in the crypto space.

What is LFi Minting?

Before delving into the specifics of xLFi Minters, it’s essential to grasp the fundamentals of LFi Minting. While it shares similarities with traditional token mining, involving steps such as data verification, block generation, and recording authenticated information on a blockchain network, LFi Minting sets itself apart by leveraging the power of the Proof of Stake (PoS) consensus mechanism.

The PoS consensus mechanism – unlike traditional mining methods that rely on computational power – considers the amount of cryptocurrency an individual holds and is willing to “stake” or lock up as Minting utility Token. This decentralizes and enhances the security of the blockchain network while being energy-efficient.

The Function of Validators

In the world of cryptocurrency minting, validators play a pivotal role in confirming transactions, proposing new blocks, and ensuring the blockchain’s integrity. What makes this process truly remarkable is its decentralization, allowing virtually anyone interested in contributing to the blockchain’s security without the need for intermediaries.

This inclusive approach fosters a more accessible and democratic crypto ecosystem, eliminating the reliance on centralized regulatory authorities.

The Wide Range of Minting Solutions Offered by LFi

LFi understands that the path to financial freedom is a personal journey with diverse preferences and needs. Therefore, LFi offers three distinct methods for token minting:

xLFi Minter: Designed to be straightforward and accessible, xLFi Minter is perfect for newcomers to the cryptocurrency space.

CloudX Minting: A revolutionary system that simplifies and secures the minting of LFi tokens by allowing users to rent minting hardware in remote locations.

LFi One Smartphone: This groundbreaking device is specifically designed to support crypto minting, making it a mobile gateway to the world of decentralized finance.

Introducing xLFi Minters

Now, let’s focus on the latest addition to LFi’s lineup – the xLFi Minters. These dedicated hardware devices come in five versions: xLFi 500, xLFi 1000, xLFi 5000, xLFi 10000, and xLFi VALIDATOR.

Each model is meticulously crafted to facilitate the minting of digital assets, allowing users to choose the one that aligns best with their preferences and requirements.

One of the standout features of xLFi Minters is their user-friendly setup process. Unlike many other cryptocurrency-related hardware devices that demand extensive technical know-how, xLFi Minters are designed to be hassle-free to install.

Even if you’re new to the crypto world, you can set up your xLFi Minter at home with ease. Once installed, the hardware minting process with LFi is initiated automatically, eliminating the need for complex configurations or constant monitoring.

While detailed information about the xLFi Minter’s features is yet to be unveiled, anticipation is building around this new addition to LFi’s suite of minting solutions. LFi is renowned for delivering innovative and user-focused solutions, and the xLFi Minters are expected to be no exception. LFi’s commitment to providing accessible tools for financial freedom is at the core of this new product.

Minting Redefined

As LFi continues to push the boundaries of financial innovation, the introduction of xLFi Minters represents a significant step towards democratizing the token minting process.

These user-friendly hardware devices empower individuals in the world of cryptocurrency, aligning perfectly with LFi’s core philosophy of decentralization and accessibility. The xLFi Minter is a game-changer, making token minting easy and accessible to all, regardless of their experience level.

Stay tuned for updates as this revolutionary technology transforms the crypto world.

About LFi

LFi is a technology company that aims to empower the global fintech movement with new and innovative offerings that combine cutting-edge hardware with next-generation software. Leveraging the power of advanced computing and blockchain technology, LFi seeks to realize a future of financial independence through integrated products and solutions.