In this article, we navigate the speculative world of the metaverse, focusing on the tokens of leading platforms, Decentraland and The Sandbox. Our analysis explores land ownership, exchange volumes, net exchange activity, and virtual land speculation trends to understand the primary motives behind acquiring these tokens.

Speculation is an integral part of any new technology, and the metaverse is no exception. Due to the use of blockchain-based tokens, it is even more susceptible to speculation.

To analyze the level of speculation in the metaverse, we have analyzed the tokens of the top two decentralized metaverse platforms: Decentraland and The Sandbox.

Chart 1 shows the percentage of tokenholders who used their tokens to purchase land on these platforms. The ownership of land is low for both MANA and SAND tokenholders, but SAND tokenholders have a higher percentage of ownership than MANA tokenholders in all months. This low level of land ownership indicates that most users are not acquiring these tokens to buy land on their respective platforms.

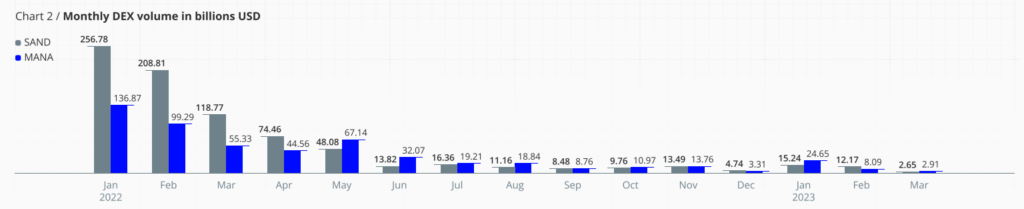

The decentralized exchange (DEX) volume for both tokens has been decreasing over the months and is minuscule compared to the centralized exchange (CEX) volume for the same.

Net exchange activity for both tokens is contrasting, as MANA largely has a net outflow of the token from major CEXs, while SAND has a net inflow. A higher net inflow to CEXs indicates that fewer tokens are being used within the metaverse.

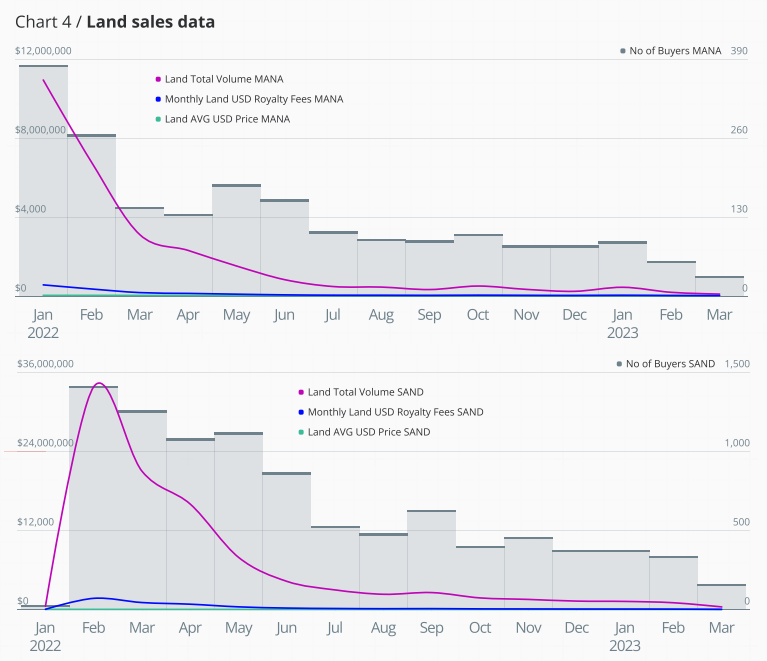

In chart 4, one can observe the speculation in the virtual land of both platforms. The current land sales volume is only a fraction of what it was at the start of 2022.

The average sales value of land has decreased by approximately 89% in Decentraland and 84% in The Sandbox. The number of buyers shows a similar trend.

From the charts, it’s clear that metaverse tokens are still not primarily being acquired to use within the platforms. For most users, these tokens are a means to ride the anticipated growth of the two metaverse platforms. Moreover, as the metaverse platforms become more immersive and adoption grows, speculation will decrease with time.

From our extensive examination, it’s evident that the primary motive behind acquiring metaverse tokens is not yet to utilize them within their respective platforms but rather to speculate on their anticipated growth. Low levels of land ownership, decreasing exchange volumes, contrasting net exchange activities, and diminishing land sales all point towards this conclusion. However, as the metaverse continues to evolve and becomes more immersive, we expect that the level of speculation will decrease over time, paving the way for genuine adoption and utilization of these tokens within the metaverse platforms.

In the fast-evolving world of cryptocurrency, token minting has traditionally been perceived as a complex and intimidating process, accessible only to tech-savvy individuals. However, with the advent of xLFi Minters by LFi, this notion is about to change.

LFi, a trailblazer in the blockchain and fintech arena, is all set to launch a groundbreaking addition to its ecosystem – the xLFi Minters. These innovative hardware devices are designed to make token minting accessible and user-friendly for all, regardless of their experience level in the crypto space.

What is LFi Minting?

Before delving into the specifics of xLFi Minters, it’s essential to grasp the fundamentals of LFi Minting. While it shares similarities with traditional token mining, involving steps such as data verification, block generation, and recording authenticated information on a blockchain network, LFi Minting sets itself apart by leveraging the power of the Proof of Stake (PoS) consensus mechanism.

The PoS consensus mechanism – unlike traditional mining methods that rely on computational power – considers the amount of cryptocurrency an individual holds and is willing to “stake” or lock up as Minting utility Token. This decentralizes and enhances the security of the blockchain network while being energy-efficient.

The Function of Validators

In the world of cryptocurrency minting, validators play a pivotal role in confirming transactions, proposing new blocks, and ensuring the blockchain’s integrity. What makes this process truly remarkable is its decentralization, allowing virtually anyone interested in contributing to the blockchain’s security without the need for intermediaries.

This inclusive approach fosters a more accessible and democratic crypto ecosystem, eliminating the reliance on centralized regulatory authorities.

The Wide Range of Minting Solutions Offered by LFi

LFi understands that the path to financial freedom is a personal journey with diverse preferences and needs. Therefore, LFi offers three distinct methods for token minting:

xLFi Minter: Designed to be straightforward and accessible, xLFi Minter is perfect for newcomers to the cryptocurrency space.

CloudX Minting: A revolutionary system that simplifies and secures the minting of LFi tokens by allowing users to rent minting hardware in remote locations.

LFi One Smartphone: This groundbreaking device is specifically designed to support crypto minting, making it a mobile gateway to the world of decentralized finance.

Introducing xLFi Minters

Now, let’s focus on the latest addition to LFi’s lineup – the xLFi Minters. These dedicated hardware devices come in five versions: xLFi 500, xLFi 1000, xLFi 5000, xLFi 10000, and xLFi VALIDATOR.

Each model is meticulously crafted to facilitate the minting of digital assets, allowing users to choose the one that aligns best with their preferences and requirements.

One of the standout features of xLFi Minters is their user-friendly setup process. Unlike many other cryptocurrency-related hardware devices that demand extensive technical know-how, xLFi Minters are designed to be hassle-free to install.

Even if you’re new to the crypto world, you can set up your xLFi Minter at home with ease. Once installed, the hardware minting process with LFi is initiated automatically, eliminating the need for complex configurations or constant monitoring.

While detailed information about the xLFi Minter’s features is yet to be unveiled, anticipation is building around this new addition to LFi’s suite of minting solutions. LFi is renowned for delivering innovative and user-focused solutions, and the xLFi Minters are expected to be no exception. LFi’s commitment to providing accessible tools for financial freedom is at the core of this new product.

Minting Redefined

As LFi continues to push the boundaries of financial innovation, the introduction of xLFi Minters represents a significant step towards democratizing the token minting process.

These user-friendly hardware devices empower individuals in the world of cryptocurrency, aligning perfectly with LFi’s core philosophy of decentralization and accessibility. The xLFi Minter is a game-changer, making token minting easy and accessible to all, regardless of their experience level.

Stay tuned for updates as this revolutionary technology transforms the crypto world.

About LFi

LFi is a technology company that aims to empower the global fintech movement with new and innovative offerings that combine cutting-edge hardware with next-generation software. Leveraging the power of advanced computing and blockchain technology, LFi seeks to realize a future of financial independence through integrated products and solutions.

Tokenomics, the economic models behind cryptocurrency tokens, are a crucial aspect of any blockchain-based project. These models dictate how tokens are minted, distributed, and managed, playing a significant role in their value and functionality. This article explores four primary tokenomic models: the fixed supply model, the deflationary model, the inflationary model, and the dynamic supply model.

Each of these models has its unique features, advantages, and potential drawbacks. Additionally, the article delves into the token distribution patterns in metaverse tokens, highlighting the importance of fair distribution in fostering network effects, incentivizing participation, and maintaining price stability.

Tokens play a vital role in the decentralized metaverse ecosystem by facilitating the exchange of value and ownership. They also provide a means for tokenholders to engage in the decision-making process through governance proposals.

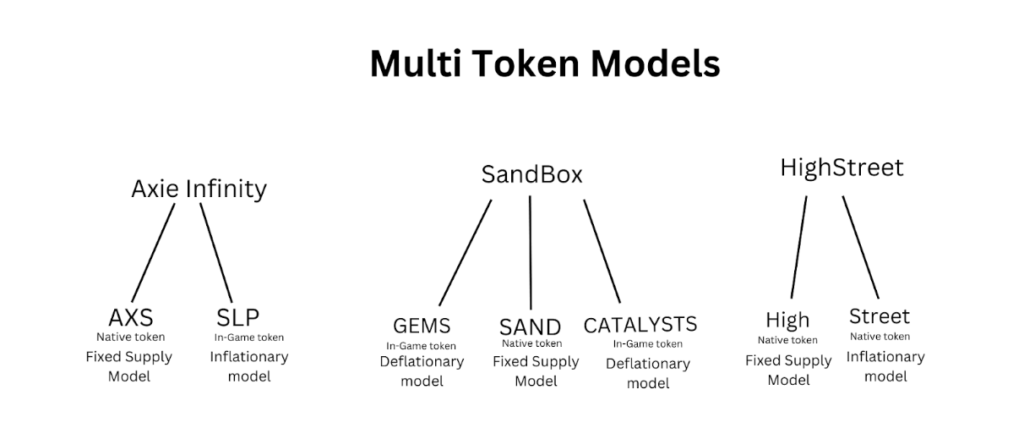

A carefully designed tokenomics model is key to aligning the incentives between different stakeholders in the metaverse. The first step toward designing tokenomics is deciding whether the platform will have a single- or multi-token system. A single-token system works best for metaverse platforms that have a limited scope of token utility.

A multi-token model is ideal for a complex metaverse ecosystem, where projects might want to have more than one token to serve different purposes. In a multi-token model, each token has its own unique use case and value proposition, and they are often designed to work together in a symbiotic relationship to create a more robust and functional ecosystem. Each token can have its own schedule and can be inflationary or deflationary.

Source: Cointelegraph Research

The use of multiple tokens can help to improve liquidity, incentivize different types of users, and create more opportunities for value creation and distribution. However, managing a multi-token model can be complex and requires careful design and implementation to ensure that the different tokens work together effectively and efficiently. It is also important to ensure that the supply and demand for each token are balanced to avoid over- or under-valuing any particular token in the ecosystem. The multi-token model is most commonly used by play-to-earn metaverses.

The tokens can be then further categorized into four main models:

The fixed supply model: Thisis the simplest and most common form of tokenomics model. In this model, a protocol mints a fixed supply of tokens either at the genesis or using an emission rate to mint the supply over a period of time.

Deflationary model: In a deflationary model, the supply of tokens decreases over time, either through a token burning mechanism. The token could be burned through different mechanisms (such is the case for Decentraland). 2.5% of the total MANA utilized is burned whenever someone purchases land in the metaverse. The primary purpose of the deflationary model is to increase the token value as the adoption increases. A major drawback of a deflationary model is that a scarcity in supply could occur in case the platform experiences a constant surge in the number of users.

Inflationary model: An inflationary model is the exact opposite of a deflationary token model. In this model, there is no limit on the number of tokens that could be minted, and there is an inflation rate that increase the circulating supply of the tokens over time. This model is useful to boost liquidity of a project by offering high staking rewards to the users. However, on the downside, the token is prone to hyperinflation in the long run, which can devalue the token and reduce investor confidence. This model is seldom used in a single-token system and is often a part of a multi-token system.

Dynamic supply model: This model does not impose a limit on the supply of tokens. Instead, it incorporates a burn rate to introduce scarcity, and as demand for the token grows, the algorithm adjusts the supply accordingly by increasing it. However, given the poor track record of algorithmic tokens, this model has yet to reach significant adoption.

Token distribution patterns of metaverse tokens:

The token distribution pattern plays an important role in the success of the tokenomics model of a project. A fair distribution would create network effects, incentivize participation, and maintain price stability. The pattern of token distribution varies from project to project, keeping the metaverse design and the hierarchy of stakeholders in mind as seen in the chart.

However, there are a couple of recurring patterns:

Token emission towards community incentives is higher than that for most projects, indicating the community-first approach of decentralized metaverse.

A dedicated distribution for the ecosystem is not the priority, and projects are more reliant on the treasury for the ecosystem growth.

Understanding tokenomics is vital for both project developers and investors in the blockchain space. The choice of model – be it the scarcity-driven deflationary model, the liquidity-boosting inflationary model, or the flexible dynamic supply model – can significantly impact a project’s success and token value. Moreover, the pattern of token distribution can shape the community’s engagement and the overall growth of the ecosystem.

As seen in decentralized metaverses, a community-first approach with high token emission towards incentives can drive participation and growth. However, it’s also important to note that each project’s unique needs and goals would dictate the choice of tokenomic model and distribution pattern. As the blockchain and metaverse landscape evolves, so too will the strategies and models employed in tokenomics.

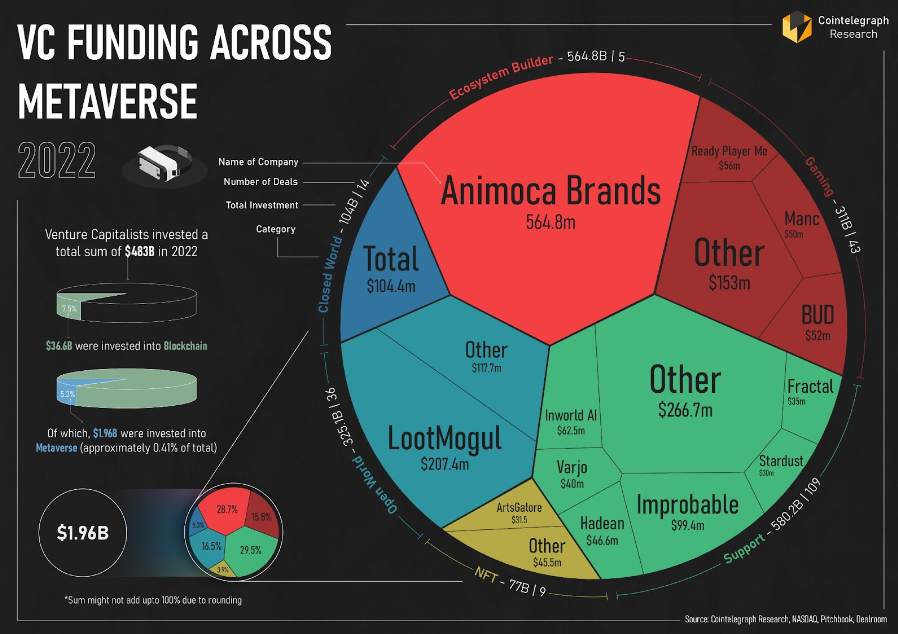

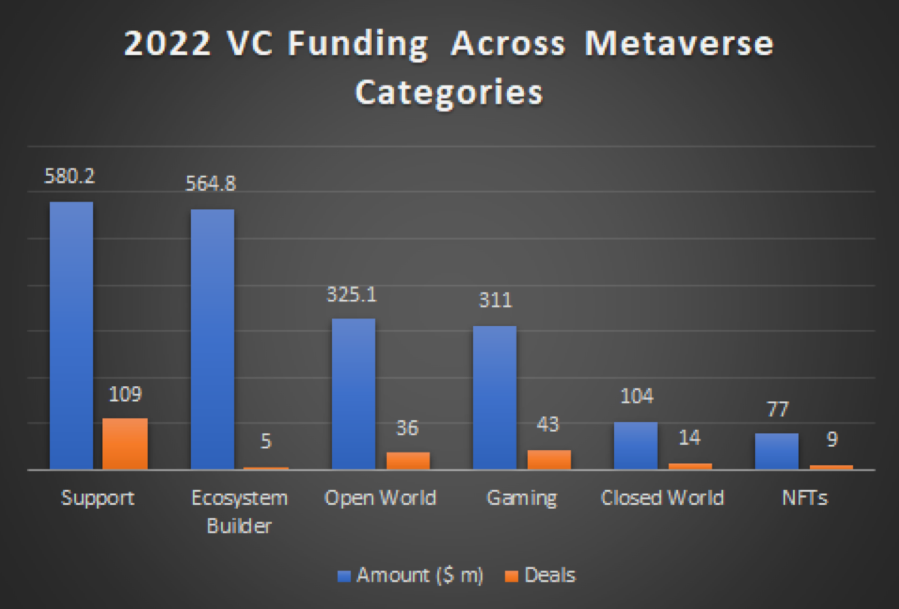

Venture capital (VC) funding in the metaverse has seen a significant surge, with over $2 billion invested in related activities in 2022, according to data maintained by Cointelegraph Research. This database, tracking over 5000 blockchain industry deals since 2012, indicates a shift from predominantly funding open metaverse platforms in 2021 to supporting service entities in 2022. These support services, focusing on customized metaverse architecture, AI, avatar creations, and more, accounted for over 50% of VC deals. The article further explores different metaverse categories, such as Support, Ecosystem Builder, Open World, Gaming, Closed World, and NFTs, and examines the funding trends within each.

Cointelegraph Research keeps a database of all venture capital and private equity deals in the blockchain industry. The database contains over 5000 deals since 2012 and is updated weekly and available for downloading here. According to Cointelegraph Research’s VC database, total VC funding on metaverse-related activities in 2022 surpassed $2 billion in 2022.

Elevated thresholds in the cost of capital, intermittent bouts of market volatility and general economic uncertainty may all put a limit on the ability of global venture funding to stage a strong comeback, following a year in which it was down by 35% YoY.

Total VC funding on metaverse related activities in 2022

If 2021 VC funding was largely centered around the funding of open metaverse platforms, the predominant texture of deals in 2022 involved support service entities that received over $580 million in funding. Support service startups focussing on customized metaverse architecture, AI, avatar creations, etc. currently account for over 50% of VC deals. While support service-related funding may dominate the volume charts, businesses with strong credentials in ecosystem building will likely attract the most lucrative VC deals in the metaverse.

Metaverse Categories

Support – This can be an umbrella of metaverse development services which includes building technologies to shape and grow businesses. Eg Meta/Oculus

Ecosystem Builder – These are projects that aim to provide the tools, and infrastructure required to build a metaverse. Eg. Roots Network

Open World – The open metaverse is a term used to describe the virtual world beyond any company’s walled garden. It is a single, connected universe where users can interact with each other regardless of which platform they are using. The Sandbox and Decentraland are examples of open metaverse platforms where individuals can create objects and move them across them.

Gaming

Closed World – The Closed Metaverse is a metaverse that is not open to the public. It is usually only accessible to employees of the company or organization that owns it. For example, Coca-Cola has its closed metaverse called “Coca-Cola World” that is only accessible to Coca-Cola employees. Other closed metaverses include IBM’s “Second Life” and Cisco’s “Virtual U”

NFTs

Source: Nasdaq

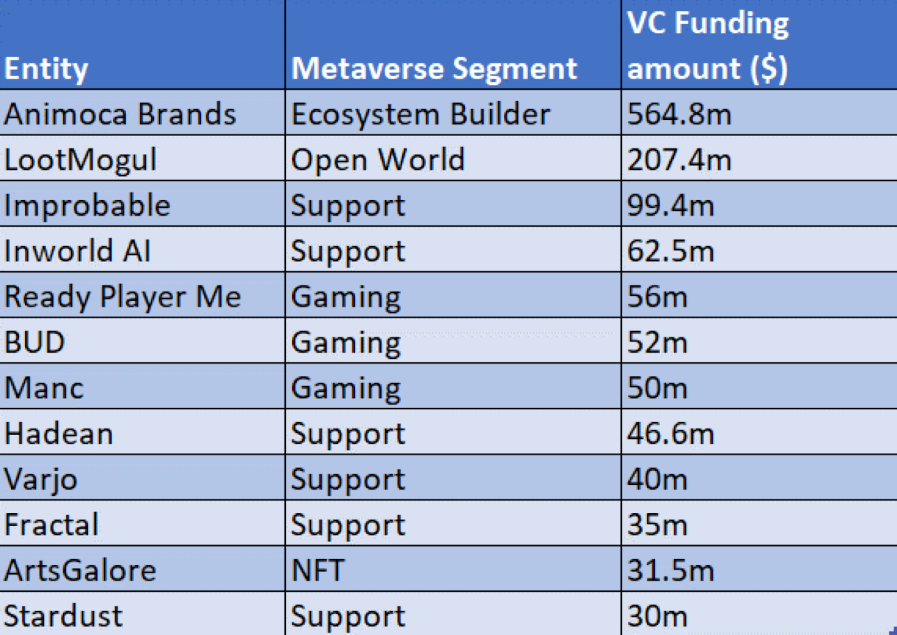

A case in point here is Hong Kong-based Animoca Brands (it garnered $360 million in just one round of funding with Liberty City Ventures, amongst others), which has been making waves in the building of an open metaverse and has already made investments in 30-odd metaverse-related projects. VC investors would likely prefer to fund late-stage ecosystem entities such as this that could then use their expertise to make more discerning choices and divert those VC funds to early-stage startups. The table below provides some context on the type of entities that attracted the big bucks from the VC world last year.

If there’s one area in the metaverse that appears to be going through a phase of enervation, it may well be the “user devices” segment or those companies involved in virtual reality, augmented reality and the virtual worlds where funding has been sliding sequentially for four straight quarters. VC interest may likely have cooled, as there are still ample encumbrances linked to the limited interoperability of these devices. If these devices are still unable to facilitate the linkage and usability of content across different virtual worlds, offered by different vendors, widespread adoption could remain stunted.

In conclusion, despite the challenges posed by elevated thresholds in the cost of capital, market volatility, and economic uncertainty, VC funding in the metaverse has shown resilience. While support services dominate the volume charts, businesses with strong credentials in ecosystem building have been attracting the most lucrative deals. However, it’s worth noting that the “user devices” segment, including virtual and augmented reality, is experiencing a downturn. This could be due to the limited interoperability of these devices, suggesting that there may still be hurdles to overcome in this rapidly evolving sector.

The metaverse, despite its current imperfections, opens up a world of opportunities for businesses to innovate and overcome its inherent flaws. This article explores the potential strategies companies could adopt to build scale in this fragmented landscape, focusing particularly on the inorganic route, or acquisitions. It will delve into the concept of M&A (Merger and Acquisition), the role of valuation multiples, and how a possible ‘metaverse winter’ might affect these.

The discussion will also touch upon past M&A trends in the technology, media and telecom (TMT) sector, which is responsible for a significant portion of metaverse-related M&A deals, and look at the potential targets for future M&A activities. Additionally, it will highlight key end markets like gaming, e-commerce, and the emerging health and fitness market, that could drive metaverse-related M&A activity.

The metaverse, in its current state, is hardly indefectible, but the prevalence of existing inadequacies will only spur opportunities for incumbents to iron out some of the inherent flaws and transform the metaverse into a more consummate state. Considering this status quo, deploying capital to deepen in-house intellectual property (IP) infrastructure may prove to be a very fulfilling proposition over time. However, when you consider that the metaverse is currently a very fragmented landscape, with multiple parties scrambling to reach the top, the more expeditious strategy to build scale and fill gaps in the service portfolio could likely be through an inorganic route — i.e., acquisitions (provided integration challenges are kept to a minimum).

Learn M&A

Inorganic route is another term for M&A. Organic route is when the company spends capital expenditure and R&D to develop their own products/tech. Inorganic route is when they feel they are better off spending money by acquiring another firm that has the requisite tech they need, rather than building it inhouse.

Besides, the onset of a metaverse winter may also bring down acquisition multiples to more palatable levels, thus maintaining the scope for substantial merger and acquisition (M&A) activity in 2023 as well. For example, Microsoft’s acquisition of Activision Blizzard in an all-cash deal for ~$69bn (7.6x EV/Sales multiple, 20.2x EV/EBITDA multiple). A healthy enterprise value (EV) to sales multiple is around 1x to 3x, and a healthy enterprise value to earnings before interest, taxes, depreciation, and amortization is between 11 and 16. In line with higher interest rates, we suspect valuation multiplies will continue to come down over the next year.

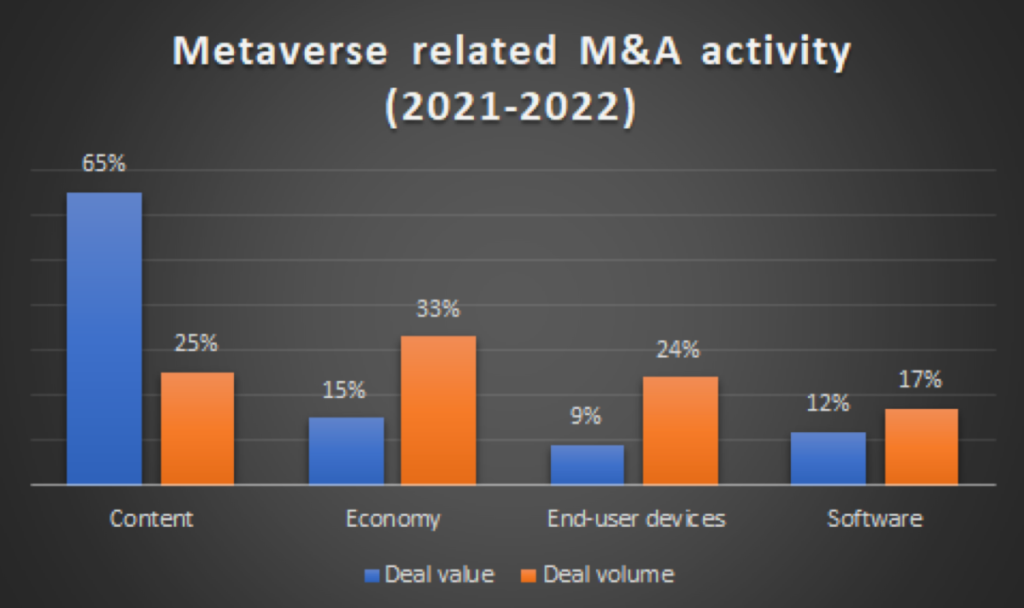

For perspective, over the last two years, the technology, media and telecom (TMT) sector, which is typically responsible for 75% of all metaverse-related M&A agreements, engaged in 115 deals, totaling $174 billion in aggregate. The table below sheds light on some of the interesting metaverse-related deals that took place last year.

If the past is any indication of the future, entities with content-rich portfolios and libraries are likely to be chief targets for prospective M&A buyers. Over the last two years, content-related acquisitions have accounted for the lion’s share of metaverse-related M&A by value (skewed no doubt by Microsoft’s proposed acquisition of gaming entity Activision Blizzard) while also accounting for a quarter of all deals by volume (the second-highest category).

As far as end markets go, gaming and e-commerce could likely serve as principal hubs of M&A-related activity, as those markets look set to remain the hotspots of the metaverse universe, even by the end of this decade (both of those segments will likely account for 75% of the metaverse-related spending by 2030).

Figure 2 Source: Deloitte

The burgeoning health and fitness market is another promising landscape that could witness greater impetus in metaverse-related M&A undertakings, as 81% of global healthcare executives have already flagged that the metaverse could have a positive impact on their organizations, whilst nearly 50% believe the impact could be transformational.

The metaverse presents an exciting frontier for businesses, with the potential for dynamic growth through strategic acquisitions. As we’ve explored, the inorganic route could be a viable strategy for companies to quickly scale and enhance their service portfolio. Past trends indicate that entities with content-rich portfolios are likely to be the main targets for M&A activities, and markets like gaming, e-commerce, and health and fitness are poised to be the hotspots for metaverse-related spending.

With almost half of global healthcare executives believing the metaverse could have a transformational impact on their organizations, the stage is set for a surge in metaverse-related M&A undertakings. However, the ever-changing nature of the metaverse landscape requires businesses to stay agile, making informed decisions based on careful evaluation of market trends and valuation multiples.

In the era of digital transformation, traditional financial institutions are not only adapting but also innovating to stay relevant. This article explores how global entities like HSBC, JPMorgan, and others are venturing into the burgeoning metaverse – a virtual reality space where users can interact with a computer-generated environment and other users.

These companies have announced partnerships and plans to engage with their customers in unique ways, from hosting events in virtual stadiums to launching virtual versions of real-world locations. Additionally, crypto companies are also joining the race, leveraging the metaverse to enrich user experiences and expand their digital presence.

HSBC

HSBC announced a partnership with The Sandbox, in which the financial institution will have a stadium that will be used for engaging with sports, esports and gaming fans.

Furthermore, the bank plans to bring the World Rugby Sevens Series into its metaverse experiment, as the bank is the official sponsor of the event.

JPMorgan

JPMorgan has also joined the metaverse race but decided to open a lounge in Decentraland, the other top player in the metaverse sector.

The bank launched its blockchain unit, Onyx, which offers institutions and businesses an opportunity to enter the metaverse. JPMorgan’s lounge is located in the Metaiuku District, a virtual version of Tokyo’s Harajuku shopping district, where users can watch experts talk about the crypto and finance markets.

Corporate Marketing in the Metaverse

Launching metaverse-related initiatives in the financial sector has grown around the world, with institutions in other regions, such as Asia and Latin America, also entering this race.

The Industrial Bank of Korea (IBK) announced its plan to launch a virtual realm on the social media platform Cyworld Z, one of the most popular social media platforms in South Korea. The Company aims to set up an IBK Dotori Bank in the metaverse, which will launch financial products tailored for Cyworld Z (IBK’s platform) users.

NH NongHyup Bank also announced the launch of “NH Dokdo-verse,” a metaverse replica of Dokdo Island, a beautiful destination that is difficult to travel to in real life. It’s expected that users will be able to interact with one another by playing fishing games and buying land. This move came after the active promotion of the real island by the bank.

Interbank: In December 2022, the company was the first Peruvian bank to enter the metaverse. The company’s headquarters (the Interbank Tower), which is located on an important highway in Lima, arrived in Decentraland. The bank plans to engage more closely with its customers, expand its digital presence and interact with the bank’s content.

Crypto companies in the metaverse “race”

The metaverse race has also attracted the interest of different crypto companies trying to build their presence in this virtual realm with partnership announcements with leading The Sandbox, Decentraland or Bloktopia. The moves were an attempt to bring users to their virtual spaces and enrich their experiences.

Binance: One of the leading crypto companies acquired 4,012 LAND NFTs in The Sandbox world. A total of 1,859 land plots adjacent to Binance’s estates were sold to Binance users. The further development and use cases of the acquired land are still unknown.

Kraken: The U.S. exchange has partnered with Decentraland, with the company hosting virtual events, such as a Metaverse Music Festival. The event, which started in 2021, is a collaborative music festival that features over 500 artists in different virtual realms and stages in Decentraland. Although the event is open to the public, Kraken sends early-bird invitations to its user base, which can interact, listen to the lineups and collect NFT wearables.

Other companies: KuCoin, CoinMarketCap, Cointelegraph, and blockchain projects such as Solana, Chilliz, Chainlink and Polygon have partnered with Bloktopia, a Polygon-based metaverse. In those spaces, the companies and protocols are tenants of the virtual space, with some of them utilizing it as a virtual office or as a virtual branch of the company.

In summary, the financial sector is actively embracing the metaverse as a new frontier for customer engagement and marketing. Whether it’s HSBC’s stadium in The Sandbox or JPMorgan’s lounge in Decentraland, these initiatives demonstrate the sector’s commitment to innovation and customer-centricity. Moreover, the involvement of crypto companies like Binance and Kraken further validates the potential of the metaverse. As more institutions continue to explore this virtual realm, we can anticipate a paradigm shift in how businesses and customers interact, offering exciting opportunities and challenges alike. The future of finance, it seems, is not just digital, but also virtual.

In an era where technology permeates every aspect of our lives, leading brands like Adidas, Gucci, and Nike are exploring new territories in the digital realm. The concept of Web3 and the metaverse has piqued the interest of these global giants, prompting them to venture into this uncharted territory. Nike, a pioneer in its field, has already established a strong presence in the metaverse, while Adidas and Gucci are not far behind. With their respective strategies, these brands are redefining the intersection of fashion, technology, and customer engagement.

Nike has been particularly enthusiastic about the possibilities that the metaverse offers, filing patents for virtual apparel and footwear, and even launching a Roblox-based universe called Nikeland. Adidas, on the other hand, has collaborated with Bored Ape Yacht Club (BAYC) for its first NFT collection, “Into the Metaverse,” and has acquired virtual land in The Sandbox metaverse. Gucci, a luxury fashion brand known for its innovation, has opened “Gucci Town” in Roblox and established partnerships with Zepeto and Superplastic.

Nike

Nike has been really supportive and enthusiastic about Web3 and the metaverse. Apart from filing several patents regarding plans of selling virtual apparel and footwear, Nike has already established a strong presence in the metaverse by:

Launching a Roblox-based universe called Nikeland intended to be a free immersive sports space where users can interact with one another and participate in free sporting events. The company launched this initiative in November 2021 with the intention to help users turn sports and gaming into a lifestyle. So far, it has received 7 million visits. In this world, buildings, fields and courts are inspired by the Nike headquarters and are also equipped with detailed scenarios where the skills of Roblox users are put to the test in mini-games. Furthermore, it’s expected that users will be able to purchase branded clothes for their avatars.

Acquiring RTFKT. Nike acquired RTFKT, a leading brand and NFT studio in December 2021. Founded in 2020, RTFKT is pioneering and innovating brand-building in the boundaries of physical and digital economies.

Nike launched its first collection of NFT sneakers created in a collaboration with RTFKT Studios, “CryotoKicks Dunk Genesis,” a collection of 13,570 items that has generated over 7,600 Ether (ETH) of traded volume. An interesting feature is that users can customize each pair using “skin vials.” These vials can be created by different designers, adding special effects and patterns to the base sneakers.

Furthermore, Nike has continued releasing drops (with RTFKT), including a complete NFT collectiondrop called CloneX (an NFT profile picture collection from RTFKT). With this collection, the company has also included a merch drop by airdroping Nike Air Force 1 with designs based on specific Clonex NFT traits. This collection, called RTFKT CloneX Forging SZN 1, has raised a total of 3,500 ETH as total traded volume.

Nike has demonstrated its ability and willingness to interact and experiment with Web3 and metaverse technology, and it seems to be paying off. According to on-chain analytics, Nike has outperformed every other brand that has interacted with Web3 and NFTs when considering the revenue its initiatives have generated. In this case, Nike, thanks to RTFKT, has generated over $180 million in revenues (primary and royalties), while Adidas, another sports apparel company, has only generated 10% of that amount.

Adidas

Adidas has also made big moves when it comes to its Web3 and metaverse strategy.

NFT drop in collaboration with Bored Ape Yacht Club (BAYC), Adidas sold its first NFT collection, “Into the Metaverse,” back in December 2021.

The NFTs were sold for 0.2 ETH each, and each unlocks a digital and physical wearable (hoodie, tracksuit and Gmoney’s signature orange beanie). Furthermore, the digital version will be used in The Sandbox metaverse. As part of this initiative, Adidas purchased its first NFT, BAYC #8774, for its “Into the Metaverse” campaign.

Gucci is another brand that has made significant and courageous moves in metaverse by:

Opening “Gucci Town” in Roblox. On May 22, Gucci started a short-term presence in Roblox with a garden space called “Art Garden.” This space, conceived as a virtual representation of an installation called Gucci Garden Archetypes in Florence, was available for Roblox Users for two weeks.

Making the place look like a central garden (with the classic Gucci logo) and having connections to different stages where users can perform different activities, such as playing mini-games and visiting a store, where it’s possible to purchase Gucci merchandise for Roblox’s avatars. According to the company, over 20 million players have visited the garden.

Establishing a partnership with Zepeto. In February 2021, Gucci partnered with Zepeto, a leading app and social platform that personalizes avatars and creates virtual worlds. With the collaboration, Zepeto users are able to purchase and dress their avatars with pieces from Gucci House’s latest collections and explore the Gucci Villa world.

Collaborating with Superplastic for an NFT series. The vinyl toy brand partnered with Gucci to launch a unique NFT collection featuring Gucci-styled Superplastic characters. The complete set is designed by Gucci head of design Alessandro Michele and will come with a physical ceramic representation, which will be handmade by Italian artisans.

At the time of this writing, the collection’s floor price is 0.82 ETH ($1,300) and has a total trading volume of 6,00 ETH.

Launching a virtual experience in The Sandbox. This space is based on the Gucci Vault platform and will offer immersive experiences, including an experimental store with Gucci vintage pieces.

Other Fashion brands

Other brands have started experimenting with metaverse technology. Most of them joined Decentraland in the first metaverse fashion week event. Brands like Estée Lauder, Tommy Hilfiger and Dolce & Gabbana understand that this virtual realm has the potential to convert the e-commerce shopping experience from 2D product images into a 3D immersive shopping experience.

In this event, there was a virtual fashion exhibition and the opening of the Fashion District, where 15+ brands, including Tommy Hilfiger and Hogan, have flagship virtual stores.

The innovative steps taken by Nike, Adidas, and Gucci towards embracing the metaverse and Web3 technology have set the stage for a new era in the fashion industry. Their experiences provide valuable insights for other fashion brands that are yet to venture into this space. For instance, brands like Estée Lauder, Tommy Hilfiger, and Dolce & Gabbana have begun experimenting with the metaverse through participation in the first metaverse fashion week event in Decentraland.

In conclusion, it’s evident that the metaverse is more than just a passing fad; it’s a revolutionary platform that’s transforming how we interact with brands and consume products. As Adidas, Gucci, and Nike continue to innovate and expand their presence in the metaverse, they’re setting a standard for other brands to follow. The success of these brands in the metaverse also underscores the importance of adapting to technological advancements and customer expectations in today’s digital age. Indeed, the future of fashion lies in the metaverse, and brands that embrace this will likely lead the pack in the years to come.

In the era of digital transformation, the metaverse has become the new frontier for technology companies. As a virtual reality space where users can interact with a computer-generated environment and other users, the metaverse is breaking boundaries and opening up endless possibilities for businesses and consumers alike.

This article delves into the strategic moves and plans of four major companies – Apple, Spotify, Tinder, and Shopify – as they navigate their paths in this burgeoning space.

Apple

Unlike the other tech giants, Apple has neither released nor joined the “metaverse race” publicly; however, it is building a strong footprint on the infrastructure by working on an advanced high-end AR/VR headset that could be ready in 2023, according to Bloomberg.

This bet reflects Apple CEO Tim Cook’s ideas:

“I think AR is a profound technology that will affect everything. Imagine suddenly being able to teach with AR and demonstrate things that way. Or medically, and so on. Like I said, we are really going to look back and think about how we once lived without AR.”

Tim Cook, CEO Apple

Spotify

In May 2022, the music streaming company announced its entry into the virtual world with a partnership with Roblox and launched “Spotify Island.” In this world, users (both artists and fans) can hang out and explore a “wonderland of sounds, quests” and obtain exclusive merch for their Roblox avatars.

With this move, Spotify is the first music-streaming company to have a presence in the Roblox game and start exploring innovative methods, in which their users can interact and establish new relationships with artists and creators.

The visuals of this virtual world are based on green areas, with different icons (such as “Like” icons for redeeming free virtual merch) and interactive quests. Related to merch, the company explains that a portion of sales will go to the artists (but has not revealed what specific share).

It’s expected that users will be able to go to different themed islands, each of which has related content, activities and quests. The first one will be “K-Park,” a perfect place for all K-Pop culture.

Tinder

Back in December 2021, Match Group, the holding company of Tinder, announced its plans to enter the metaverse race with its so-called Tinderverse virtual world; with this, the company also announced plans to launch its own in-app currency, Tinder Coins, which was intended to reward customers who were active on the app and be accepted as payment for premium Tinder features.

To make a more aggressive bet, Tinder acquired the AI and AR firm Hyperconnect, a well-known social discovery and video technology firm that launched two flagship apps: Azar (live video and audio chat) and Hakuna Live (a social live streaming app). Match Group expects the acquisition will help it to expand online dating and social features on its apps.

However, last August, Bernard Kim, the company’s CEO, instructed the Hyperconnect team to scale back and “not invest heavily in the metaverse at this time,” citing uncertainty about how the whole metaverse will look and a more challenging operating environment. This happened after the resignation of Tinder CEO Renate Nyborg and disappointing Q2 earnings. On Dec. 22, the company decided to delist Match Group’s stock.

Shopify

Similar to Apple, the biggest e-commerce platform is betting on incorporating AR into its business in the e-commerce segment. Currently, Shopify — thanks to a partnership with Poplar Studio — has been allowing merchants to launch a 3D and AR version of products on their respective sites.

According to Poplar Studio, “Once the brand has built the 3D model of its catalog, it can create the AR visualization experience, helping seeing the products in more detail, overlying the 3D models onto the real world from the app/web.”

Furthermore, the company has announced a partnership with Novel, a no-code Web3 e-commerce platform. Thanks to this partnership, the startup launched an app on Shopify Store to equip existing merchants on Shopify with easy-to-use tools to experiment with Web3 without any technical knowledge. The core features allow for the creation (minting) and distribution of NFTs to be bought in the Shopify merchant front end.

The movement and interest in the metaverse have also attracted “legacy” or “traditional” fashion brands to the space. The move here appears to have strengthened its product offering and created a virtual immersive store where brands can interact with the worldwide public and sell virtual items.

As we’ve explored, Apple, Spotify, Tinder, and Shopify are all making their mark on the metaverse in unique ways. From Apple’s advanced AR/VR headset to Spotify’s musical wonderland on Roblox, Tinder’s virtual world and in-app currency to Shopify’s AR-enhanced e-commerce experience, these companies are leveraging technology to create immersive and interactive environments for their users.

While the future of the metaverse remains uncertain, one thing is clear: these tech giants are leading the charge and shaping the future of this exciting new digital realm.

A new generation of blockchain-based projects have begun to ascend into the crypto industry, ChainGPT is there to provide them with the necessary support and tooling to help them succeed.

ChainGPT, the leading AI Infrastructure provider for the crypto, blockchain, and Web3 industry is bringing one of its most promising incubation projects to the public. After months of careful planning, diligent development, and community building, Solidus AI Tech will be taking its next step into Web3 and launching its $AITech IDO on the ChainGPT Pad.

With their world-class team, mesmerizing website, incredible network of connections, and rock-solid plan of action, Solidus AI Tech is ready to bring its products to market and become an active player in the digital economy!

What is Solidus AI Tech?

Based in Europe, Solidus AI Tech is an IaaS (infrastructure as a service) company that is solving some of the most prevalent, fundamental issues plaguing the digital economy; namely the demand for computational infrastructure. Building out their own 8,000-square-foot facility to house hardware that has been wired with their proprietary algorithms that improve computational costs and efficiencies. In tandem to the physical infrastructure, they are tapping into their resources to provide a full stack of cutting-edge Web3 infrastructural software solutions including Artificial-Intelligence-as-a-service (AIaaS), Blockchain-as-a-Service (BaaS), High-Performance Computing power (HPC), and an Artificial Intelligence marketplace.

What does AI Tech Provide?

As an infrastructure services company, Solidus AI Tech is providing a suite of four core services that can be used by companies, institutions, and even governments as a foundation to build sustainable digital systems. From metaverse to CBDC to gaming and beyond this is what AI Tech is providing:

AIaaS– Artificial-Intelligence-as-a-service Artificial intelligence is the frontier of mankind’s intellectual flourishing. Considered to be just as, if not more important a technological revolution as was the steam engine, AI has become the building block for new technologies promising to improve the lives of people around the world. Solidus AI Tech has neatly wrapped up a turnkey solution to jumpstart the integrations and implementations of AI into a broad range of applications.

BaaS– Blockchain-as-a-service Building blockchains from scratch is an extremely tedious, long, and resource-intensive (labor and capital) process. Building quality blockchains that can satisfy the security and operational demands of sensitive, high-value operations if even more arduous. Solidus AI Tech is extending its intelligent blockchain designs for any imaginable use case.

HPC– High-Performance Computation The demand for computation continues to grow alongside the world’s population that is coming online and new energy-dependent solutions are introduced into society. Solidus AI Tech provides computation for the most intensive use cases across a multitude of industries.

AI Marketplace The exchange of automated intelligent processes unlocks an entirely new machine economy that contributes to a potentially entirely new and untapped market segment. Solidus AI Tech will be providing a venue where industrial and individual AI commerce can take place.

What are some of AI Tech’s Unique Features?

Apart from the four key products that Solidus AI tech provides, there is a mixture of sophisticated novel developments at the design, code, and principle layers of the project that make it stand out from the crowd and supersede all existing solutions attempting to spearhead the enormous, evergreen market segment of Computational Infrastructure.

Some of these features include:

High-Performance Computing Costs reduction Notorious for its insatiable energy demands, HPC is a problem that is looking for solutions beyond just the linear increase of hardware. Solidus AI Tech has developed proprietary algorithms that improve hardware efficiencies by 40% above the benchmark rate of existing industry standards; driving down costs, while increasing efficiency.

Eco-Friendly Computation IP (Intellectual Property) Going hand-in-hand with its HPC reductions costs, a byproduct of Solidus AI Tech’s focus on optimization has resulted in the creation of innovations granting them intellectual property in the form of algorithmic systems that is much friendly for the environment with its efficient (lowered) consumption of energy and heightened computational capacity.

Custom Data Center Solidus AI Tech has been able to secure a location with some of the lowest-cost energy and highest internet speed internet in all of Europe. With the presence of an in-house data center, Solidus AI Tech is in control of the computational supply chain and has full sovereignty in optimizing its service across every vertical of supply and demand. Built in Bucharest, the facility spans some 8,000 square feet and operates under ISO 14001:2015.

Vulnerability Monitoring Security, monitoring, and specifically designed firewalls, Solidus AI tech provides a full spectrum of proactive protective measures to ensure the reliability of its systems. Leveraging novel structures of network devices existing without IP or MAC addresses alongside its protocol of automatic vulnerability detection satisfies the most stringent institutional security requirements.

Government Enterprise Blockchain Solutions Utilizing a combination of its software and hardware solutions, Solidus AI Tech is able to service the most demanding use cases while adhering to NATO quality assurance standard. From voting, taxation, land registration, and supply chain traceability to Healthcare and Identity management; the security, flexibility and expertise Solidus AI Tech provides caters to every grade of entity.

Solidus AITECH Tokenomics

In tune with the forward-looking innovations that are coming out of Solidus AI Tech’s ecosystems, their vision of a decentralized, digital future is underscored with its elegant tokenomics that complement and underpin their system processes. Empowering users of all types with equal access to high quality infrastructure the $AITECH token adheres to inclusive, cost-efficient ideologies. From a payment vehicle for their product licenses, an incentive for creating and publishing quality AI tooling, and membership to the DAO, $AITECH is worth taking a look at:

Token Name: AI Tech Token Symbol: $AITECH Token Standard: BEP-20 Issuing Network: Binance Smart Chain Total Supply: 2,000,000,000

Moreover, the $AITECH token has adopted the leading practices in deflationary economics by implementing a variable burn program that takes 5%-10% of every transaction used for acquiring platform serves and systematically removes them from circulation; thereby exerting constant pressure on the open market dynamics of the asset.

$AITECH IDO on ChainGPT Pad Details

Solidus AI Tech has dedicated a portion of its supply for the ChainGPT Pad IDO as follows:

IDO Date: 08/21/2023 Token Price” $0.012 Supply Allocation: 13,333,333.33 $AITECH tokens Max Allocation: $160,000 Listing on Exchanges: August 28th, at 10 AM (UTC)

More information about the IDO specifications are available in their official listing here.

* ChainGPT implements a unique protection mechanism for all IDO participants in the form of a refund policy. After an IDO has been completed, if for any reason participants feel as though they would rather revise their contributions, they have up to 7 days to do so (unless they claim their allocations). For a more in-depth explanation of the ChainGPT Pad refund policy refer to their official article discussing it here.

About ChainGPT

ChainGPT is the leading provider of AI-powered Infrastructure for the crypto, blockchain, and Web3 industry. The one-stop-shop Crypto AI hub. From automated smart contract generation and auditing, to autonomous community management, advanced Web3 AI chatbot, AI-powered news aggregation, and NFT generation, ChainGPT is the most sophisticated, end-to-end AI solution on the market.

The metaverse as a future virtual reality has been explored for a long time, with projects like Decentraland launching its first beta in 2017; however, 2021 changed everything.

The concept of the metaverse, a collective virtual shared space created by the convergence of virtually enhanced physical reality and physically persistent virtual reality, has been around for quite some time. However, it was in 2021 when interest in this futuristic realm skyrocketed, thanks largely to Facebook’s rebranding to Meta and its ambitious pledge to “bring the metaverse to life.” This article delves into various companies’ ventures into the metaverse, with a particular focus on Meta’s extensive efforts and investments, despite significant financial challenges.

Facebook announced its rebranding to Meta in October 2021. The company announced a complete company pivot and a new focus of the entire company to “bring the metaverse to life and help people connect, find communities and grow businesses.” After that, the amount of interest for “the metaverse” reached all-time highs: Companies around the world had started making announcements about their entries to the metaverse as they started working and building. According to market research company Newzoo, this number grew from 200 back in July 2021 to more than 500.

Are these moves and announcements part of a long-term strategic shift or only marketing buzz?

In this part of the report, we will focus on discovering those companies, exploring what and where they are trying to build their metaverse presence.

Facebook

The company Facebook has extremely lofty ambitions for the future of the internet and the metaverse, making the metaverse its biggest priority. Apart from the name change, the company is building its own metaverse platform, investing billions in the industry, and acquiring or developing different parts of the infrastructure.

Oculus/Meta Quest: The ex-startup was acquired by Facebook for $2 billion in mid-2014. It’s currently the most popular VR headset, with the second version (Meta Quest 2) selling over 14.8 million units since its launch in 2020, according to International Data Corporation.

Horizon Worlds: Meta’s first virtual world, it launched in December 2021 and is currently live for users in the United State and Canada. This virtual world serves as a free app, where users can hang out with friends, meet new people, play games and attend different virtual events. According to the platform, there are +10,000 worlds available right now.

Research and development: Meta has committed millions of dollars to research new technologies that could unlock the metaverse’s full potential, including VR, AR, AI, blockchain and crypto economies, and artificial vision, among others. Furthermore, the platform has launched a $50-million fund to invest in global research and program partners to help build the metaverse collaboratively.

Despite these efforts, Meta was one of the most impacted Big Tech companies from a turbulent macro environment and general market crackdown: Meta had to lay off over 11,000 employees and saw a sharp decline in its own stock, which lost 70%+ of its value from its peak of $300 per share down to $90 per share. Furthermore, in its Q4 2022 earnings call, the company announced that its metaverse unit (Reality Labs) recorded a $4.28-billion operating loss, bringing its total for 2022 to $13.72 billion. Although the unit only accounts for less than 2% of Meta’s revenue, it’s losing six times the amount of money it generated as revenue.

Despite this, the company continues to support its new vision, saying, “Reality Labs’ losses will increase in 2023 as they will continue to invest meaningfully in this area given the significant long-term opportunities that we see.”

Microsoft

The company has also been working on its own virtual realm; however, Microsoft’s strategy is different from Meta’s, as the Bill Gates-founded company is aiming to build a more work-focused metaverse, currently called “Microsoft Mesh.”

In its strategy, its “metaverse” is expected to be connected with Microsoft’s product offering and allows teams and people in different physical locations to send chats, join virtual meetings, collaborate on shared documents, etc. and will include different ways to share content, including “Presenter Mode” and “Together Mode.” These modes are already live on the platform.

Apart from this, the company has developed its tech in-house: It owns augmented and mixed reality lenses called HoloLens. This hardware is currently used by several big enterprise clients, including Audi, Toyota, Airbus, Goodyear and the United States Army.

Furthermore, the company is well-positioned to grow and interact with gaming-related metaverses, which is supported by Satya Nadella, CEO of Microsoft, who believes “gaming will play a key role in the development of metaverse platforms.” The company currently has a strong footprint in that vertical:

Activision Blizzard acquisition. In early 2022, Microsoft acquired Activision Blizzard, a leading game developer studio, for $68 billion, making it the most expensive gaming acquisition of all time. This acquisition gives Microsoft the intellectual property of top-tier games, including Guitar Hero, World of Warcraft and CandyCrush, among others.

Owning Mojang Studios. Microsoft owns the creators of one of the most popular virtual world games, Minecraft, which has over 141 million active users and has sold 200 million copies since its launch. It’s important to highlight that Minecraft is often cited as an example of an existing, early-stage, closed version of a virtual world with metaverse characteristics. However, the company has banned NFT-related tech use cases.

Google

The company is focused on the tech stack and has already invested millions of dollars in Big Tech trends: VR, AR, XR and 3D cloud storage content.

The company also launched Google Labs, committing strong efforts to R&D for projects such as Area 120 (Google’s in-house incubator) and ARCore, among others.

Furthermore, Google relaunched its AR Google Glass and has secured a European trademark for the new version. According to company’s announcement, it will test the prototype in a public setting when available.

Despite the turbulent macro environment and substantial financial losses, Meta remains undeterred, continuing to invest heavily in the metaverse. The company views this sector as a long-term opportunity with significant potential. Despite the skepticism and the financial hurdles ahead, Meta’s commitment to the metaverse signals a shift in how we perceive and interact with digital spaces. As we move forward, it will be intriguing to see how this bold vision shapes the future of the internet and whether other companies will follow suit in this brave new digital world.